Company Overview: Bingo Industries Limited is an Australia-based waste management and recycling company. The Company provides environmental and waste management solutions across the waste management supply chain. Its services include Skip Bins, Commercial Waste, Liquid Waste, Recycling Centres, Contaminated Soils and Education. It provides all types of skip bins to residential, building or construction job. Its Commercial Waste services include front lift bins, rear lift bins, compactors and infrastructure services, specialty bins, diversion from landfill and resource recovery service, and account management and education services. Its liquid waste service categories include septic, liquid and hazardous, industrial, and cooking. It operates waste recovery facilities across New South Wales. Its centers produces recycled products, such as recycled soil, recycled bedding sand, recycled aggregate and recycled road base. The Company also specializes in the disposal of contaminated soils for any size project.

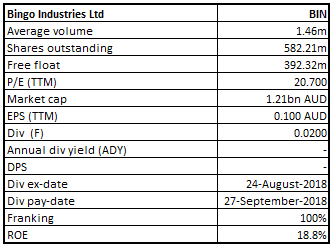

BIN Details

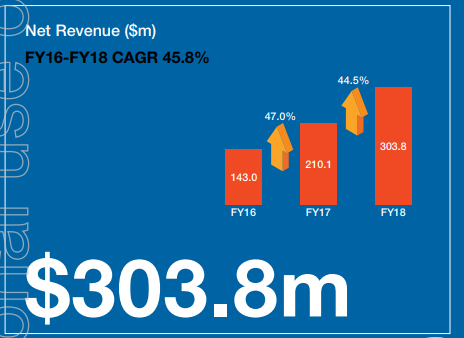

Acquisitions, Organic Growth Supported Bingo Industries: Bingo Industries Limited (ASX: BIN) is in the business of providing end-to-end environmental as well as waste management solutions throughout waste management supply chain. Mr. Daniel Tartak is the Managing Director and Chief Executive Officer (or CEO) of Bingo Industries and Mr. Michael Coleman is the Independent Chairman and Non-Executive Director. As at February 5, 2019, the company is having a market capitalization of ~$1.21 billion. As demonstrated in annual report FY 2018, the company happens to have strategic enablers which revolve around protection and optimization of the core, geographic expansion as well as enhanced vertical integration. The company had earlier reported the results for FY 2018, and the company posted net revenues amounting to $303.8 million in FY 2018, and it had witnessed CAGR of 45.8% from FY2016-FY2018. As demonstrated in the company’s annual report FY 2018, the company has been benefiting by the combination of strategic acquisitions as well as organic growth. In FY 2018, the company witnessed a rise in the network capacity to 2.2 million tonnes per annum throughout New South Wales as well as Victoria. In addition, the company stated that the company happens to be on the path of increasing the network capacity to 3.4 million tonnes per annum by FY2020 so that the rise in the recycling demand can be met. The demand happens to be on the back of unprecedented infrastructure programs in Melbourne and Sydney, rising population and diminishing landfill capacity. On the macro front, there are several positive waste market drivers like increasing urbanization, supportive regulatory environment, maturity of the Australian market as well as changing community attitudes which will act as a tailwind for future growth of the company. However, there are other favourable waste market drivers like there has been the compound growth rate of 7.8% per annum with regards to waste generation in Australia, and the recycling “crisis” is raising the profile of waste with respect to homes, organizations as well as governments. In FY 2018, the company has made progress with regards to the organic and inorganic growth strategy. The company had also led activities focused towards expansion in Victoria as well as they have enhanced the vertical integration by the acquisition of Patons Lane as well as National Recycling Group. Additionally, the company had also made an announcement related to the Dial-a-Dump acquisition. The company added that they have maintained their focus towards the extraction of the synergies from the acquisitions and towards bringing Patons Lane as well as other opportunities of development online.

Net Revenues Trend (Source: Company Reports)

Strong Position from Margins’ Perspective: Bingo Industries Limited happens to be in a robust position with regards to the margins. In FY 2018, the company posted net margins of 12.7% which reflects the rise of 3.2% on the YoY basis. In addition, the company’s net margin is also higher than the industry median of 11.5% which demonstrates the strength in the company’s top line as compared to the broader industry. The company’s EBITDA margin in FY 2018 stood at 27.8% which is higher than the industry median of 19.6%. Moreover, the company’s operating margin has improved substantially over FY 2015-FY 2018. In FY 2015, its operating margin stood at 6.4% while in FY 2018 it stood at 19.4%.

There has been an improvement in the company’s current ratio in the last four years to FY 2018 (FY2015-FY2018) which reflects that the company’s liquidity position has been improved placing it in the position to meet short-term commitments. In FY 2015, the company’s current ratio stood at 0.90x while in FY 2018 it stood at 0.97x in FY 2018.

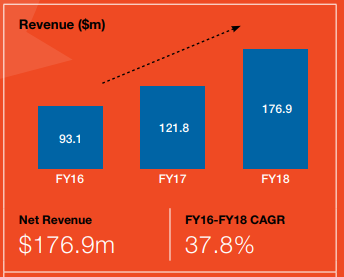

Collections Business Segment on Rise: Bingo Industries Limited’s Collections segment posted net revenues amounting to $176.9 million in FY 2018 and it has witnessed the CAGR of 37.8% from FY2016-FY2018. In FY 2018, the company’s collections fleet witnessed a rise to 254 as compared to 173 in FY 2017. The segment’s pro-forma EBITDA amounted to $41.6 million in FY 2018 which implies the rise of 48.1% on the YoY basis. With respect to collections segment, the company stated that they would be utilizing the present operational footprint so that critical infrastructure projects, as well as commercial opportunities, can be targeted with regards to residential and non-residential construction. There are expectations that favourable macroeconomic factors with respect to the collections would continue.

Collections Business Segment (Source: Company Reports)

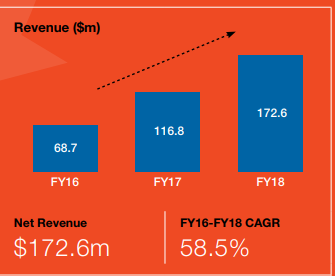

Robust CAGR Growth in Post-Collections Segment: Bingo Industries Limited’s post-collections segment’s revenues have generated net revenues amounting to $172.6 million which reflect the YoY growth of 47.7% as well as the segment’s pro forma EBITDA stood at $48.7 million implying YoY growth of 42.2% thanks to the contributions (full-year) from St Marys and Revesby facilities as well as contribution (5 months) from sites which were acquired as the part of National Recycling Group. The post-collection business segment witnessed the CAGR growth of 58.5% from FY2016-FY2018. The company had made significant investments towards the strategic network of the recycling infrastructure. As a result of these investments, the company happens to be in the healthy position when it comes to processing greater waste volumes especially when given the robust growth outlook in Western Sydney as well as infrastructure pipeline in Victoria.

Post-Collections Business Segment (Source: Company Reports)

Update Provided by BIN Regarding DADI’s proposed Acquisition: Bingo Industries Limited had issued an update with regards to its proposed acquisition of DADI (or Dial A Dump Industries). The company stated that they have offered an undertaking to Australian Competition and Consumer Commission (or ACCC) related to the response to ACCC’s SOI (or Statement of Issues). The Australian Competition and Consumer Commission would be undertaking further market consultations with regards to the proposed undertaking in addition to the continued consideration of issues which have been brought up in SOI. There are expectations that, by February 21, 2019, the final decision would be out.

Further, the top management of the company stated that they have made an offer to divest the facility which is at Banksmeadow so that the specific concern related to B&D (or Building and Demolition) processing in inner Sydney and Eastern Suburbs of the ACCC can be addressed if, as a result of this, the regulator gives final clearance for acquisition of Dial A Dump Industries to move forward.

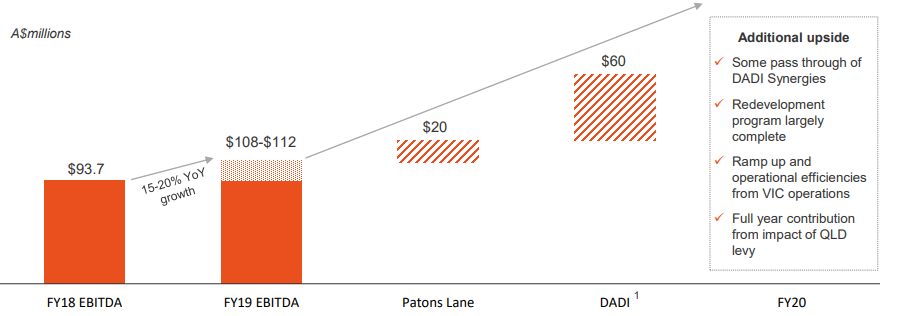

Drivers for Future: With regards to FY2019, Bingo Industries Limited had stated that the company happens to be on the path to deliver on stated guidance for FY 2019 with regards to growth in pro forma EBITDA of underlying business between 15-20%. The company stated that FY 2019 would be skewed to H2 FY 2019 because of the rise in the annual price forecast in H2 FY2019 and ramp up in the volumes as well as timing with respect to large infrastructure projects’ commencement. Moreover, another reason relates to newly built West Melbourne as well as Mortdale recycling facilities slated to be online in H2 FY 2019. Moving forward, Bingo Industries is expected to be supported by recent capital deployment towards strategic assets as well as operating footprint with regards to core growth markets having favourable prospects for the long-term.

Outlook (Source: Company Reports)

Stock Recommendation: In the last three months, the stock has been down by around 7.17% and is trading below the average of 52 weeks high and low level of ~$2.49. From a technical standpoint, a technical indicator, Exponential Moving Average or EMA has been applied on the daily chart of BIN, and default values were used for the purposes. After careful observation, it was observed that the stock price has crossed the EMA and had trended upwards after the crossover signifying the bullishness. Therefore, there are expectations that the stock might witness a rise moving forward.

However, Relative Strength Index or RSI has been applied and default values were used for the purposes. It was observed that the 14-day RSI is trending towards the overbought region. If the 14-day RSI reaches the overbought region, the stock price might witness some fall. Moreover, the company has recently disclosed the resignation of Mr. Ronald Chio as (Joint) Company Secretary of Bingo and Ms. Rozanna Lee will remain as Company Secretary of Bingo with an additional appointment to be made in due course. We are affirmative on the stock at the back of (1) respectable RoE at 18.8% as compared to industry median of 21.3% in FY18; (2) consistent track record of profitable growth with significant opportunity to scale up; (3) decent balance sheet with low debt-to-equity ratio of 0.63x in FY18 as compared to historical trend; (4) robust cash conversion cycle, etc. Besides this, the company’s post-collections segment is expected to be helped by deployments while the collections segment will be supported by the present operational footprint. Given the backdrop of the above-mentioned factors and current trading scenario, we give a Speculative Buy” recommendation on the stock at the current market price of A$2.150 per share (up 3.865% on 5 February 2019).

BIN Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...