BlueScope Steel Limited produces metal coated and painted steel building products, principally focused on the Asia-Pacific region. The Company offers a range of branded products that include pre-painted COLORBOND steel, zinc/aluminium alloy-coated ZINCALUME steel and the LYSAGHT range of building products. It operates through five segments: Australian Steel Products (ASP); New Zealand & Pacific Steel (NZPac); Global Building Solutions (GBS); Building Products ASEAN, North America and India (BP), and Hot Rolled Products North America (HRPNA). It has metallic coating, painting and steel building product operations in China, India, Indonesia, Thailand, Vietnam, Malaysia and North America, primarily servicing the residential and non-residential building and construction industries across Asia, and the non-residential construction industry in North America. It operates two iron sand mines in New Zealand. It also supplies engineered building solutions to industrial and commercial markets.

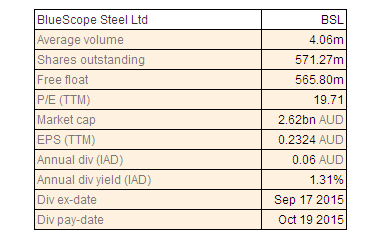

BSL Dividend Details

Growth strategies driving the bottom line: BlueScope Steel Limited (ASX: BSL) sales revenue rose by 7% year on year (yoy) to $8,571.7 million in fiscal year of 2015, driven by better export volumes in Australian Steel Products and higher volumes in Buildings North America as well as Fielders, Orrcon and Pacific Steel business acquisitions contribution. However, BlueScope reported a solid net profit after tax increase by $218.7 million to $136.3 million in fiscal year of 2015, driven by the decrease in restructure and redundancy costs. The underlying net profit after tax rose by $10.6 million to $134.1 million during the period on the back of higher spreads which would offset unfavorable revenues mix. As per the segments highlights, Building Products segment underlying EBIT rose by $9.4 million to $98.3 million in FY15 boosted by improved margins in Indonesia on the back of enhanced performance from its Indian joint venture, coupled with better cost performance and positive foreign exchange translation.

.png)

BSL Daily Chart (Source - Thomson Reuters)

Global Building Solutions underlying EBIT increased by $16.8 million to $43.7 million in FY15 driven by solid North America buildings performance coupled with better volumes and margins as well as steady performance in the China coating and painting operations. With regards to the Hot Rolled Products North America business, the underlying EBIT surged over $2.7 million to $107.3 million in fiscal year of 2015 on the back of better volumes and falling Australian dollar. Meanwhile, BSL reported that it’s ASP underlying EBIT surged by $102.8 million during the fiscal year of 2015 against FY2014 boosted by its better spread. As per the balance sheet highlights, the group’s net debt reached $275.2 million (with over $25 million attributable to non-controlling interests). BSL has an undrawn debt plus cash of $1,591.0 million during the period, indicating solid liquidity while management reported a fully franked final dividend of 3.0 cents per share during the year. Bluescope also enhanced its net assets by $282.4 million to $4,739.1 million as at June 2015 against $4,456.7 million in the prior corresponding period, as over $230 million was contributed from the translation impact of the lower Australian dollar against the US dollar.

.png)

Fiscal year of 2015 performance highlights (Source: Company Reports)

Acquisition of entire North Star: BSL reported that it is acquiring the rest of the 50% of Cargill’s North Star (NS) share for USD 720 million enabling the group with the entire 100% stake at North Star. Based on the Jacobson survey, customers identified that North Star business as a leading mini-mill in the U.S. in terms of its quality, service and on-time delivery. North Star enhanced its output to 2.0 mtpa in FY2015 from 1.5 mtpa in FY2001, and is targeting to add over 90,000 tonnes per annum of production capacity in the coming two years by enhancing casting width and speed. NSBSL sells over 80% of the combined production in the MidWest U.S., wherein over 45% of end customers are from automotive, 25% from construction, 10% from agricultural and 20% from manufacturing/industrial applications. BSL’s 50% ownership in North Star delivered around $1.1 billion of cash dividends, and BSL believes that acquiring the entire stake would enhance its cost competitiveness in steelmaking. BSL is targeting to maintain over 1.0 times net debt to EBITDA ratio within twelve to eighteen months.

.png)

Acquired full North Star (Source: Company Reports)

Solid efforts to reduce costs and focusing on premium brands to offset commodity price pressure: BSL has been focusing on reducing its costs to maintain its competitiveness as well as sustain the commodity prices pressure. The group estimates to achieve over $200 million of total permanent cost reductions in Australia, and over NZ$50 million in New Zealand, by fiscal year of 2017. The group has decided to keep its steelmaking at Port Kembla and Glenbrook. Accordingly, BSL is also seeking initiatives from the Federal and State governments like decreasing payroll tax, EPA and WorkCover costs, as well as use the EITE framework to defer carbon costs. On the other hand, management is focusing on premium branded businesses growth around the world to sustain its pricing in the current tough market conditions. Management reported that Indicative Asian hot rolled coil steel spreads have fallen below US$200 per tonne, decreasing from an average of around US$295 per tonne over the five years to 30 June 2014. Meanwhile, China reported that its finished steel exports more than doubled to over 100 million tonnes per annum since 2010-2013 period, wherein the rise is almost equivalent to the output of 20 Port Kembla steelworks. This rise in China, and improving global steel production and exports, led to steel prices and spreads pressure during the year. Meanwhile, to restore the group’s China Buildings business back to profit track, BSL is selling its 28% of stake in McDonald’s Lime Limited to Graymont Limited, for NZ$41 million and recognizing a NZ$36 million pre-tax profit.

.png)

EBITDA and Spread (Source: Company Reports)

Outlook:China is exporting an equivalent production of 45 Port Kembla Steelworks leading to a global surplus and the hot rolled coil prices have fallen to the lowest levels since 2003. Therefore, to offset this pressure, Bluescope continues to focus on cost savings in Port Kembla as well as in Glenbrook in New Zealand. With the Australian Distribution business restructuring, the group intends to achieve over $20 million per annum of cost savings by fiscal year of 2017. On the other hand, Glenbrook Steelworks in New Zealand are expected to deliver over NZ$50 million in savings. The group estimates to derive benefits from the increasing painting capacity in Malaysia. After witnessing a heavy pressure on the back of falling steel prices in second half of 2015, management estimates its North America margins to recover in the coming periods.

.png)

U.S. Midwest Mini-mill Spread (Source: Company Reports)

Stock Performance:The shares of Bluescope have delivered a negative year to date returns of over 21.19% (as of November 06, 2015) on the back of oversupply of steel coupled with commodity price volatility. On the other hand, the shares of BSL generated over 24.65% (as of November 06, 2015) returns in the last three months driven by the group’s better performance coupled with its cost cutting efforts. Moreover, BlueScope also recently reported that it entered into a three-year enterprise memorandum of agreement with unions and employees at Port Kembla. Accordingly, Bluescope reported that its employees, site management and the combined unions would deliver over $60 million per annum in labor cost savings. NSW Government is also deferring over $60 million of payroll tax payments in the coming three years, as well as decreasing other charges. The group also said that the unions approved to suspend the Port Kembla wages bonus scheme. Moreover, the group has upgraded its earnings outlook forecasts and estimates over 40% increase in underlying EBIT in first half of 2016 against second half of 2015, which is about $50 million above the previous outlook. The upgrade in guidance is mainly due to earlier than planned delivery of the group’s initiated cost reductions in the Australian Steel Products segment, as well as improving domestic demand. We believe that the improving residential volumes, coupled with the group’s cost efficiency efforts as well as falling Australian dollar would add support to the stock in the coming months. Based on the foregoing, we give a “BUY” recommendation for the stock at the current levels of $4.44

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...