Kalkine has a fully transformed New Avatar.

Company Overview: Botanix Pharmaceuticals Limited, formerly Bone Medical Limited, is a pharmaceutical company. The Company focuses on developing medical dermatology products for dermatologists and their patients. Its segments include Research & Development and Corporate. The Company's products and pipeline products are all based on drug delivery technology known as Permetrex, which helps solve the challenge of delivering active pharmaceutical ingredients across the skin. The Company's products, which are under development, are focused on modulating the body's endocannabinoid system of receptors which regulates skin function, growth and renewal. Its product pipeline includes BTX1503, BTX1308 and BTX1204. Its BTX1503 is a transdermal gel formulation used for the treatment of serious acne in adults and teenagers. Its BTX1308 is a transdermal gel formulation used for the treatment of plaque psoriasis. Its BTX1204 is a transdermal gel formation used for the treatment of atopic dermititis.

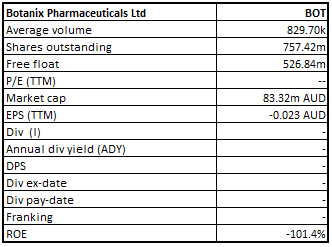

BOT Details

Significant Rise in Total Revenues: Botanix Pharmaceuticals Ltd (ASX: BOT) is a micro-cap company with the market capitalization of around $83.32 Mn as of March 01, 2019. It is dedicated towards the development of next generation therapeutics for the treatment of serious skin diseases. The company generated total revenues amounting to $4,743,690 for the half-year ended December 2018 reflecting the substantial rise of 163% on the YoY basis. Botanix is in the process of undertaking rapid development throughout three clinical programs for treating acne (BTX 1503), atopic dermatitis (BTX 1204) and psoriasis (BTX 1308). The company started BTX 1503 Phase 2 acne study in the month of June 2018 and the completion of enrolment is expected in mid-2019. The BTX 1204 Phase 2 atopic dermatitis study is also ongoing and full enrolment is expected in Q3 CY 2019. The company’s Phase 1b psoriasis patient study is anticipated to be fully enrolled by Q1 CY 2019 end and the top line data is anticipated in Q2 CY 2019. The company posted net loss after income tax of $4,181,110 for the six months ended December 31, 2018 while, in the same period of prior year, the figure stood at 2,392,381. The net loss was because of expenditure which was associated with the research and development activities and the general administration costs related with the ASX.

The company’s position in key margins got improved significantly in FY 2018 on a YoY basis thus, placing it in a better position to achieve growth. There has been substantial YoY improvement in FY 2018 in its net margins which reflects the improved capability of Botanix to convert the top line into the bottom line. From the liquidity standpoint, the company was in a better position in FY 2018 as compared to the broader industry and this is evident from its current ratio which was 12.42x and is higher than the industry median of 5.45x. It reflects that the company is in a better position to meet the short-term commitments.

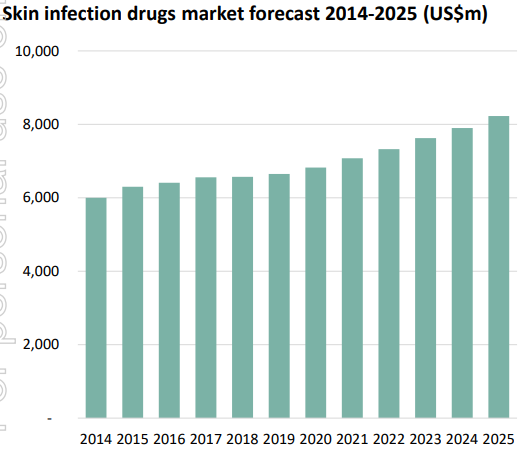

In a nutshell, it can be said that Botanix would largely be supported by the strong capital position and by its focus on making deployments towards product portfolio development. Also, broader dermatology market offers significant opportunities and market for skin infections exceeds US$6.5 billion per annum and, we believe, that the company is firmly placed to capitalize on these opportunities.

Market Forecast (Source: Company Reports)

Digging Deeper into BOT’s operations: The company’s BTX 1503 product is for the moderate to severe acne. After the enrolment of the first patient in BTX 1503 Phase 2 clinical study in the month of July 2018, the company conducted investigator’s meeting in July 2018 so that details and protocol of study can be discussed. The meeting got positive feedback with respect to the data from Phase 1b study, the planned patient recruitment rates as well as physician’s assessment of novel BTX 1503 formulation.

The company’s BTX 1204 product is for atopic dermatitis and, in August 2018, BOT wrapped up a successful Pre-Investigational New Drug (pre-IND) Meeting with FDA, in which it confirmed its proposed development plan and data package supported Phase 2 clinical development in the United States.

The company’s BTX 1308 product is for psoriasis and, in July 2018, Botanix completed the primary pre-clinical formulation and testing work on BTX 1308 for treatment of psoriasis. These results allowed the company to progress the product into Phase 1b patient study and BOT treated the first patient in the month of November 2018.

BOT’s latest pipeline product named BTX 1801 is a novel antimicrobial which is having the potential to address the unmet needs in serious skin infections and there also significant market opportunities. In July 2018, Botanix announced the successful completion of pre-clinical testing and demonstrated that BTX 1801 was very effective at killing methicillinresistant staphylococcus aureus (MRSA) strains of bacteria when compared to Permetrex™ or cannabidiol alone. After these findings, the company signed the research agreement with The University of Queensland’s (UQ) Institute for Molecular Biosciences in July 2018.

.PNG)

Key Catalyst (Source: Company Reports)

Positive Results Received from Tioga Research for BTX 1503 Product: Botanix Pharmaceuticals had recently released the data from the independent analysis which was done by Tioga Research in which there was a comparison of BOT’s lead product for acne, BTX 1503, with other commercially available cannabidiol (CBD) creams or gels. The comparative analysis reflected that, as compared to closest comparator CBD topical product, BTX 1503 had delivered >5 times as much CBD to the epidermis and >3 times as much CBD to the dermis, and significantly more than other CBD topical creams and gels. Also, further analysis got wrapped up by Tioga Research to determine the amount of CBD in other comparator products. The results have demonstrated that BTX 1503 delivered more CBD in each dose utilized by the patients in clinical studies than an entire package of each of comparative products.

R&D Refund Supports Capital Position: The company had earlier made an announcement of receipt of research and development tax incentive cash refund which amounted to A$4,616,539 for financial year 2017/2018. The top management of the company stated that, as a result of this receipt, BOT’s capital position has strengthened, and it also allows the company to continue developing the exciting product portfolio. Moreover, they added that the refund is well timed as BOT’s team finalizes the necessary logistical and regulatory arrangement which is needed to start the BTX 1204 program in the near term.

Investigator's Meeting Boosted Management's Confidence: Botanix had also made an announcement about the successful completion of the investigator’s meeting for BTX 1204 Phase 2 atopic dermatitis clinical study with the investigating dermatologists and study site coordinators. The top management reflected favourable views seeing the level of interest at investigator’s meeting in the potential for BTX 1204 to provide novel and safe treatment for the patients with the moderate atopic dermatitis. The management’s confidence with respect to enrolment for Phase 2 study was boosted by experience and quality of study sites participating in the study and the positive feedback which they received from attendees about the potential for BTX 1204.

Significant Progress Made in December 2018 Quarter: The company had advanced Phase 2 clinical study for BTX 1503, in December 2018 quarter, for treatment of moderate to severe acne. All the US and Australian clinical sites are activated boosting the recruitment. BOT is on track to complete recruitment for study by mid-CY 2019 with data available in Q3 CY 2019. In December 2018 quarter, the company started patient recruitment for BTX 1204 Phase 2 atopic dermatitis clinical study after receipt of ethics approval in December 2018. Around 200 patients would be enrolled for 12-week randomized, double-blind, vehicle-controlled study which is being held across leading dermatology clinics in Australia, New Zealand and the US and enrolment for the study is expected to be wrapped up in Q3 CY 2019.

The company has maintained its focus on prudent cash management and this is evident from its focus towards making deployments in clinical programs development, rather than administrative overheads. At the end of December 2018 quarter, the company was possessing A$13.5 million in cash. Following receipt of R&D Tax Incentive refund, the company witnessed net cash outflows which amounted to A$0.72 million with A$4.6 million deployed towards R&D activities.

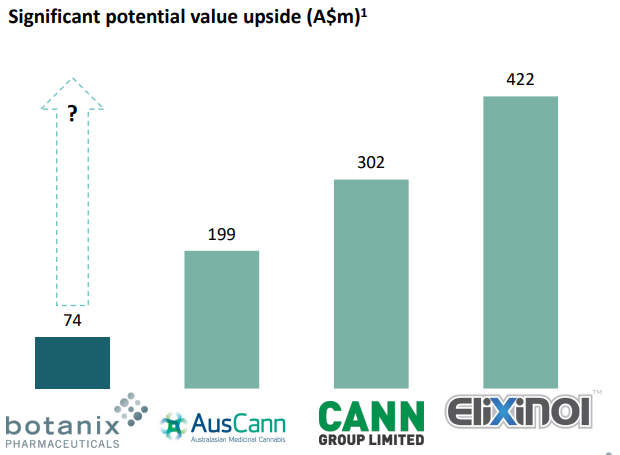

Drivers for Future: We are positive on the company at the back of huge opportunities in billion-dollar dermatology market, unmet patient needs and novel mechanism of action for skin disease. Dermatology studies are faster, and they are more cost effective in comparison to other pharmaceutical areas. It is expected that 2019 would be a transformative year which is backed by planned completion of two Phase 2 studies, a Phase 1b patient study coupled with milestones for the broader pipeline as well as Permetrex™ technology platform. The robust upside potential of the company is being underpinned by its focus towards high-value pharmaceuticals, with de-risked late-stage studies underway. The company’s primary differentiating factors include generation of positive clinical data, targeting markets with no new alternatives in 15-20 years, advanced and broadest clinical program globally, unrivaled track record and fully synthetic drug active approach which helps in avoiding FDA issues and challenges.

Significant Potential Value Upside (Source: Company Reports)

Stock Recommendation: In the last three months, the stock has risen around 41.03% as at 28 February 2019 and is trading slightly towards an average of 52-week lower and higher levels. A technical indicator, Moving Average Convergence Divergence or MACD has been applied on the daily chart of Botanix Pharmaceutical Ltd. It was noticed that MACD line had crossed signal line and moved in the upward direction after crossover signifying bullishness. From the analysis standpoint, the company has maintained a decent current ratio at 12.42x in FY18 as compared to the industry median of 5.45x. Moreover, the company is expected to be aided by a strong capital position and by its focus on using the R&D tax incentive refund towards the development of its product portfolio. Additionally, the company would be aided by its focus on prudent cash management and by opportunities which broader dermatology market offers. Based on the aforesaid facts and current trading level, we, have a “Speculative Buy” recommendation on the stock at the current market price of A$0.115 per share (up 4.545% on 1 March 2019).

BOT Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...