Company Overview - BC Iron Limited (BC Iron) is engaged in mining, crushing and export of direct shipping iron ore and mineral exploration, focusing primarily on iron ore deposits near Nullagine, Western Australia. The Company’s core focus is the Nullagine Iron Ore Project (NJV), a 75:25 joint venture with Fortescue Metals Group Limited (Fortescue) located approximately 55 kilometers north of Fortescue’s Christmas Creek operation. The NJV mine plan comprises four mining areas: Outcamp, Warrigal, Bonnie East and Coongan. BC Iron is the operator and manager of the project, which includes mining activities at Nullagine and haulage of iron ore by road from the mine to Fortescue’s Ore Processing Facility at Christmas Creek. BC Iron contracts Fortescue’s subsidiary, The Pilbara Infrastructure Company, to provide rail services from Christmas Creek and port services through Port Hedland. Fortescue also provides marketing services to the NJV, lending support in shipping, logistics, scheduling and marketing.

Analysis – BC Iron (BCI) produced a soggy March Quarter 2014 result. However there were no major surprises either negative or positive. We expected costs to be higher in March quarter due to seasonal effects yet the higher waste movement was a little unexpected. Ore Mined of 0.95Mt was low due to a wetter than normal wet season. Ore shipped of 1.22Mt was above our estimate, a great outcome considering the weather and low mining volumes. The shipped ore was 28% higher than ore mined which underlines BCI’s planning ability at the operational level and flexibility in mining and stock piling. C1 cash costs were higher than anticipated at $54/t due to above average stripping ratio. The resultant cash balance of $149m was substantially below our estimate due to timing of cash receipts from two ships leaving in late march and BCI paying 75% of costs (as per JV) for the quarter but only receiving 62% of sales revenue. Changes to free cash flow have been significant from quarter to quarter. The December Quarter Free Cash Flow was $84m whereas the March Quarter Free cash flow fell to an estimated $14m.

Nullagine Project (Source - Company Reports)

Nullagine Project (Source - Company Reports)

NJV FY14 sales guidance remains unchanged at 5.8Mt to 6.2Mt with cost guidance for FY14 also unchanged at A$46 - $50/t. The increase in C1 costs during the March Quarter to $54/t was a result of increase in marketing costs and fixed costs spread over less tonnes. The higher strip ratios reflected the miners moving to areas of higher waste while the load and haul fleet was unable to operate during the periods of wet weather. The increased waste movements and lower volumes resulted in cash costs averaging A$54/t in the March quarter. BCI has indicated it still expects costs toe average A$46-50/t for FY14 but at the top end of the range.

Iron Ore Price (Source - Company Reports)

Iron Ore Price (Source - Company Reports)

BC Iron became cash flow positive in the December 2011 quarter. Nullagine is now de-risked and at steady production rates. Cash cost are stable and margins are impressive. We see BC Iron as a inexpensive way to gain exposure to iron ore. Cash generation is set to remain elevated now that the operation has hit the 6Mtpa rate.

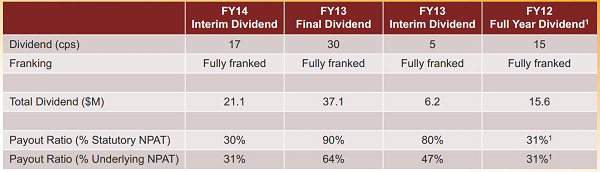

Dividends (Source - Company Reports)

Dividends (Source - Company Reports)

There will be questions asked about the use of cash given limited organic growth, however we believe BC Iron has given clear indications that it is comfortable returning cash to shareholders through dividends and after acquiring a further 25% of the Nullagine JV off FMG in December 2012, the acquisition strategy will likely be small scale, not transformational. In the current turbulent market environment , BC Iron’s strong balance sheet, steady production and healthy dividend yield (12.80% as of share price on 28/05/2014) should see the stock well supported.

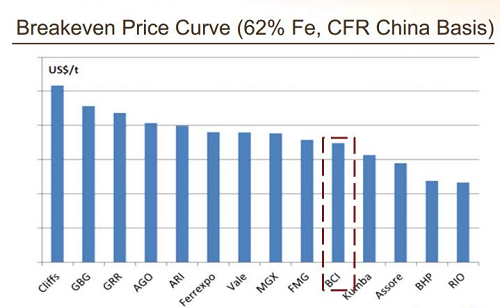

Breakeven Price Curve (Source - Company Reports)

Breakeven Price Curve (Source - Company Reports)

January 2014 had the fourth highest rainfall in more than 100 years. Accordingly BCI experienced significant wet weather impacts for the quarter. However rainfall in February and March was below average which allowed BCI to regain some lost production from inactivity in January. BCI’s share of tonnes shipped for the quarter was 0.76Mt (total ore shipped 1.22Mt) which represents 62% of total NJV tonnes shipped. This effectively reverses the previous quarter statistics. Where BCI’s share of tonnes shipped was 85%. FY14 to date BCI has shipped 3.22Mwmt or 74% of total NJV tonnes.

Ore Mined, Processed & Shipped (Source - Company Reports)

Ore Mined, Processed & Shipped (Source - Company Reports)

Realized pricing for the quarter was US$106/dmt, down from US$121/dmt achieved in the December Quarter. However this was adjusted down to US$102/dmt due to negative quotational pricing adjustments resulting from sales in December Quarter. BC Iron incurred a negative quotational pricing outcome in March Quarter. We note that this adjustment is occurring largely due to customers asking for different pricing periods. For example customers may be moving towards month +1 pricing as opposed to month pricing in an environment where it is expected that the price will fall. In other words a cargo purchased in March will be priced on the average price in April as opposed to March. In periods where the iron ore price is rising we expect customers to go back to pricing of the month or perhaps even push BCI to Month -1. The current events go to show the power the customers are able to exert on the smaller players. Also impacting the received price was discounts for impurities and the proportion of sales under the Henghou offtake agreement which attracts a pre-agreed discount as well as a small amount of uncommitted shipments in the March quarter which reflected softness in the iron ore market.

Crushing, Haulage & Port Services (Source - Company Reports)

Crushing, Haulage & Port Services (Source - Company Reports)

Iron Ore price is currently trading below U.S $100. Other factors are clearly also weighing on sentiment including ongoing credit tightness, elevated port inventories, steel mill iron ore destocking, falling steel prices and reduced rates of steel production. With such an aggressive drop in price we would expect buyers to stay on the sidelines waiting for further price falls. For those who had been waiting to buy into iron ore names we believe this current price weakness creates such an opportunity. BCI is expected to deliver a strong finish to the year hence the June quarter production result should provide a positive catalyst for the stock. The results of the low grade processing study are due for release in July and assuming are positive should enable BCI to upgrade its reserves and extending the mine life of NJV. We like BCI story and are putting a BUY on the stock at the current price of $3.69.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Please wait processing your request...

Please wait processing your request...