Kalkine has a fully transformed New Avatar.

Company Overview: Bravura Solutions Limited provides software products and services to clients operating in the wealth management and funds administration industries in the Asia-Pacific and Europe, Middle East and Africa regions. The Company's software products and services support the front-office, middle-office and back-office functions needed to manage and administer financial products across investment product sand wrap platforms, superannuation, pension and retirement products, life insurance, private wealth and portfolio administration. It operates across two segments: Wealth Management, which provides software and services that support back-office functions relating to the management of investment products and wrap platforms, superannuation, pension and retirement products, and life insurance, and Funds Administration, which supports back-office administration requirements for a range of investment managers, custodians and third-party administrators for both retail and institutional customers.

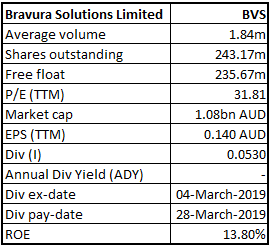

BVS Details

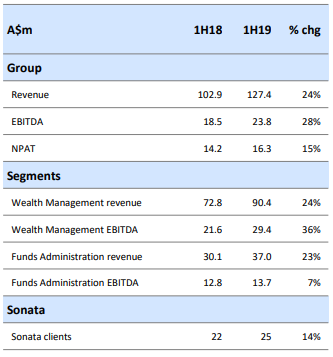

Remarkable Growth Across All Key Metrics: Bravura Solutions Limited (ASX: BVS) is engaged in the development, licensing and management of highly specialised administration and management software applications. The company is also involved in the provision of professional consulting services for the Wealth Management, and Funds Administration sectors of the financial services industry. The company has 12 offices across eight countries in APAC and EMEA. In addition, it operates development and support centres in the United Kingdom, Poland, India, Australia, New Zealand and South Africa. Moreover, the company has strong clientele base and it offers its services to 350 direct and indirect blue-chip clients including Fidelity International, Fidelity Life (NZ), Partners Life, Suncorp, STANLIB Wealth, Bank of New York Mellon, Lloyds, Citi, and Westpac NZ. Coming to the segment-wise contribution, in 1H19, revenue from the Wealth Management contributed ~71% of the Group revenue, whereas Fund Administration segment accounted for the rest 29%.Looking at the performance over the period covering FY14 to FY18, the company witnessed 13.1% top-line CAGR growth with FY14 revenue amounting to $135.5 million and FY18 revenue amounting to $221.5 million.In addition, the company reported an 87.5% yoy growth in revenue during FY18, with FY17 profit of $14.4 million and FY18 revenue of $27 million. During the first half of the financial year, the company reported revenue amounting to A$127.4 million, up 24% on prior corresponding revenue of A$102.9 million. EBITDA for the period amounted to A$23.8 million as compared to A$18.5 million in the prior corresponding period. NPAT for the period also reported a rise of 15% at A$16.3 million in 1HFY19 and A$14.2 million in 1HFY18. Earnings per share for the period amounted to 7.6 cents per share, up 15% on the prior corresponding period.

With the strong performance seen in FY18 and 1H19 results, strong clientele base and rising demand from key markets, exuberant growth in its flagship product Sonata, strong sales pipeline, upward revision for the FY19 earnings guidance, etc., the company is well poised to grow further in years to come.

1HFY19 Key Highlights (Source: Company Reports)

Wealth Management Segment Results: Performance by the segment was characterised by strong operating leverage. During the period, the wealth management segment generated revenue amounting to A$90.4 million, up 24% on the prior corresponding period. EBITDA for the segment was reported at A$29.4 million, depicting an increase of 36% on pcp EBITDA of A$21.6 million. The segment also witnessed an increase in the EBITDA margin to 33% as compared to 30% in 1HFY18.

Performance by Sonata: Sonata, the flagship product of the company, accounts for almost all of the Wealth Management segment. The product is used by financial institutions across the globe to administer financial products such as investment, wrap platforms, life insurance, superannuation and pensions on behalf of their customers. Since FY13, revenue from Sonata has increased from $5.0 million to $122.5 million in FY18. The number of clients over the period has also increased from 3 in FY13 to 24 in FY18. Sonata’s average revenue per client in FY18 amounted to $5.1 million as compared to $1.7 million in FY13.

Sonata Growth (Source: Company Reports)

During the first half, revenue from Sonata witnessed strong growth. The company achieved two new contracts for Sonata during the period along with the implementation of new clients. In addition, the company has commenced several projects for new and existing clients for Sonata. As per the half yearly results, the number of clients for Sonata increased by 14% on the prior corresponding period to 25.

Funds Management Segment Results: During the first half, the funds management segment benefitted from increased development work arising from an enhanced contract with a key global client. Revenue from the segment was reported at A$37.0 million, up 23% on prior corresponding period revenue of A$30.1 million. EBITDA for the segment stood at A$13.7 million as compared to A$12.8 million in the prior corresponding period.

Excellent Shareholder Returns: In 1HFY19, return on equity was 28%, owing to Bravura’s consistent and long-term investment in product development, deep market knowledge and expertise, significant operating leverage and sound business model. Return on assets for the period was reported at 22%. The Board declared an interim unfranked dividend of 5.3 cents per share, representing 70% of the EPS during the period.

Recent Updates:

(a) Substantial Shareholder: In a recent announcement to the exchange, the company updated that Vinva Investment Management became a substantial shareholder with the voting power of 5.06%.

(b) Deed with GBST cancelled: The company updated that it has not executed the Process and Exclusivity Deed with GBST Holdings Limited that was comprised of a cash offer of $3.00 per GBST share to acquire 100% of the ordinary shares of GBST. GBST did not accept the non-binding indicative offer made by Bravura, pursuant to a better proposal from SS&C Technologies, which offered a non-binding indicative proposal of A$3.60 cash per share via a scheme of arrangement.

(c) Change in Shareholding: During the financial year 2018, there was a material change in the company’s shareholding when Ironbridge Capital sold its shareholding of 47% in the company to allow a number of new investors to come in. Ironbridge Capital had made a huge contribution to the development of the company’s flagship product, Sonata.

(d) New Contracts in Wealth Management Segment: During FY18, the company was awarded long-term client contracts for Sonata in all the key markets including the UK, Australia, New Zealand, and South Africa. Revenue from the segment came in at $155.1 million, posting a growth of 26% for FY18 with EBITDA growth coming in at $52% to $46.2 million. Revenue for Sonata increased by 32% to $122.5 million during the period along with an improvement in development margins.

Key Risks and Mitigation Actions: The company’s key risks revolve around four major categories including (a) Increased competition with a number of specialist software vendors which is mitigated by investing in Sonata development to enhance the core platform and implementing employee incentives to retain key personnel. (b) Foreign Exchange risks that affect financial results. With the presence in a number of jurisdictions, the company is able to mitigate the risk of foreign exchange. (c) Domestic and international economic conditions also impact client revenue which is again mitigated through a presence in multiple jurisdictions.

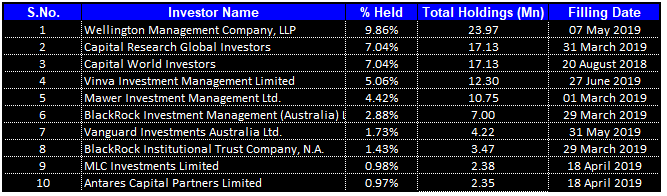

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 41.41% of the total shareholding. Wellington Management Company, LLP holds the maximum interest in the company at 9.86%, followed by Capital Research Global Investors and Capital World Investors in 7.04% each.

Top 10 Shareholders (Source: Thomson Reuters)

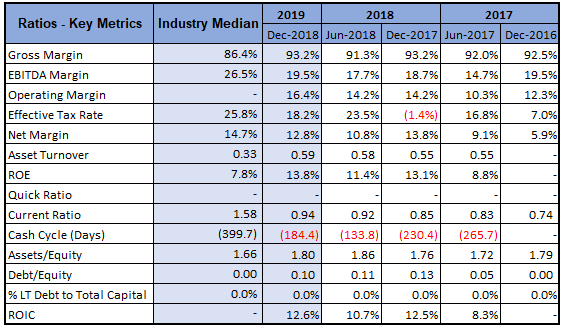

Key Metrics: For 1HFY19, the company posted a gross margin of 93.2%, which is higher than the industry median of 86.4%. EBITDA margin for the period stood at 19.5% as compared to 18.7% on the prior corresponding period.

Key Metrics (Source: Thomson Reuters)

FY19 Outlook: Going forward, the company has a strong pipeline owing to sales opportunities from new clients and significant project activity from existing clients. The business will see strong demand from the UK, Australia, New Zealand, South Africa & Asia and is well placed to take advantage of the same. The company is witnessing increased operating leverage due to strong growth, increasing scale and greater efficiency. Continued investments in Sonata are expected to support client demand and enhance product functionality. With a decent financial position in the first half, the company is well positioned to consider additional growth opportunities. As at 31 December 2018, Bravura had net cash amounting to A$14.0 million and operating cash flow amounting to A$8.0 million, representing cash conversion of 34%. The company revised the full year FY19 forecast for EPS growth to be in the range of mid to high teens.

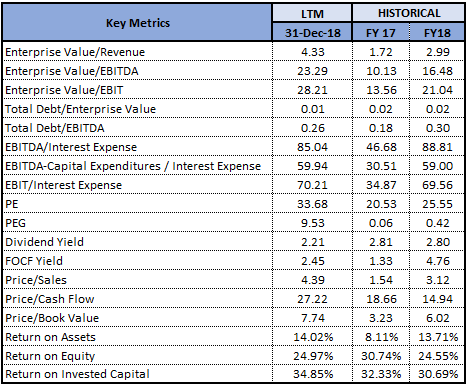

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology:

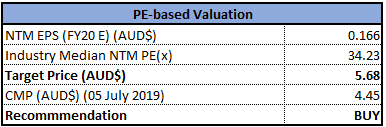

Method 1: Price to Earnings Multiple:

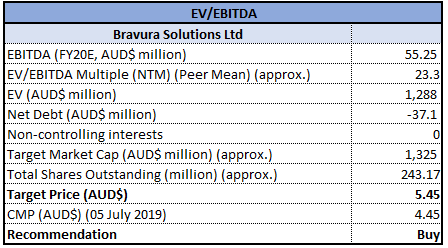

Method 2: EV/EBITDA Multiple Approach (NTM):

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Stock Recommendation: The stock of the company generated returns of -4.52% and -17.93% over a period of 1 month and 3 months, respectively. Currently, the stock is trading slightly below the average of 52 week high and low prices of around $4.61 with a beta of 1.17x (2-Years, Weekly), proffering a decent opportunity for accumulation. The six months ended 31 December 2018 was a period of outstanding growth across all key metrics. Group revenue increased by 24%, EBITDA by 28% and NPAT by 15%. The period also saw strong growth in recurring revenue of 31%, which comprised 72% of total revenue. Growth in recurring revenue was attributable to the addition of new clients and broadening of existing clients. Both wealth management and funds management segments, reported an uplift in the revenue of 24% and 23%, respectively. EBITDA margin for the wealth management segment expanded by ~300 bps to 33%, reflecting significant operating leverage. Apart from the above, the company witnessed a strong financial position during the period resulting in excellent shareholder’s returns. Pursuant to the above factors, the company also revised upward the earlier forecasted growth in EPS. Considering the performance during the first half, strong sales pipeline from new and existing clients accompanied by strong demand from key markets, growth in revenue & clientele for Sonata and the revised FY19 EPS growth guidance, we have valued the stock using two relative valuation methods, Price to cash flow and EV/EBITDA multiple and arrived at the target price of the stock in the range of $5.45 to $5.68 (double-digit upside (%)). Hence, we recommend a “Buy” rating on the stock at a current market price of $4.450, up 0.225% on 05 July 2019.

BVS Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...