Company Overview: Boral Limited is an Australia-based company, which is engaged in the provision of building and construction materials. The Company's products include ash, asphalt, blocks, bricks, cement, cement additives, cement dry mixes, concrete, decorative concrete, lime and minerals, oxides, pavers, pool surfacing, quarry products, retaining walls, roof tiles, stone, structural timber, timber cladding, timber decking and timber flooring. The Company's building solutions include infrastructure solutions and commercial solutions. The Company offers various services, including material technical services, empty pallet pick-up and roof tiling installers. Its commercial construction solutions include industrial, commercial and residential, office blocks and towers, institutional, sporting complexes, and retail and entertainment. The Company manufactures and supplies building products for factory buildings, manufacturing plants and warehouses.

.png)

BLD Details

Long-term growth story intact amidst certain challenges: Boral Limited (ASX: BLD) is an ASX listed company whose principal activities revolve around manufacturing and supplying of the building and construction materials in Australia, the USA, and Asia. As on June 27, 2019, the market capitalisation of Boral Limited stood at ~$6.05 billion. The company had made an announcement of the half-year results and there was progress with respect to the value-creating growth strategy for USG Boral. The company reported a net profit after tax before amortisation (NPATA) & significant items amounting to $224 million for the half year ended December 31, 2018, which reflects a fall of 6% than the first half of the last year. The company’s half-year results demonstrate growth from Boral North America, which was more than offset by the lower earnings associated with the divestments, as well as lower first half earnings from Boral Australia and USG Boral. The company’s net profit after tax (or NPAT) before significant items amounted to $200 million, which reflects a fall of 6% on 1H FY 2018 while its Statutory NPAT (including significant items) stood at $237 million, which reflects a rise of 37% on 1H FY 2018.

In 1H FY 2019, the company’s sales revenue stood at $2.99 billion, displaying a rise of 2% on a Y-o-Y basis. The company also highlighted half-year Headwaters synergies amounting to US$14 million against the full year target of US$25 million. On the back of respectable performance of 1H FY 2019, the company declared an interim dividend amounting to 13.0 cents per share which reflects a rise of 4% on the interim dividend of the last year. The company’s CEO & Managing Director named Mr. Mike Kane stated that the company’s results for the half-year reflect robust underlying businesses, which got weighed by the adverse weather, particularly in North America, and project-related volume delays in Australia. There are expectations that the company would deliver growth in 2H FY 2019. The company also stated that the underlying activity in the key markets happens to be solid.

Moving forward, respectable liquidity levels (as evident from current ratio) and dividend pay-out ratio might act as tailwinds for long-term growth. Also, Boral Australia’s revenue is derived from the various markets which could support the company moving forward. There are expectations that operational excellence as well as efficiency programs would be helping Boral Australia in servicing the future construction activity more cost-effectively. At CMP of $5.16, the stock of the company is trading at P/E multiple 11.97x of FY20E EPS. Despite the challenges that the group keeps on witnessing, we see a long-term growth story for Boral. Hence, considering aforesaid parameters, we have valued the stock using the relative valuation method, EV/EBITDA multiple and 1-year forward P/E market multiples (discounted ~3x to five year average considering quantitative earning scenarios related to housing market in US and Australia) to FY20E consensus EPS of $0.43 and arrived target price in the ambit of $5.6 to $5.8 (single-digit upside (%)).

.png)

Key Metrics (Source: Thomson Reuters, Company Reports)

Top 10 Shareholders: The following table gives a brief overview of the top 10 shareholders of Boral Limited:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Respectable Margins Build Confidence in BLD’s Operations: Boral Limited is having decent standing with respect to the key financial ratios as its net margin in 1H FY 2019 stood at 6.5% which reflects a marginal rise of 0.3% on the YoY basis, showing its capability to convert its top line into the bottom line. Also, the company’s operating margin stood at 9.7%, which reflects an increase of 0.8% on the YoY basis.

.png)

Key Metrics (Source: Thomson Reuters)

The company has also witnessed an improvement in its liquidity levels in 1H FY 2019 on the YoY basis as is evident from its current ratio of 1.84x, which reflects a significant increase of 49.4% that builds confidence that BLD would be able to meet its short-term obligations. Also, the company could make deployments towards key business capabilities, which could act as growth catalysts over the long-term.

A View of Cement Supply Agreement: Not so long ago, it was announced that Wagners Holding Company Limited, through a subsidiary Wagners Cement Pty Ltd, is a party to the Cement Supply Agreement with Boral Resources (Qld) Pty Limited and Boral Limited. In accordance with the CSA, BLD is required to purchase the minimum volume of cement from the company on an annual basis at the determined price.

However, later on, there was a Boral cement supply agreement update. In an update, it was mentioned that Wagners Holding Company Limited had elected to suspend supply of cement products to Boral following the receipt of the notice from BLD purporting to be a Pricing Notice issued under Cement Supply Agreement between the company and BLD. It was also mentioned that Wagners Holding Company Limited had started the formal process disputing the validity of Pricing Notice.

Signing Of Scoresby Property Agreement With Mirvac: Boral Limited had recently made an announcement that it had entered into the property development management deed with Mirvac with regards to its Scoresby site in Victoria. As per the agreement, Mirvac would be managing urban development of the 171-hectare site over the multi-decade period, including the proposed new housing community as well as substantial new parklands.

Key Takeaways From Boral Australia Investor Day Presentation: In the presentation, it was mentioned that Boral Australia happens to be a strong as well as well-positioned business and it is having diversified geographic exposure increasingly focused on the construction materials. Boral Australia is performing well, and the recent capital deployments further strengthen the positions for the future. The deployments towards excellence programs and capability have been supporting the margin growth. Also, there is a robust customer base throughout the diverse segments.

.png)

Boral Australia (Source: Company Reports)

Coming to the priorities for 2H FY 2019 with respect to Boral Australia, there are plans to reduce the costs with the help of Operational Excellence programs which includes the supply chain optimisation. It was also mentioned that 2H FY 2019 happens to be broadly in the range of the expectations and property, which is on track to deliver approximately $30 million in FY 2019, as guided. Boral Australia is focused on sustaining the strong business via capability as well as strategic deployments.

Rise in Interim Dividends Might Attract Market Players’ Attention: Boral Limited had declared an interim dividend amounting to 13.0 cents per share (franked to 50%), showing a rise of 4% on PCP basis. It equates to pay-out ratio of 76%, which is higher than the guidance range of 50-70% of earnings before significant items. The company’s operating cash flow amounted to $253 million, which reflects a rise of 17% that largely reflects lower restructuring and integration payments amounting to $19 million as compared to $82 million in the prior half year. Further, the company stated that the franking rates for the dividends are anticipated to be partially franked at or approximately 50% in line with relative earnings from Australia in the total portfolio. Also, the company’s annual dividend yield (as per ASX) stood at 5.23%, which is higher than the industry median of 4.2%, which might help the company in gaining traction of the dividend seeking investors.

.png)

Dividends Paid or Declared (Source: Company Reports)

What To Expect From BLD: In the release dated February 25, 2019, it was noted that Boral North America is expected to deliver EBITDA growth of around 15% in USD in FY 2019 for the continuing operations, which reflects volume growth, further synergy delivery, and operational improvements. The outlook of Boral North America also includes the expected Headwaters acquisition synergies amounting to approximately US$25 million in FY 2019. However, USG Boral is anticipated to deliver slightly lower profits in FY 2019 as compared to FY 2018. Boral has been progressing the strategic opportunities for the USG Boral plasterboard business but there have been assumptions that there would be no impact in FY 2019.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

With full benefit from the reduction in the US corporate tax rate, the company’s effective tax rate has been anticipated to be in the range of 21–22% in FY 2019. Also, Boral’s corporate costs are anticipated to be broadly in line with FY 2018. Overall, there are expectations that the depreciation and amortisation would be in the range of $380 million–$390 million in FY 2019. The company’s expectation for the capital expenditure for FY2019 happens to be between $425 million–450 million.

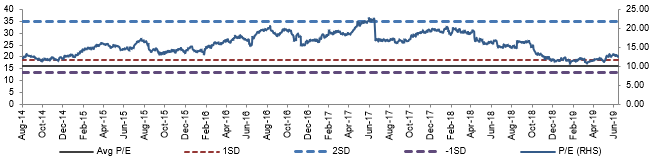

Historical P/E Band (Source: Company Reports, Thomson Reuters)

Valuation Methodology:

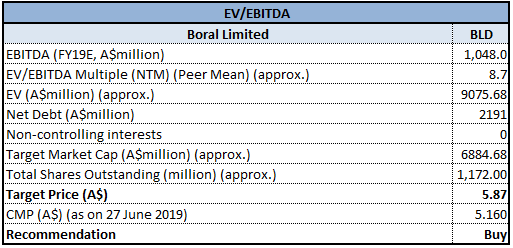

Method 1: EV/EBITDA Multiple Approach

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM: Next Twelve Months

Stock Recommendation: The stock of Boral Limited has delivered the return of 5.74% in the span of previous six months, while in the time frame of past three months, the returns stood at 13.66%, which could be considered at respectable levels and might attract the attention of market players. Also, with respect to signing of Scoresby property agreement with Mirvac, Boral anticipates to receive around $66 million of EBITDA through to FY 2026, which includes $3 million in FY 2019. The company also stated that additional significant earnings are anticipated from the development of Scoresby from FY 2027 through to anticipated project completion in 2035.

The company also anticipates Scoresby to deliver in excess of $300 million of earnings over the life of the project, subject to rezoning, which includes the removal of the existing Victorian State Government parks acquisition overlay, as well as market conditions. Also, the company’s annual dividend yield (as per ASX) is higher than the broader industry median. Based on the foregoing, we have valued the stock using the relative valuation method, EV/EBITDA multiple and 1-year forward P/E market multiples (discounted ~3x to five year average considering quantitative earning scenarios related to housing market in US and Australia) to FY20E consensus EPS of $0.43 and arrived at a target price in the ambit of $5.6 to $5.8 (single-digit upside (%)). Hence, we give a “Buy” rating on the stock at the current market price of $5.160 per share.

.png)

BLD Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...