Kalkine has a fully transformed New Avatar.

Company Overview: BSA Limited (ASX: BSA) is a national provider of contracting services to subscription TV and telecommunication companies which require satellite and telecommunication installation services, and delivery of infrastructure projects, services, and equipment to the Building Services industries. The Group is organized into three segments, namely BSA | Connect, BSA | Build and BSA | Maintain. BSA | Connect provides contracting services to the telecommunications, whereas BSA | Build provides the design and installation of building services for commercial and industrial buildings. BSA | Maintain provides the maintenance of building services for commercial and industrial buildings including: Mechanical Services, Air Conditioning, Heating and Ventilation, Refrigeration and Fire services..png)

BSA Details

Improvement across All Key Metrics: BSA Limited (ASX: BSA) is a national provider of contracting services to subscription TV and Telecommunication companies. As on 26 June 2020, the market capitalization of the company stood at ~$123.17 million. FY2019 was a successful year for BSA Limited, wherein it reported improvements across all key financial metrics for continuing operations. During the year, revenue of the company went up by 9.7% to $469.5 million, from $427.9 million in FY18 whilst EBITDA witnessed an increase of 13.7%, from $19.2 million in FY18 to $21.8 million in FY19. This resulted in an increase in NPAT from continuing operations to $10.8 million, up from $8.8 million. FY2019 has seen the successful development of BSA’s commercial solar capabilities delivering several projects across the health, education and retail sectors.

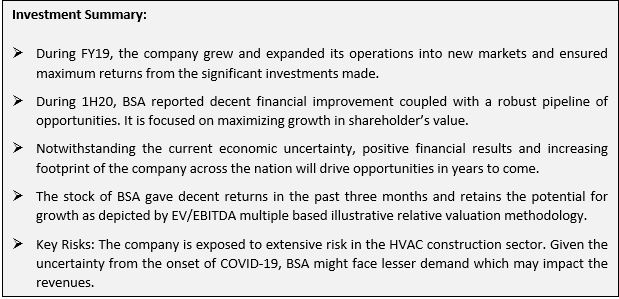

During FY19, BSA rejuvenated its finance function, and the refreshed financial management team has driven a keen focus on key aspects of cash management. During FY19, operating cash inflow increased by 289.4% to $18.3 million and Net Cash at year end was $16.3 million. The BSA | Connect business unit performed well, achieving consecutive record years in terms of revenue and profit whilst BSA | Maintain streamlined operations and generated tangible cost efficiencies. During the year, the company grew and expanded its operations into new markets and ensured maximum returns from the significant investment. The company has yielded results with several contract awards in new and existing markets.

During 1H20, BSA reported strong financial improvement coupled with a robust pipeline of opportunities. During the half-year, the company integrated its strategy to expand its building controls and evolved its technology solutions to drive efficiencies for clients. The company has favorable markets with strong relationships with key clients and hence is well-positioned for long term partnerships.

The growth plans of the company are based on end-to-end service provision across Telecommunications and Property Asset Management. Performance of the company was improved because of the strategy to refocus the business to meet the challenging external environment.

FY19 Financial Highlights (Source: Company Reports)

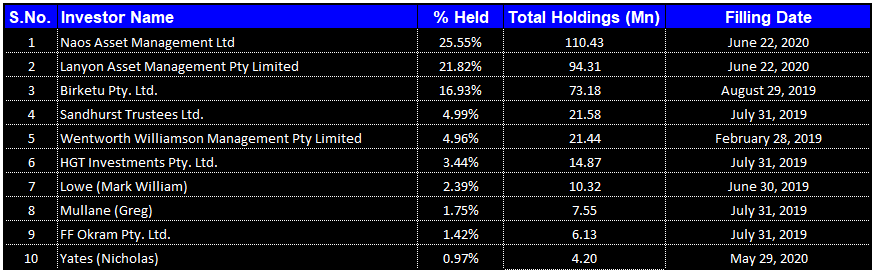

Details of Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of BSA Limited. Naos Asset Management Ltd is the largest shareholder in the company, with the percentage holding of 25.55%.

Top 10 Shareholders (Source: Refinitiv, Thomson Reuters)

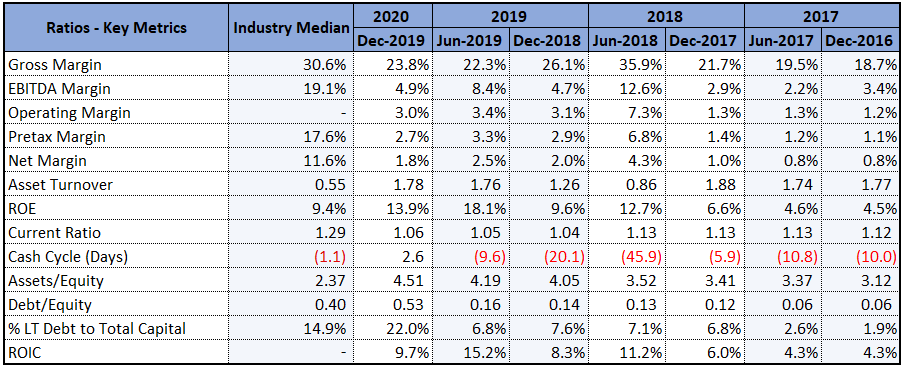

Well Management of Costs and Increasing Returns to Shareholders: During 1H20, gross margin of the company witnessed a slight improvement on the previous half and stood at 23.8%, up from 22.3% in 2H19. In the same time span, net margin of the company went up to 1% from 0.8% in 1H17. The improvement in the gross and net margin shows that the company is well managing its costs and is capable of converting its revenue into profits. During the half year, EBITDA margin of the company stood at 4.9%, up from 4.7% in 1H19, indicating increased profitability. In the same time span, Return on Equity of the company stood at 13.9%, higher than the industry median of 9.4%. This shows that the company is well managing the capital of its shareholders and is capable of generating profits internally. During 1H20, current ratio of the company stood at 1.06x, up from 1.04x in 1H19. This shows that the liquidity of the company is improving and it is capable of paying off its current liabilities using its current assets. In the same time span, Assets/Equity Ratio of the company was 4.51x, and Debt/Equity Ratio of the company was 0.53x.

Key Margins (Source: Refinitiv, Thomson Reuters)

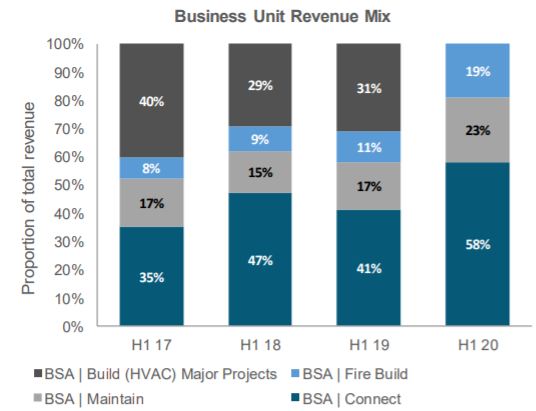

Half Year Results: During 1H20, the company reported strong performance from its continued operations with an increase of 30.4% in revenue to $258.9 million and a growth of 39.1% in EBITDA to $12.8 million. This was mainly due to the growth in Connect and Fire Build operational streams. Higher revenues and EBITDA resulted in an increase of 17.5% in reported NPAT to $4.7 million, which further resulted in a growth of 14.3% in EPS to 1.084 cps from continuing operations. During the half-year, the company reported recurring revenue of 81% following the divestment of HVAC Build Major Projects. Strong recurring revenue growth was underpinned by key contract wins in National Maintenance Contracts and the extension of nbn. During the half-year, the company reported an operating cash conversion of 66% and net cash of $15.2 million. BSA continued to report organic growth and expanded its investment into an operating model to unlock the next phase of growth. It has a robust order book across all core business units and has a strong client appetite for multi-service national maintenance contracts. BSA is further expanding into South Australia, Northern Queensland, and Tasmania to increase its National footprint.

Change in Revenue Mix (Source: Company Reports)

Key Risks: Construction contracts of the company are accounted based on estimated costs and date of completion. Variations in contract work and claims are probable and may pose some risks. The group is also exposed to various risks including credit risk, market risk, interest rate risk etc. However, the group has entered a variety of derivative financial instruments to manage its exposure to interest rate risk, including interest rate swaps. Given the uncertainty from the onset of COVID-19, the company might face lesser demand for its services which may impact the revenues.

Future Expectations and Growth Opportunities: The company has recently upgraded its guidance for FY20, wherein it expects revenue from continuing operations to be in the range of $475 million to $485 million. It also anticipates EBITDA from continuing operations to be in between $22 million to $23 million. BSA continued to witness a resilient performance from its Connect and Fire Build Business Units but has seen some slow down and deferral of discretionary work within its Maintain business unit. BSA is focusing on working capital and has retained a strong cash position with no material impact on receivables or other working capital because of the pandemic.

Given decent trading, improved certainty and BSA’s proactive focus on managing its working capital, the company is expecting to pay its interim divided on 8 July 2020, which was earlier deferred until October 2020. It also expects that all near term dividends will be fully franked. The company is maximizing growth in shareholder value. The core markets have strong demand and BSA is well-positioned for future organic growth. It maintains a significant franking credit balance of $13.9 million and is considering a range of capital management options to release franking credits.

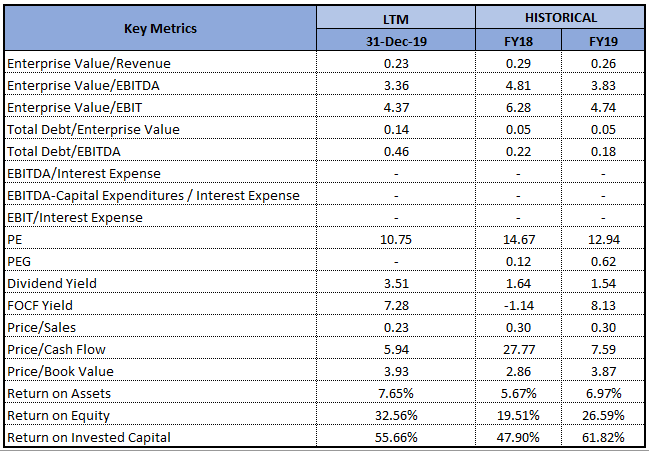

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

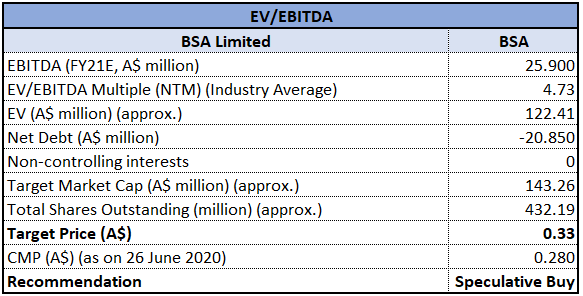

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

EV/EBITDA Multiple Based Relative Valuation Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Notwithstanding the current economic uncertainty, positive financial results and increasing footprint of the company across the nation will drive opportunities. It is focusing on strong operational ground performance within existing core contracts to secure partnerships over the long-term and is implementing new fields service management solution to optimize business and client outcomes. The company has a decent platform for growth and is converting opportunities within adjacent sectors. As per ASX, the stock of BSA gave a return of 21.28% in the past three months and a return of 11.76% in the past one month. The stock is trading close to its 52-weeks’ low level of $0.230, proffering a decent opportunity for the investors to enter the market. We have valued the stock using EV/EBITDA multiple based relative valuation method and have arrived at a target price of lower double-digit upside (in percentage terms). Considering the attractive trading levels, decent returns in the past three months, financial resilience despite the global pandemic and guidance for FY20, we recommend a ‘Speculative Buy’ rating on the stock at the current market price of $0.280, down by 1.754% on 26 June 2020.

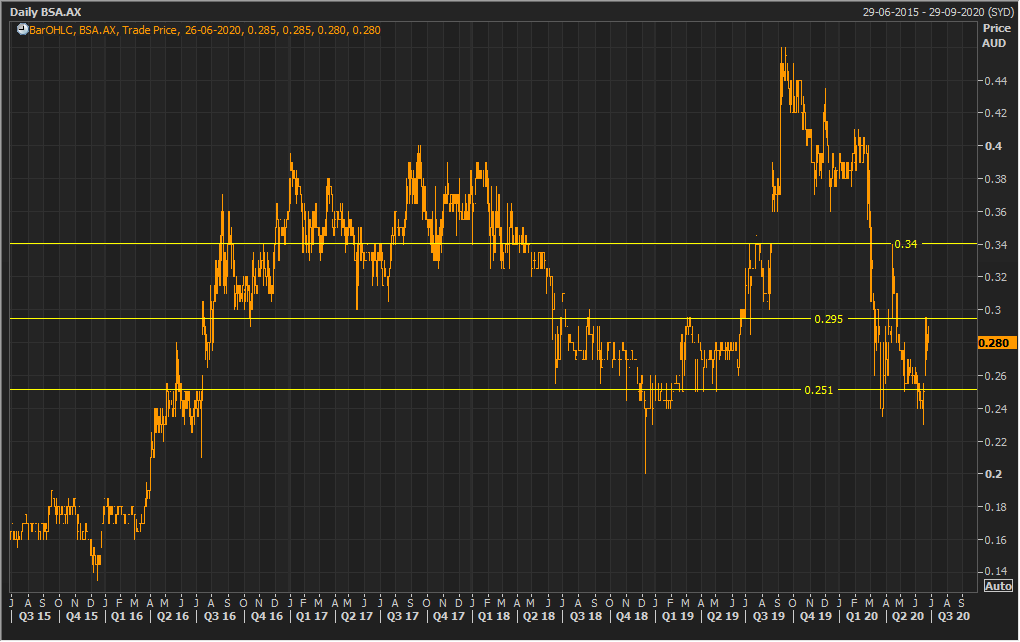

BSA Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...