Company Overview - Beadell Resources Limited is engaged in the construction, mining and processing activities at its Tucano gold mine located in northern Brazil, and exploration for and evaluation of mineral resources in Australia and Brazil. It is primarily a gold producer with focus on its Tucano gold mine, located in Brazil. The Company has a portfolio of key gold exploration tenements throughout Australia and Brazil, including the Tartaruga and Tropicana East Projects. It operates in two segments: Australian exploration and evaluation and Brazilian exploration and evaluation. The Tucano site is located in Amapa State in northern Brazil, covering approximately 2,500 square kilometers of exploration licenses and a mining concession. Its Tartaruga project is located 120 kilometers northeast of Tucano. The Tropicana East project is located adjacent to the AngloGold Ashanti/Independence Group. The Handpump prospect located in the remote West Musgrave province of Western Australia.

Analysis – Beadell Resources has released its report for December quarter. BDR’s quarter was solid. Gold production at 61 koz increased 10% quarter on quarter and cash costs fell 4%. The key disclosure was that thee 9g/t JORC reserve at Duckhead has been disregarded and a substantial amount of material previously defined as waste has shown to be ore (lower grade) following grade control drilling. We now expect this to continue for the remainder of the life of the duckhead with the net effect of recovering more ounces than the reserve model predicts at a lower cost per ounce. BDR has provided guidance for eFY14 of 190 – 210koz on the existing reserve. We anticipate the tucano reserve to be updated this quarter with the key component Duckhead likely to add 20-40koz. We expect this to be mined during FY14 and as a consequence have revised FY14 production to 225koz at an all sustaining cost of US$569/oz.

The high grade nature of the Duckhead satellite deposit is unsurprisingly causing a few ups and downs for BDR. Grade and ounces produced will vary wildly from week to week. Fleet productivity at Tucano is clearly an issue for BDR as can be inferred from the overuse of the spent ORE stockpile. Again the spent ore stockpile was the savior with almost 500kt of low grade ore put through the mill during the quarter. We believe this no doubt led to the purchase of CAT 777’s to augment the existing fleet. Furthermore without additional fleet we envisage the gold production would have dropped dramatically in the second half of this year as mill feed would have still been heavily reliant on the spent ore stockpile yet not offset by the high grade Duckhead ore.

Mined tonnes are expected to continue to lag behind processed tonnes as high grade duckhead ore is blended with spent stockpiles to maintain a suitable recovery strategy scenario. With the purchase of additional fleet capacity we expect the mined tonnes to increase and therefore the Duckhead ore should represent a lower proportion of the overall mill feed blend. The fleet is expected to reduce maintenance costs and improve fleet availability. Management expects the fleet will progressively move from Duckhead to the longer life Urucum deposits.

Some of the key risks associated with Beadell resources are operational risk where an increase in operational costs could reduce the profitability and free cash generation of the Tucano project, commodity price risk - This includes factors such as supply and demand fluctuations for both gold and iron ore, technological advancement, forward selling activities and macro-economic factors ( a reduction in the gold price could impinge on the working capital position of the company), Capital Expenditure Risk – Beadell may exceed expected budgets and/or exhaust available funding before the completion of the stated projects and their respective timelines, Country risk – Brazil is a emerging economy and is subject to the risks of government taxes and political instability. Despite this risk, billions of dollars continue to be invested into Brazil’s iron ore and gold sectors, Reliance on third party risk – Quality of workmanship and services undertaken by contractors or third parties to Beadell resources is a relative risk. Work performed in a nature that is not conceived at a quality standard or in line with industry practice can affect the operations and performance of Beadell resources and its share price.

Source – Thomson Reuters

Source – Thomson Reuters

|

Price |

Price % Change |

|

Close: |

0.77 (06-Feb-2014) |

3M: |

(13.56%) |

|

52 Wk High: |

1.02 (28-Oct-2013) |

6M: |

17.69% |

|

52 Wk Low: |

0.49 (28-Jun-2013) |

1Y: |

(15.93%) |

Iron ore concentrate stockpiles continued o build in the quarter. This partly resulted in higher than expected cash cost as iron ore sales were less than expected. Moreover the strategy to accommodate high grade Duckhead ore resulted in the processing of low magnetite content stockpiled ore. We expect the volume of iron ore concentrate production and sales to increase as the non – Duckhead portion of the mill feed blend increases throughout the year.

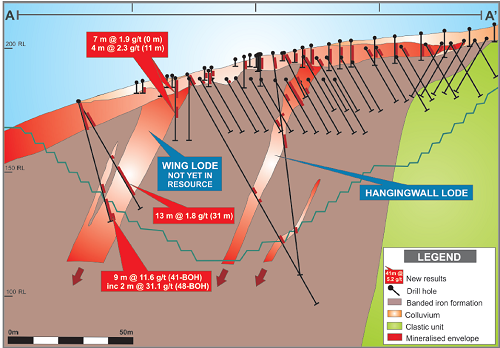

Duckhead drill section showing location of significant new wing Lode results (Source – Company Reports)

Duckhead drill section showing location of significant new wing Lode results (Source – Company Reports)

The ongoing exploration program remains focused on duckhead with 20,763m of RC drilling completed during the period. Of this 15,077m was on grade control drilling. A second RC rig was brought to site by the end of December quarter, which will allow on rig tor be dedicated too Duckhead, where a 30,000m drill program has commenced. Further rigs are expected to be brought to site in the first half of the year. Remodeling and re-optimization of the pit is underway, following a 30% positive reconciliation to the reserve model in the December quarter. In addition an interim resource model of the Wing Lode is also being completed and will be included in the re optimized Duckhead pit. In Australia one comment that attracted our attention was that nickel sulphides had been identified at the Tropicana East Project during a petrological and multi-element geochemical analysis of RC drill chips. Company geologists have logged ultramafic rocks (traditional hosts of nickel sulphide deposits in Western Australia) with disseminated nickel and copper sulphides subsequently identified via petrological analysis. Given the recent successes of Sirius Resources we will keep an eye on this.

Project Debt was reduced to UD$62 Million during the quarter from US$94 Million at the end of September, with net debt reducing to A$45 Million from A$66 Million. Cash and bullion at the end of December dropped A$10 Million to A$25 Million from A$35 Million at the end of September, with solid operational cash flows offset by the US$32 Million in principal debt repayments and capex of A$16.6 Million during the quarter. We will be putting a BUY on BDR at the current closing price of $0.765.

Disclaimer

Kalkine provides general advice on securities. Kalkine does not provide advice that takes into account your, or anybody else’s investment objectives, financial situation or needs. We strongly suggest that you should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. Employees and/or associates of Kalkine Pty Ltd may hold one or more of the stocks reviewed on this website. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...