Company Profile: Bubs Australia Limited (ASX: BUB) offers a wide range of organic baby food, goat milk infant formula products, the adult goat milk powder products and fresh dairy products. The group had identified a single operating segment being the sale of nutritional food, fresh products, adult powder and providing canning services of nutritional dairy product. BUB segregates its revenue by region in three segments, namely Australia, China and Other International.

.png)

BUB Details

.PNG)

Significant Improvement in Margins and Strong Balance Sheet: Bubs Australia Limited (ASX: BUB) is a producer of Australian premium infant nutrition and goat dairy products. As on 14 April 2020, the market capitalization of the company stood at $431.43 million. During FY19, the company progressed on its vertical integration capabilities and extended its infant nutritionals product portfolio. It advanced its China strategy and strengthened its financial capability. During FY19, gross revenue of the company witnessed an increase of 154% and stood at $46.8 million, with strong cash reserves of $23.3 million. This high growth profile has been achieved through continuous focus on four key drivers including, domestic market penetration, brand awareness and impact, innovation and product development and enhanced Asian focus. BUB also saw the creation of Australia’s first organic grass-fed infant formula range and witnessed a change in product focus and channel mix.

BUB has also released its interim results for the period ended 31 December 2019 wherein it had a continued focus on executing its foundation strategy with key partners to build on strong competitive advantage and unique assets. During 1H20, the company reported strong performance of Bubs® infant formula in all retail channels and regions with a record revenue of $28.8 million, reflecting an increase of over 37% on the pcp. In the same time span, it witnessed an improvement in gross margin and has maintained a consistent half-year growth trend since listing in 2017.

The company expects new markets and product launches to build on existing foundations that will drive incremental revenue streams. The company is well placed to pursue its strategic goals towards delivering profitable and sustainable growth and is confident of achieving overall profitability in the years to come. The new agreement with Woolworths provides a leading platform to gain market share in larger organic bovine formula segment..png)

Key Financials (Source: Company Reports)

Details of Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of Bubs Australia Limited. C2 Capital Global Export-To-China Fund, L.P. is the largest shareholder in the company, with a percentage holding of 9.41%. .png)

Top 10 Shareholders (Source: Thomson Reuters)

Increased Profitability and Stable Balance Sheet: During 1H20, gross margin of the company stood at 13.6%, as compared to a negative margin in the prior corresponding period. In the same time span, EBITDA margin of the company also improved substantially, representing a decent growth trajectory. During 1H20, net margin of the company also witnessed an improvement on the prior corresponding half, indicating that the company is managing its costs well and is capable of converting its revenue into profits. During 1H20, current ratio of the company went up to 3.03x, up from 2.03x in 2H19. This indicates that the company is liquid enough to pay off its current liabilities using its existing assets. In the same time span, Assets/Equity Ratio went down to 1.39x from 1.46x in 2H19, and Debt/Equity Ratio of the company stood at 0.04x, lower than the industry median of 0.19x. This indicates that the business is financed with a significant proportion of investor funding and a small amount of debt, resulting in a financially stable balance sheet..png)

Key Margins (Source: Thomson Reuters)

Highlights for the Third Quarter Ended 31st March 2020: During the quarter, the company reported gross revenue amounting to $19.7 million, representing an increase of 67% on pcp basis and an uplift of 36% on Q-o-Q basis. As a result of a strong performance by Bubs® infant formula range, which witnessed an increase of 137% in sales on the prior corresponding quarter, the company delivered a positive operating cashflow amounting to $2.3 million, with a strong cash balance of $36.4 million at the end of the period. Bubs® Organic Baby Food represented 4% of the gross sales during the period, witnessing an increase of 17% on the prior corresponding period. The company has not faced any supply chain or manufacturing disruptions due to its offerings falling under the category of Essential Service and has managed to deliver the required services in the wake of increase in domestic demand.

Market-Wise Performance in the March Quarter: Sales to Australia formed 64% of gross sales and went up by 34% on the prior corresponding period. Sales to China represented 24% of gross sales and witnessed a significant increase of 104% on pcp, as the company boosted its exports by shipping products by sea container to its strategic partners, including Alibaba and the Beingmate Joint Venture. In the home market, the company expanded its activity by 140% as compared to the prior corresponding period, with sales in Australian accounting for 64% of gross sales for the quarter. Moreover, the company delivered significant progress on its plan to be on-shelf in 700 Woolworths stores in May 2020 and began ranging the Bubs Organic® Grass Fed Infant Formula in 200 Woolworths stores in March 2020. Other markets apart from Australia and China contributed to 12% of gross sales for the quarter, with brilliant growth of Bubs® Infant Formula into Vietnam. Overall, the company witnessed growth across all channels and key partners and is optimistic about continued growth on the back of the rising demand for its products.

New Supply Agreement with Woolworths: The company has recently announced that it has entered into a new supply agreement with Woolworths which is expected to materially add to the company’s domestic revenues. This new updated agreement reinforces the confidence which Woolworths has in the company’s brand portfolio. Under the new agreement, BUB® Goat Milk Infant Formula store representation will increase more than threefold to 400 stores.

Future Expectations and Growth Opportunities: The company is likely to experience strong growth in the key domestic retail space owing to its partnership with Chemist Warehouse group and the activation of its corporate Daigou partnership. It also anticipates a further improvement in its gross margin as it is continuously working on reducing product costs and optimizing the product and channel mix. BUB is harnessing the power of top Mother & Baby Social Influencers to engage with Chinese millennial parents and is working on building deeper connections. The new supply agreement with WOW is all set to double retail exposure for the company. BUB is continuing to explore and develop market entry strategies for other opportunities in SE Asia. The company continues to be fully focused on ensuring a responsive integrated supply chain to the increased demand through all channels..png)

Key Valuation Metrics (Source: Thomson Reuters)

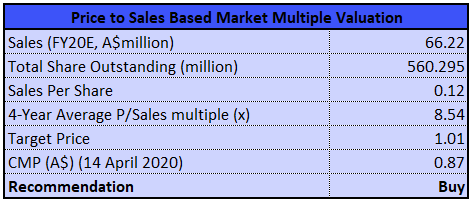

Valuation Methodology: Price to Sales Based Market Multiple Valuation

Price to Sales Based Market Multiple Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of BUB gave a return of 33.91% in the past one month and is trading below the average of its 52-week low and high level of $0.40 and $1.615, respectively. This offers an excellent opportunity for the investors to enter the market. BUB is operationally flexible and has a strong balance sheet and has delivered a record quarterly revenue building on strong underlying sales momentum established in the second quarter. The strength of the business model and its agility to continue to meet the needs in the rapidly changing environment is expected to boost the company’s long-term growth. It has put in all measures to sustain continued security of its supply chain to meet increased demand because of COVID-19. It has increased its capacity and is working to expand its inventory cover. Considering the trading levels, improvement in margins, company’s resilience in the changing market environment and decent outlook, we valued the stock using Price to Sales based market multiple valuation method and have arrived at an indicative target price offering a growth of lower double-digit (in percentage terms). Hence, we recommend a ‘Buy’ rating on the stock at the current market price of $0.870, up by 12.987% on 14 April 2020, owing to its recent quarterly results.

.png)

BUB Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...