Company Overview: Botanix Pharmaceuticals Limited, formerly Bone Medical Limited, is a pharmaceutical company. The Company focuses on developing medical dermatology products for dermatologists and their patients. Its segments include Research & Development and Corporate. The Company's products and pipeline products are all based on drug delivery technology known as Permetrex, which helps solve the challenge of delivering active pharmaceutical ingredients across the skin. The Company's products, which are under development, are focused on modulating the body's endocannabinoid system of receptors which regulates skin function, growth and renewal. Its product pipeline includes BTX1503, BTX1308 and BTX1204. Its BTX1503 is a transdermal gel formulation used for the treatment of serious acne in adults and teenagers. Its BTX1308 is a transdermal gel formulation used for the treatment of plaque psoriasis. Its BTX1204 is a transdermal gel formation used for the treatment of atopic dermititis.

.png)

BOT Details

Execution is the key to drive the business: Botanix Pharmaceuticals Ltd (ASX: BOT) is a clinical stage medical dermatology company based in Perth, Australia and Philadelphia, PA. It is focused on developing cannabidiol-based topical drugs for the treatment of serious skin disease such as acne, psoriasis, eczema, etc. It is believed that cannabidiol could play a significant role in modulating the endocannabinoid system of receptors; potentially normalizing unwanted skin growth, reducing excessive production of oils and reducing inflammation and infection, among other functions. The group generates revenue through licensing/partnering its products or commercializing the products themselves. There is a huge time lag between product development and potential income due to the difficult FDA approvals process. That’s why, the company is aiming to significantly reduce the time required for drug approval, providing earlier opportunities for income from partnering or licensing agreements. We expect that execution of its ongoing product development is the key driver of the company to generate revenue in upcoming period.

.png)

Product Portfolio Value Consideration in the Industry (Source: Company Reports)

BTX 1503 Product - Growth Catalyst: BTX 1503 is well positioned for clinical development, following the successful completion of an oversubscribed placement in early February 2018. The BTX 1503 Phase 2 clinical trials are now fully funded and are expected to take approximately 12 months to complete. Moreover, the company successfully completed its first patient studies with its lead product, BTX 1503 for the treatment of acne in January 2018, and is now preparing for a 360 patient Phase 2 study commencing mid-2018 with completion expected in mid-2019. The BTX 1503 Phase 2 clinical trials are designed to deliver data that allows Botanix to explore licensing and other corporate opportunities. The company believes that BTX 1503 has the potential to generate similar or greater revenue of its two leading topical acne products i.e., Aczone generated revenue of US$ 456 Mn in FY16 and Epiduo recorded revenue of US$ 494 Mn.

.png)

BTX 1503 indicative Clinical Timeline (Source: Company Reports)

Completed Enrolment of BTX 1204 Atopic Dermatitis Study: Medical dermatology company, BOT has completed enrolment for its Phase 1b BTX 1204 atopic dermatitis patient study. During the trial, 36 patients received either BTX 1204 or vehicle (placebo) treatment for 4-weeks at four leading Australian dermatology clinics. BTX 1204 is focussing on the prescription atopic dermatitis market that currently generates more than US$8 Bn annual sales globally. Following the completion of the study, Botanix plans to file an IND application with the United States Food and Drug Administration (FDA), allowing a multicentre Phase 2 safety and efficacy study for BTX 1204 for potential commencement later in 2H CY2018. Currently, the company is pursuing a rapid clinical development strategy to accelerate product commercialization and timing to first generate revenues.

.png)

BTX 1204 Phase 1b Study Results (Source: Company Reports)

Product Pipeline – Long term Growth Drivers: The company has a strong product pipeline, enabled by Permetrex, that has the potential for early revenue. Currently, the company’s pipeline of products focusses on the topical treatment of serious skin diseases using cannabidiol as the active ingredient. The cannabidiol active is driven deep into the skin using a novel drug delivery technology called Permetrex. Furthermore, the company continued to advance other pipeline products that utilise the Permetrex delivery technology. The Company commenced pre-clinical studies of BTX 1308, a novel treatment for psoriasis, with pre-clinical skin data that is expected in 2Q CY2018. Following this, the company also plans to take BTX 1308 into a psoriasis patient study in 3Q CY2018. Moreover, the company undertook pre-clinical testing of a new product designated BTX 1801 which is expected to be announced early in Q3 and will follow BTX 1308 into the clinic in 2H CY2018. BTX 1701 remains under review by the Company. Hence, we expect that the company’s strong product pipeline should boost volumes in upcoming period.

.png)

Clinical programs with near term milestones (Source: Company Reports)

Quarterly Cash Flow Update (31 March 2018): The Company released its Quarterly Cashflow report for the quarter ended 31 March 2018 wherein net cash inflow recorded A$12.9 Mn, supported by the receipt of the A$1.6 Mn R&D tax incentive refund (January 2018) and the successful completion of the A$15 Mn (before cost) significantly oversubscribed placement (February 2018). During the quarter, the company invested around A$2.4 Mn in R&D activities, primarily associated with BTX 1503 and BTX 1204 clinical program. The company continued its focus on investing in the development of the clinical programs, rather than administrative overheads, and this highlights a clear focus on prudent cash management. The Company had $15.14 million in cash at the end of the March 2018 quarter. Total cash receipts during the same period were $145 k. Further, the group estimated cash outflow for the next quarter of approximately $4,330K, comprising of R&D expenses ($3,980K), staff cost ($100K), and administrative and corporate costs ($250K).

.png)

Next Quarter Cash Outflow Estimates (Source: Company Reports)

Robust Global Market: The global atopic dermatitis (AD) market is forecasted to grow at CAGR of 12.8% from circa US$7 Bn in 2017 to about US$24 Bn in 2027. BTX 1204 has significant potential to address this market opportunity. Additionally, the global prescription acne market is projected to generate revenues of over US$4.5 Bn by 2018. Epiduo, currently the top-billed prescription acne treatment, had recorded sales of over US$494 Mn in 2016. We expect that there is a large opportunity for its flagship product BTX 1503 in years ahead after execution on its ongoing development which is expected to be completed by mid-2019.

.png)

Global Atopic Dermatitis (AD) market (Source: Company Reports)

Business development and strategic partnerships: During the third quarter, the company received a cash payment for collaborations with multiple partners to utilize the Permetrex delivery technology to formulate new drugs in development. These collaborations involve undertaking early stage paid formulation work for select collaborators, which will be followed by human skin testing and product characterization work. This work helps to offset the Company’s operational costs and may also translate into future licensing opportunities for the Permetrex platform, which may provide immediate revenue and the potential for substantial revenues from milestone payments and royalties, at no additional cost to Botanix. On the other hand, the company has assembled a strong board with impressive experience in developing new drugs for the skin care market. The Company’s strong relationship with Dr. Eugene Cooper, the inventor of Permetrex and holder of its patent, sets a solid foundation for developing potential future pipeline products leveraging the Permetrex drug delivery vehicle.

Financial Highlights: FY17 was the progressive year wherein the Group executed its strategic and tactical plans efficiently. The Group raised its capital from the two sources and the total cash injections amounted to $10.9 Mn which helped the Company to build a sustainable business in the dermatology and dermatitis market. The company utilized these funds to further advance the research, development, and commercialization of products which were held by the Group. The Group reported a net loss after income tax of over $4.7 million for the year 2017 and whereas for 2016 it was $1.7 million. This increase was due to the higher R&D expenses, rise in employee cost and finance expenses during the same period. As on 31 December 17, the Group had consolidated net assets of $5,436,823(2016: 3,180,914) which included the cash balance of $5,720,514(2016: $3,651,986).

.png)

FY17 - Consolidated P&L (Source: Company Reports)

During the first half of the year, the consolidated revenue from continuing operation substantially increased by 16,406% year on year (YoY) to $1,805,276 in 1HFY18 from $10,937 in 1HFY17. However, loss from continuing operations after tax amounted to $2,392,381 in 1HFY18 from $1,246,000 Mn in 1HFY17 at the back of rising research and development expenses, professional consultant expenses and share-based payment during the same period. In February month, BOT raised A$15 Mn through a placement of shares at an issue price of 11 cents per share. This fund was slated for use in accelerating clinical development and enable broader commercialization strategy.

Stock Performance: Given the growth rate in the industry and continuous good performance in the past few years, we expect that the company has a healthy outlook. Moreover, its flagship products, BTX 1503 and BTX 1204 can be a significant catalyst for the company in years to come. Meanwhile, Gayle McGarry and Caperi Pty Ltd, a substantial holder of the Group changed its holding from 10.35 per cent of the voting power to 9.32 per cent of the voting power. Besides this, another substantial holder, Shenasaby Investments Pty Ltd, changed its holding from 10.35% to 9.34%. The current ratio stood at 4.89x in 1HFY18. During the one-year span of time, the average account receivable (days) substantially decreased from 735.9 days to 105.4 days. This represents proactive management policy towards their cash management and we expect that the company will continue the same trend in future as well. BOT stock has risen 71.88% in the last six months but was down by 12.0% in the past five days as at June 28, 2018. On the other hand, BOT needs to maintain sufficient cash reserves to fund the clinical trial program for BTX-1503 and other products. Timing is also critical for being first-to-market with a new acne formulation. As the company has stated that no new formulations have hit the acne market in over of 10 years, so, this is the advantage for the company as they bring new formulation into the market and distribute products. Further, the recent first US FDA approval of a cannabidiol product looks to be favourable for the group. Based on aforesaid facts and expectations, and current trading scenario, we give a “Speculative Buy” recommendation on the stock at the current market price of $ 0.110.

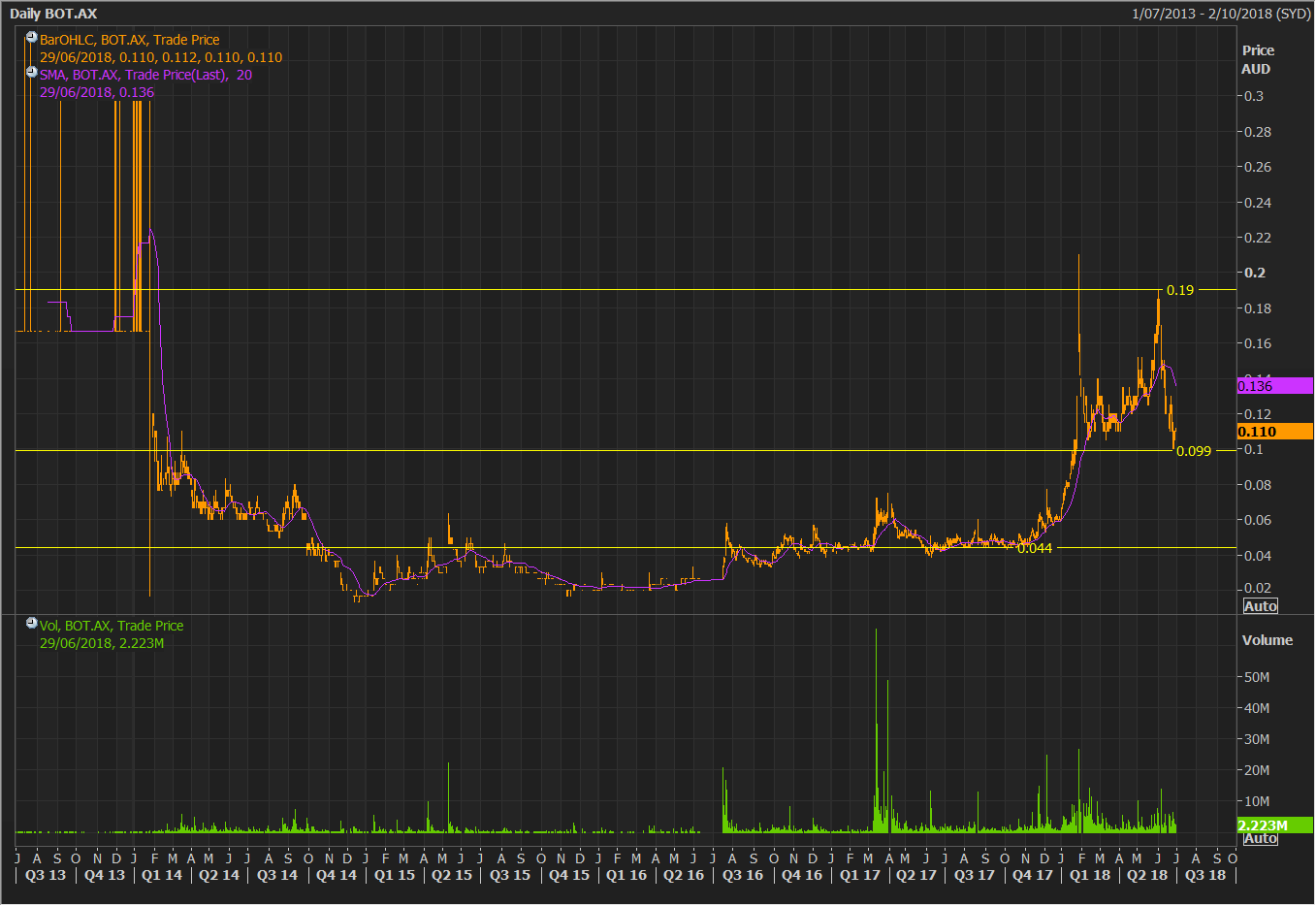

BOT Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...