Company Overview - BHP Billiton Limited is diversified natural resources company. The Company generally operates through customer sector groups (CSGs). The Company operates in nine segments: Petroleum, Aluminium, Base Metals, Diamonds and Specialty Products, Stainless Steel Materials, Iron Ore, Manganese, Metallurgical Coal and Energy Coal. As of June 30, 2012, the Company was working in more than 100 locations worldwide. During the fiscal year ended June 30, 2012 (fiscal 2012), the Company total petroleum production was 222.3 millions of barrels of oil equivalent. During fiscal 2012, its aluminium had a total production in 1.2 million tones (Mt) of aluminium. In August 2011, the Company acquired Petrohawk Energy Corporation. On September 30, 2011, it acquired HWE Mining Subsidiaries from Leighton Holdings. On September 7, 2012, it announced the sale of its 37.8 % non-operated interest in Richards Bay Minerals. In May 2014, Cassini Resources Ltd acquired BHP Billiton Limited's West Musgrave Project.

Analysis - Amidst the mixed global economic environment and changing commodities demand, we capture BHP Billiton Limited (BHP) this week as it is expected to be a deep-value play.

The fall in the iron ore price of 45% from peak last year and lower Australian dollar may be of concern. However, this global resource Company’s aim has always been to create long-term shareholder value through discovery, acquisition, development and marketing. BHP’s cash generating ability coupled with its forte in diversified portfolio, and not solely, the iron segment, catches the attention as a long-term profitable target.

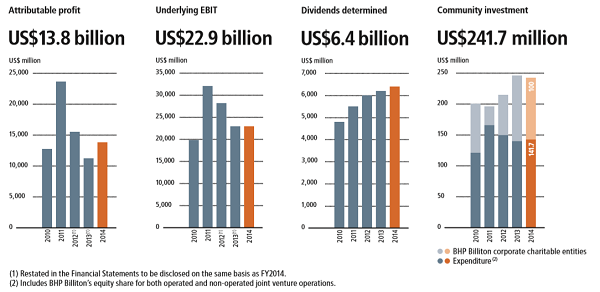

FY2014 Performance Highlights (1) (Source – Company Reports)

FY2014 Performance Highlights (1) (Source – Company Reports)

BHP’s business that spans around Petroleum and Potash; Copper; Iron ore; Coal; and Aluminium, Manganese and Nickel operates on a model that ensures efficient decision-making while being acclimatizing to changing market environments.

FY2014 Performance Highlights (2) (Source – Company Reports)

FY2014 Performance Highlights (2) (Source – Company Reports)

The Company reported attributable profit of US$13.8 billion and net operating cash flow of US$25.4 billion, which have been driven by increased production and productivity-led cost efficiencies. BHP admits that its commodities markets have been affected by the changing economic sentiments. Nonetheless, the Company is trying to leverage on the healthy though slow Chinese growth, underlying momentum in the United States and Japan.

Underlying EBIT and Profit (Source – Company Reports)

Underlying EBIT and Profit (Source – Company Reports)

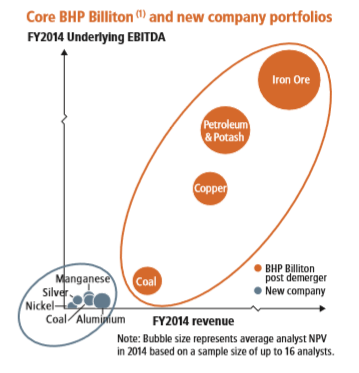

The recent announcement (on 19 August 2014) on demerging of BHP’s selected aluminium, coal, manganese, nickel and silver assets, appears to improve the productivity of the businesses with the establishment of a new global metals and mining company. The Company further declared that the shareholders will receive shares in new company while shares in BHP would be retained as such. The demerger is expected to be completed by 1H15 post necessary approvals and is estimated to be followed by either an increase or at least the sustenance of BHP’s dividend per share.

The Company would then emphasize on its long-lived assets – iron ore, copper, coal, petroleum and potash. BHP expects that it would still be the largest exporter of metallurgical coal, and one of the top producers of iron ore and exporter of copper concentrate.

BHP Billiton and New Company Portfolio (Source – Company Reports)

BHP Billiton and New Company Portfolio (Source – Company Reports)

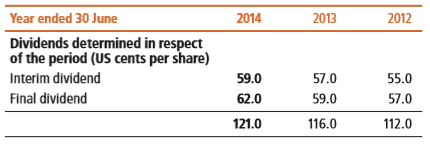

As at 30 June 2014, net debt was US$25.8 billion (down by US$1.7 billion compared last year). Further, the Company reported to have followed a progressive dividend policy year-on-year.

Dividends (Source – Company Reports)

Dividends (Source – Company Reports)

BHP has strategized its operations in order to reduce annual capital expenditure by increasing competition for capital within the Group. Specifically, BHP focused on higher quality growth and completed the high priority projects during FY14, which include but are not limited to, Macedon (Petroleum), Jimblebar mine expansion (iron ore), Port blending facilities and rail yard (iron ore), Samarco fourth pellet plant (iron ore), and Caval ridge (Coal).

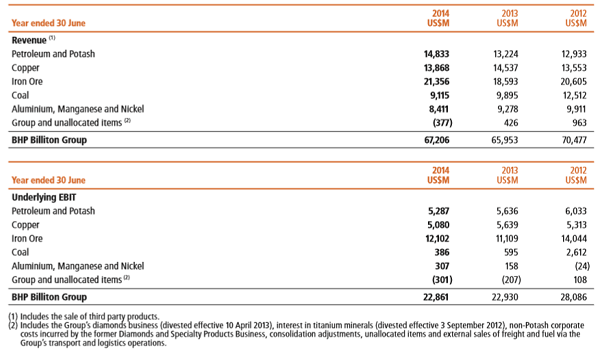

Revenue and Underlying EBIT Performance by Business (Source – Company Reports)

Revenue and Underlying EBIT Performance by Business (Source – Company Reports)

The overall production for FY2014 for the Petroleum and Potash Business was 246.0 million barrels of oil equivalent (MMboe), mainly emanating from the US and Australian operations. Copper Business yielded a total copper production of 1.7 million tonnes (Mt) in FY2014. Western Australia Iron Ore Operations at Western Australia Iron Ore (WAIO) is built on an integrated system of mines and more than 1,000 kilometres of rail infrastructure and port facilities in the Pilbara region. The focus is to have growth in capacity to 290 Mtpa. The Coal Business yielded a total metallurgical coal production of 45.1 Mt and total energy coal production of 73.5 Mt in FY2014. The Aluminium business yielded total production of 1.2 Mt for aluminium in FY2014.

According to a very recent announcement by the Management, the Company plans tocut costs at its Pilbara mines at least 25% over the medium term to less than $US20 a tonne. This will be an added advantage to BHP’s strategy.

Looking at performance data for Permian and Black Hawk, BHP’s US onshore assets indicate the possibility of achieving 200kboe/d liquids target, though slightly later than the FY17 timeline. BHP is now focusing on the Permian basin in West Texas, with the latest sold-out of the Midland basin and increased position in the Southern Delaware to 74,000 net acres. Hawkville and Haynesville are nonetheless found to experience some performance issues.

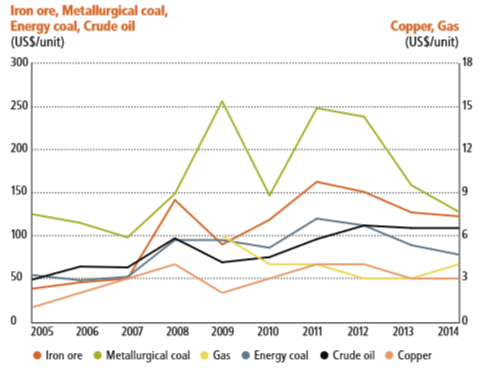

Commodity Prices 2005–2014 (Source – Company Reports)

Commodity Prices 2005–2014 (Source – Company Reports)

As per the Company, potential risks to BHP’s health entail fluctuations in commodity prices and currency exchange rate; ongoing global economic volatility; reduction in Chinese demand; actions by governments or political events in the countries of interest; failure to discover or acquire new resources; maintenance of reserves or development of new operations; changes to portfolio of assets through acquisitions and divestments; increased costs and schedule delays; any cost pressures and reduced productivity; unexpected natural and operational catastrophes; and so forth.

However, the dropping iron ore price has not deterred BHP to still increase iron ore production through its expansion projects and efforts in further cost reduction programs. But a point to consider here is whether increasing volume can offset the price drop given other conditions. Nevertheless, the spin-off may bring a sigh of relief for strengthening BHP’s cash flow and return on investment. BHP has further written to investors about its efforts on extra listing of the new Company in London. The Company also indicated about its decision on not to start a buy-back given the existing terms of the balance sheet and ongoing softness in the iron ore prices, as of now. Nonetheless, productivity improvements and strategic CAPEX deployment coupled with strong balance sheet indicate a potential in BHP.

BHP Daily Chart (Source - Thomson Reuters)

BHP Daily Chart (Source - Thomson Reuters)

Given the current scenario, it is expected that BHP can withstand the depression caused by the less favorable price environment and other economic sentiments, based on its diversified business model. Comparing BHP with its peer Rio Tinto, the Company has more advantage as iron ore forms a smaller portion of BHP’s asset pie and the balance of commodities is evenly distributed giving BHP an opportunity to bank on other commodities as well for better growth and prospects. Also, rising dividends and likely capital returns appear to steer the share price. All in all, BHP appears to be constructively positioned with commodities including iron and petroleum, in the long run. We thus put a

BUY recommendation at the current price of $32.84.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...