Company Overview - BHP Billiton (BHP) is an Australia-based mining company having interests in diversified natural resources. The Company mines, extracts and produce aluminium, coal, copper, iron ore, manganese, nickel, silver and uranium, and oil and gas. The Company extracts and process minerals, and oil and gas from its production operations located primarily in Australia, the Americas and Southern Africa. The Company’s assets, operations and interests are separated into five business units, Petroleum and Potash, Copper, Iron ore, Coal and Aluminium, Manganese and Nickel. The Company’s Petroleum and Potash Business comprises conventional and non-conventional operations and a potash project. The Company’s Copper business produces copper and related ores and minerals. The Company’s Iron ore business produces iron ore. The Company’s coal business produces multiple variants of coal. The Company’s Aluminium, Manganese and Nickel business is a producer of aluminium, manganese and nickel.

Analysis - BHP Billiton Ltd has announced its operational review for the nine months ended 31 March, 2015. Group production has grown by 9% during this period with records being set for 10 operations and 5 commodities. The group remains on track to achieve its objective of 16% production growth over the two years to the end of FY 2015.

Balance of Investment & Returns (Source - Company Reports)

Balance of Investment & Returns (Source - Company Reports)

Petroleum production grew by 6% to a record 193 MMboe largely because of a 76% increase in Onshore US liquids volumes to 40.2 MMboe. Guidance remains unchanged at 255 MMboe for FY 2015.

Copper production grew by 2% to 1.3 Mt largely as a result of strong underlying operating performance at Escondida which more than offset the impact of bad weather in Northern Chile, lower grades at Antamina and a mill problem at Olympic Dam. Production for FY 2015 is now expected to be 1.7 Mt.

Consistent Dividend Growth (Source - Company Reports)

Consistent Dividend Growth (Source - Company Reports)

Western Australia Iron Ore (WAIO) production rose 16% to a record 188 Mt (100% basis) driven by continued improvements in the integrated supply chain. WAIO production for FY 2015 is now expected to be 250 Mt (100% basis). The installed infrastructure already in place continues to perform above expectations and the company is consequently deferring the Inner Harbour Debottlenecking project. This will result in a slower growth to achieve capacity of 290 Mtpa what will result in lower capital spend.

Metallurgical coal production rose by 14% to 38 Mt and represents record volumes at both Queensland Coal and Illawarra Coal. Production for FY 2015 is now expected to touch 49 Mt.

Increasing Plant Productivity (Source - Company Reports)

Increasing Plant Productivity (Source - Company Reports)

Chief Executive Officer, Andrew Mackenzie said that the commitment for sustainable improvements in productivity and lower costs is helping to cushion the adverse effects of subdued commodity prices and an helping to maintain returns for investors. In Iron Ore, the focus remains producing at the lowest possible cost with Western Australia Iron Ore unit costs now below US$20 per tonne while productivity continues to improve. Over the last decade, China’s unprecedented growth in demand provided the company with a unique opportunity which moves swiftly to develop new iron ore capacity at some of the lowest global costs to generate long-term value for shareholders and other stakeholders. Despite the increase in competition, these low-cost initiatives continue to produce attractive margins and returns through the commodity cycle.In Petroleum, the company has responded quickly to the current market conditions by reducing the number of rigs operated in the Onshore US business by 35% over the March 2015 quarter. There is a continuous review of drilling and development program and with higher oil prices forecast for the medium term, deferring development will prove to be more profitable eventually than producing today. The high-quality acreage and excellent operating performance, with among the lowest drilling costs, provides a strong platform for future growth.

Productivity Gains (Source - Company Reports)

Productivity Gains (Source - Company Reports)

The company has spun off its non-core assets into a separate company and South32 will take over 22 of BHP's 41 assets, including mines and smelters focused coal, manganese, aluminum and nickel. Most of these assets were acquired in 2001 when BHP merged with Billiton and the core company will now focus on copper, iron ore, coal, petroleum and potash. The name, South32, is derived from the location of its head office in Perth and its regional head office in Johannesburg, both of which lie on the 32nd parallel south.

High Quality Assets + Strong Margins (Source - Company Reports)

High Quality Assets + Strong Margins (Source - Company Reports)

The underlying expectation is the creation of two significant companies which are well diversified and resource rich and the simplification of the structure is expected to provide greater focus on performance and productivity improvements. Both companies will be free to adopt flexible and tailored strategies and will no longer compete for capital. Moreover, the streamlining of the organisation and increased utilisation of global service centres is expected to deliver pre-tax cost savings of around USD 100 million annually. The freedom that BHP Billiton is expected to achieve to concentrate on its top tier upstream assets (which have many common characteristics) will increase standardisation and is expected to deliver long-term productivity gains in excess of the USC 4 billion per annum which has already been targeted.

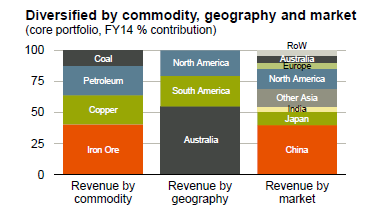

Diversification Strategy (Source - Company Reports)

Diversification Strategy (Source - Company Reports)

There are plenty of benefits for BHP Billiton which can expect to see higher growth and stronger margins from a more focused portfolio of assets. Over the last 10 years, the core portfolio has generated stronger margins and growth than the broader asset portfolio with production CAGR of 7% versus 4%, EBIT CAGR of 21% versus 15% and average underlying EBIT margin of 48% versus 41%. The core portfolio consisting of assets with very long lives provide multiple options for growth of which brownfield expansion can often provide the most attractive possible returns.

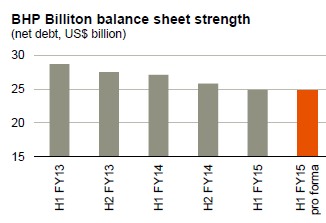

Balance Sheet Strength (Source - Company Reports)

Balance Sheet Strength (Source - Company Reports)

After the demerger, the capital structure will be appropriate to both companies. The structure for South32 was considered carefully by taking into account factors such as the nature and the scale of the business, the strategic objectives and the ease of access to capital as well as the investment grade credit rating which was targeted. The impact on BHP Billiton will be a small reduction in the net debt, a 23% reduction in the provisions for closure and rehabilitation and a reduction in employee provisions and obligations under operating leases which will be transferred.

BHP Billiton will be left with a strong balance sheet and a high-grade credit rating to provide a solid financial basis for future growth and development. Post the demerger announcement, both Moody's and Standard and Poor have reaffirmed their ratings of A1 and A+ respectively with a stable outlook. The diversification will continue from a risk point of view with broad exposure to different markets and the core businesses contributed 96% of the underlying EBIT in FY 2014.

BHP Daily Chart (Source - Thomson Reuters)

BHP Daily Chart (Source - Thomson Reuters)

Some experts feel that South32 could be an attractive acquisition for private equity companies but the sheer size of the market capitalisation makes this a daunting prospect. However, it is true that the stock has been trading at the lower end of the early expectations and we think the market may have been somewhat disappointed by the valuation placed on the assets. However, we still strongly believe that the spin-off was the right decision for both companies and will make both of them leaner and more profitable. The company is not revisiting its dividend as a result of the spin-off and the payout ratio is therefore going to be higher.

The company has had an exceptional track record in terms of dividend payments and has paid dividends every year since 1988 which is quite a record for a company that is in cyclical and volatile businesses. In fact, dividends have been increased every year over the past decade and more. We believe that the company is significantly undervalued at the current price because of the attractive dividend yield in excess of 5% as well as other factors. Despite the impact of the decline in Chinese demand and the consequent softening of commodity prices, the company still trades at a P/E ratio of around 12 times which is significantly lower than the multiple of indices such as the S&P 500. The exceptional dividend yield enhances the attractiveness of this undervalued stock to investors on top of the affordable P/E ratio. The nine months operating results to 31 March 2015 indicate that operating performance continues to be exceptionally professional and high quality.

Consequently, we have no hesitation in placing a Buy rating on the stock at the current price of $29.48.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...