Company Overview: Bingo Industries Limited is an Australia-based waste management and recycling company. The Company provides environmental and waste management solutions across the waste management supply chain. Its services include Skip Bins, Commercial Waste, Liquid Waste, Recycling Centres, Contaminated Soils and Education. It provides all types of skip bins to residential, building or construction job. Its Commercial Waste services include front lift bins, rear lift bins, compactors and infrastructure services, specialty bins, diversion from landfill and resource recovery service, and account management and education services. Its liquid waste service categories include septic, liquid and hazardous, industrial, and cooking. It operates waste recovery facilities across New South Wales. Its centers produces recycled products, such as recycled soil, recycled bedding sand, recycled aggregate and recycled road base. The Company also specializes in the disposal of contaminated soils for any size project.

.png)

BIN Details

Decent Top-line Growth in 1HFY19: BINGO Industries Limited (ASX: BIN) is a small-cap Australia-based waste management and recycling company with the market capitalisation of ~$1.2 Bn as of 21 May 2019. The company had earlier released its results for 1H FY 2019 ending December 2018 in which its net revenue witnessed a rise of 25.4% on YoY basis and stood at $178.7 million because of robust growth in the organic revenue while its underlying EBITDA rose by 4.1% and stood at $45.6 million. The company has maintained a robust balance sheet and flexibility to fund growth, with operating free cash flow of $47.2 Mn as on 31 December 2018 which might act as a tailwind for the company moving forward. In 1H FY 2019 results presentation, the company added that they have solid work in hand which is being supported by recent contract wins as well as growing pipeline of the project opportunities particularly in the social infrastructure. With respect to 1H FY 2019, the company had maintained an interim dividend amounting to 1.72 cents per share. Strong infrastructure pipeline, continued economic and population growth, and growing waste generation are some of the growth drivers which might support the company moving forward.

.png)

1H FY 2019 Financial Summary (Source: Company Reports)

The company’s business has been generating robust free cash flow in order to support growth. However, exposure to cyclical end-markets and higher regulatory compliance are some of the factors which might act as headwinds for the company. The company remains focused on executing on its strategic priorities wherein strategic enablers are (1) protect and optimise the core, (2) geographic expansion, and (3) enhanced vertical integration. The scope to build market share in Commercial & Industrial business, sustained overall construction activity, maturity of Australian waste market and supportive regulatory environment with respect to recycling are some of the factors which might support the group moving forward.

Top 10 Shareholders: The following table gives a broad overview of the top 10 shareholders of BINGO Industries Limited:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Decent Standing in its Key Margins: BINGO Industries Limited is having a decent standing with respect to its key margins as its net margin stood at 12.7% in FY 2018 which implies a rise of 3.2% on YoY basis, reflecting an improved capability to convert its top line into the bottom line. In 1H FY 2019, its net margin stood at 7.6%. Also, its gross margin stood at 52.2% in 1H FY 2019 which is higher than the industry median of 39% which reflects that the company is in a better position to address its operating expenses as compared to the broader industry.

.png)

Key Metrics (Source: Thomson Reuters)

BIN is having a current ratio of 2.33x in 1H FY 2019 which is higher than the industry median of 1.31x, displaying the decent liquidity levels that might help it to address short-term obligations. Also, the company’s Assets/Equity ratio stood at 1.14x which is lower than the industry median of 2.44x. Further, the company is able to convert its stock to cash more efficiently than its peers as it has a better than industry cash conversion cycle of negative 1 days as compared to the industry median of 15.7 days.

Overview of Macquarie Australia Conference: Recently, in Macquarie Australia Conference presentation, the company stated that the DADI acquisition got formally completed in the month of March 2019 and it was a catalyst for Bingo’s announced network reconfiguration in NSW. It was also mentioned that integration is underway and there are expectations that it would take up to two years to fully integrate two businesses. Coming to the acquisition strategic rationale, the primary points to note are that the acquisition diversifies BIN’s product offering and it is anticipated to deliver $15 million of annualised cost synergies. With respect to BIN’s network reconfiguration, it was mentioned that there has been significant capital expenditure investment on Bingo’s initial network upgrade program which amounted to $140 million and the program happens to be largely complete while the earnings are anticipated to flow from FY 2020.

.png)

BIN and DADI’s Combined Operating Footprint (Source: Company Reports)

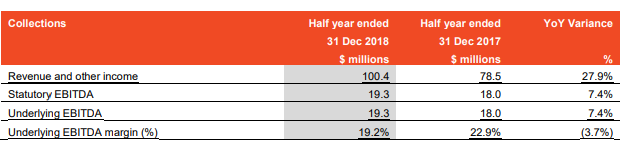

Increased Collections Fleet, Victorian Operations Supported BIN’s Collections Segment: BINGO’s collections segment posted revenue and other income amounting to $100.4 million which implies a rise of 27.9% on YoY basis which was mainly due to BIN’s increased collections fleet throughout both Bingo Bins and Bingo Commercial waste streams and full period contribution from Victorian operations. The EBITDA margin of collections segment got impacted by the softening residential construction which resulted in the pricing pressure in the months of November and December 2018. The Commercial and Industrial business has been witnessing robust growth and it presently comprises 25% of collections business.

Collections Segment (Source: Company Reports)

With respect to Collections segment, the company would continue to leverage the existing operational footprint in order to target the pipeline of critical infrastructure projects, commercial opportunities as well as residential and non-residential construction. Bingo is having a strong base of infrastructure work in hand, recent contract wins as well as work to tender that is providing revenue visibility into FY 2020.

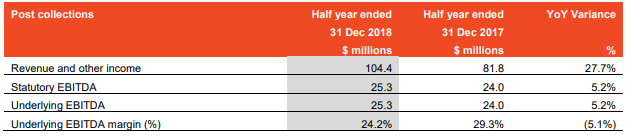

Understanding BINGO’s Post Collections Segment: Post-collections happens to be the largest contributor to the company’s revenue and EBITDA. In 1H FY 2019, this segment’s revenue witnessed a rise of 27.7% and stood at $104.4 million and its EBITDA also encountered a rise of 5.2% and stood at $25.3 million. The rise in revenues was mainly because of contributions from BINGO’s Artarmon and Campbellfield Recycling Centres and sustained growth with respect to volumes.

Post-Collections Segment (Source: Company Reports)

With respect to Post-collections, the company stated that it had deployed significantly towards the strategic network of recycling infrastructure. This deployment had positioned the company for future growth, by having the ability to process greater waste volumes and achieve resource recovery rates in excess of 75%.

Announcement of Completion of Dial-A-Dump Industries Acquisition: In the release, BINGO Industries limited stated that wrapping up of the acquisition took place after satisfying certain regulatory requirements related to the Australian Competition and Consumer Commission’s (or ACCC) approval of the acquisition. BINGO had expected to acquire DADI involving enterprise value amounting to $577.5 million. The acquisition was partially funded with the help of a $425 million underwritten entitlement offer at $2.54 per share. The proceeds from entitlement offer had been utilised towards the satisfaction of cash consideration of $377.5 million.

The scrip consideration had been satisfied by the issuance of 78,740,154 BINGO shares to vendors at an offer price of $2.54, noting that BINGO share price amounting to $1.49 reflects a reduction in the acquisition book value of around $83 million.

Valuation Methodologies:

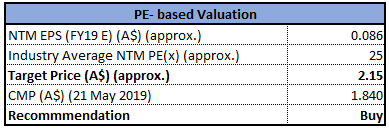

Method 1: PE- based Valuation

PE- based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

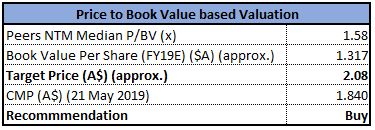

Method 2: Price to Book Value based Valuation

Price to Book Value based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

What To Expect From BIN Moving Forward: In Macquarie Australia Conference presentation, the company stated that its underlying business is on track to achieve revised FY19 EBITDA guidance and DADI business has been performing in line with the expectations. The company stated that the headwinds with regards to multi-dwelling residential construction have continued in 2H FY 2019 and are expected to continue throughout FY 2020. However, reduction in the total construction volume in the area is anticipated to be partially offset in the near term by the work in hand secured from the infrastructure projects. The growth in FY20 is expected to be mainly supported by uplift from redevelopment program, benefit from price rise, DADI acquisition as well as associated synergies. Also, the buyback had started, and it is anticipated to be earnings accretive.

As per the latest release, the company has bought back 4,687,537 shares for the total consideration of A$7,330,160.99. The company's current intention is that shares having total consideration of up to $75,000,000 would be acquired under buyback. The remaining consideration to be paid for shares with respect to the buyback is up to $67,669,839.01.

The outlook for BIN happens to be positive and construction market in NSW and Victoria is anticipated to deliver overall volumes amounting to $130 billion per annum over the span of next few years and the opportunity to significantly increase the company’s market share in C&I sector has been well indicated. Further, the management stated that FY20 is expected to be transformational for the company.

Key Valuation Metrics (Source: Company Reports)

Stock Recommendation: The stock of BINGO Industries Limited has delivered the decent return of 53.85% in the span of previous three months, while in the time frame of past one month, the return stood at 7.46% which might attract the attention of market players. Also, the company is having a solid forward order book and they have good visibility of the future revenue through the opportunities pipeline. There are anticipations that QLD levy would be positive for the business and there would be BINGO price increase early in FY 2020 in order to offset the increased operating costs witnessed in FY 2019. Also, the company’s robust balance sheet and five-year strategy would be allowing it to look towards FY 2020 with confidence. Based on the foregoing, we have valued the stock using two Relative valuation methods, P/E Multiple and Price/Book Value ratio and arrived at a lower double-digit upside growth in the next 12-18 months. Hence, considering the aforesaid parameters and current trading level, we give a “Buy” recommendation on the stock at the current market price of A$1.840 per share (up 1.099% on 21 May 2019).

BIN Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...