Company Overview - BlueScope Steel Limited is a flat steel producer for the Australia, New Zealand and the United States markets. The Company operates in six segments: Coated & Industrial Products Australia, which includes the Port Kembla Steelworks; Building Components & Distribution Australia, which contains a network of service centers and distribution sites; New Zealand Steel operation at Glenbrook, New Zealand, produces a range of flat steel products for both domestic and export markets; Global Building Solutions segment is a supplier of engineered building solutions to industrial and commercial markets; Building Products ASEAN and North America, which operates metallic coating and painting lines and LYSAGHT roll-forming facilities. In February 2014, Hills Ltd completed the sale of Fielders and Orrcon steel businesses to BlueScope. In June 2014, BlueScope Steel Ltd acquired downstream long-products rolling and marketing operations of Fletcher Building's Pacific Steel Group.

Analysis - In this report, we are eying on BlueScope Steel Group (BSL), a leading steel producer for the domestic Australian, New Zealand and U.S. markets. The Company that operates through six reportable segments, namely, Coated & Industrial Products Australia (CIPA), Building Components, & Distribution Australia (BCDA), New Zealand & Pacific Steel Products (NZPac), Global Building Solutions (GBS), Building Products ASEAN, North America and India (BP), and Hot Rolled Products North America (HRPNA), appears to have done reasonably fair in FY2014.

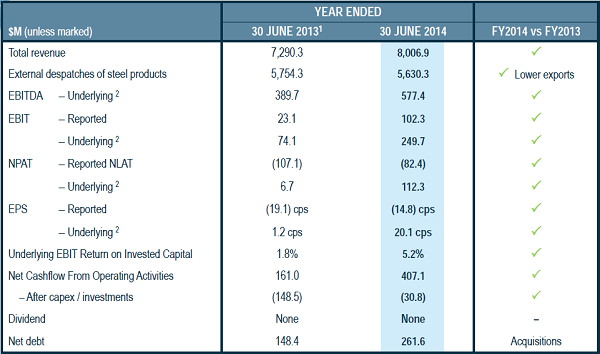

BSL reported that its sales revenue of $7,981.1M is more than that of FY2013. The increase is primarily driven by higher volumes in Australia and across other segments coupled with increased iron sands prices. The foreign exchange translation also favored the Company.

Financial Headlines FY2014 vs. FY2013 (Source – Company Reports)

Financial Headlines FY2014 vs. FY2013 (Source – Company Reports)

The NLAT was higher by $24.7M from that of FY2013, though equipoised by costs associated with restructure, redundancy, business development and acquisition. The underlying NPAT and EBIT grew higher from that of FY2013.

A view of BSL’s segments’ results showcased that the Company reported EBIT of $65.4M, which rose by $95.7M from that of FY2013 with regards to its CIPA segment. This increase was mainly resulting from enlarged AUD spread, high domestic volumes, and lower loss-making export despatches. For BSL’s BCDA segment, the underlying EBIT loss of $22.8M was reported which is slightly better than FY2013 based on better market activity and acquisitions. The NZPac segment witnessed an underlying EBIT of $74.7M, which also was an increase owing to better despatch mix, higher export iron sands volumes and increased steel spread. For BP segment, the underlying EBIT was of $88.9M, a $9.3M increase on FY2013 primarily due to better volume/mix. Similarly, the GBS segment witnessed an underlying EBIT of $18.5M which is more than than of FY2013.

BSL Daily Chart (Source - Thomson Reuters)

BSL Daily Chart (Source - Thomson Reuters)

There was a good performance for Buildings North America segment even when weather conditions were non-favorable. Earnings for BP China were high. However, Buildings Asia’s underlying EBIT was weaker than China.

For BSL’s HRPNA, EBIT of $104.6M, which is $37.9M up from that of FY2013 was witnessed.

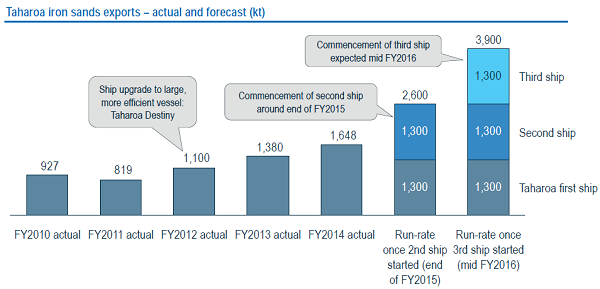

Net debt for BSL as at 30 June 2014 was $261.6M and strong liquidity was noted. The Company confirmed that its second and third iron sands export ships are on track with regards to the timeline of commencement near the end of FY2015 and the middle of FY2016 respectively.

The recent acquisitions, including the Orrcon and Fielders from Hills Holdings; OneSteel sheet and coil distribution assets; and downstream long-products rolling and marketing operations of Pacific Steel Group in New Zealand appear to contribute beneficially.

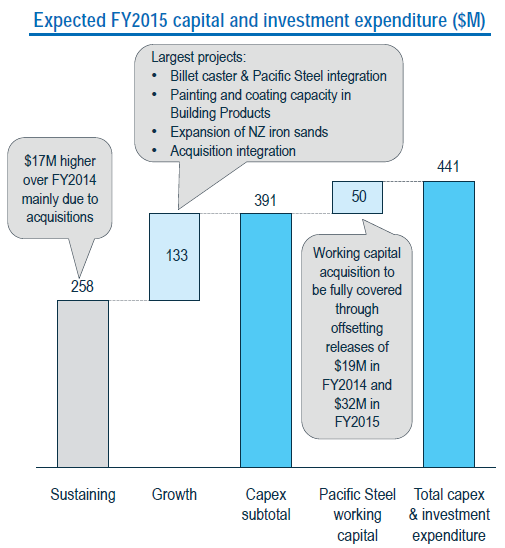

The Company further announced for investment of approximately NZ$50 million by New Zealand Steel in the construction of a billet caster and associated plant at the Glenbrook steelworks. Write-downs in Distribution Australia ($52.1M), Buildings Australia ($15.6M) and Water Australia ($12.7M) were also noted in addition to the fixed asset write-off ($7.2M) in CIPA and full reversal of prior period impairment write-downs in Coated China ($88.1M).

.png) Net Working Capital (Source – Company Reports)

Net Working Capital (Source – Company Reports)

The Company is known to have famous brands such as pre-painted COLORBOND® steel, zinc/aluminium alloy-coated ZINCALUME® steel and the LYSAGHT® range of building products, and has a widespread footmark in metallic coating, painting and steel building product operations in China, India, Indonesia, Thailand, Vietnam, Malaysia and North America.

There was no dividend declared for FY2014. The Company’s Board professed that good turnaround and progress appear to facilitate and set foundation for a future return to paying dividends.

Increase in inventory value and increase in the value of current receivables principally due to acquired businesses; value of property, plant and equipment; foreign exchange fluctuation gains; increase in the value of payables due to deferred purchase price for Pacific Steel; and increase in net debt, mainly led to decrease in net assets by $3.6M to $4,457.7M as at 30 June 2014.

As per the Company’s outlook, the Company expects first half FY2015 underlying NPAT in coherence with that of second half FY2014. 1H FY2015 is expected to have gains from intensifying domestic margins; profitable acquisitions; restructuring efforts in China; and growth in North America. Further, Company’s efforts such as Taharoa iron sands exports expansions are also on-track.

Taharoa Iron Sand Exports (Source – Company Reports)

Taharoa Iron Sand Exports (Source – Company Reports)

The only factors to be of concern remain poor iron ore prices reducing New Zealand iron sands revenue, the unsettled political situation in Thailand and normalization of the underlying tax rate.

Capital and Investment Expenditure (Source – Company Reports)

Capital and Investment Expenditure (Source – Company Reports)

The Company’s strategy is to emerge as a leading international supplier of steel products and solutions with a focus on the global building and construction markets. At the same time, the Company aims to obtain maximum value from existing steel operations in Australia, New Zealand and North America. For this, BSL is putting efforts to fast-track growth in engineered building solutions (EBS). The Company intends to grow across Asia-Pacific with a portfolio of highly competitive and locally manufactured finest-quality sustainable products. BSL also targets to exploit growth opportunities in the North American hot rolled products business.

From the downfall in FY2009, the Company’s strategy in restructuring and taking other initiatives in recent years has allowed BSL to come back to some better times. Nonetheless, the Company needs to continually take steps to manage market, operational, financial, cultural, and governance risks. Further, the Company belongs to an industry which is cyclical in nature, and is also subtle to the price trail of international steel products and raw material prices. Exchange rate fluctuations may also impact the financial prospects.

Coated & Industrial Products Australia - Despatch Mix (kt) (Source – Company Reports)

Coated & Industrial Products Australia - Despatch Mix (kt) (Source – Company Reports)

However, we opine that with BSL’s operational improvement; overall performance upsurge due to acquisitions based on higher volumes steered through such acquisitions; and continually increasing demand and planned maintenance speak of some prolific results that are underway for the Company. Further, Company’s CIPA planned maintenance program is progressing well. Specifically, the blast furnace stave replacement program continues in FY15. The Company expects to exceed 15% EBIT ROIC hurdle and be EPS accretive in FY2015 in view of the Fielders and Orrcon acquisition, and the OneSteel Sheet & Coil acquisition. There is also a likelihood that steel spread witnesses an improvement. The efforts such as new management team at Indonesia may help BSL address the underperformance in said region. Also, a few issues such as fire at Bluescope’s Port Kembla Sinter plant, and gas flow diversions were taken care appropriately by the Company recently.

New Zealand & Pacific Steel Products - Steel Despatch Mix (kt) Excluding Pacific Steel Long Products (Source – Company Reports)

New Zealand & Pacific Steel Products - Steel Despatch Mix (kt) Excluding Pacific Steel Long Products (Source – Company Reports)

Similarly, the Pacific Steel Group downstream business is expected to pay returns within three years from transfer of billet production to Glenbrook (around 1H FY2016). BSL also believes to capture higher residential construction volumes by virtue of increased construction activity. For instance, BIS Shrapnel and HIA are expected to forecast 7.5% and 1.8% growth in residential construction in FY2015.

Accordingly, we put a

BUY recommendation for this stock at the current price of $5.11.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...