Company Overview - BC Iron Limited (BC Iron) is engaged in mining, crushing and export of direct shipping iron ore and mineral exploration, focusing primarily on iron ore deposits near Nullagine, Western Australia. The Company’s core focus is the Nullagine Iron Ore Project (NJV), a 75:25 joint venture with Fortescue Metals Group Limited (Fortescue) located approximately 55 kilometers north of Fortescue’s Christmas Creek operation. The NJV mine plan comprises four mining areas: Outcamp, Warrigal, Bonnie East and Coongan. BC Iron is the operator and manager of the project, which includes mining activities at Nullagine and haulage of iron ore by road from the mine to Fortescue’s Ore Processing Facility at Christmas Creek. BC Iron contracts Fortescue’s subsidiary, The Pilbara Infrastructure Company, to provide rail services from Christmas Creek and port services through Port Hedland. Fortescue also provides marketing services to the NJV, lending support in shipping, logistics, scheduling and marketing.

Analysis – BCI has announced an off market takeover offer for Iron Ore Holdings Ltd with IOH shareholders to receive 0.44 new BCI shares for each IOH share held and cash of $0.10/share. The offer values IOH at $1.59/share, a 67% premium based on IOH’s pre offer close of $0.95/share. We view the deal as positive for BCI. The offer is expected to close by late September 2014. BCI also has guided for a final dividend of 15 cents per share bringing total FY14 dividend to 32 cents per share. BCI has stated that there will be no change to its payout ratio guidance of 30-50% following this transaction.

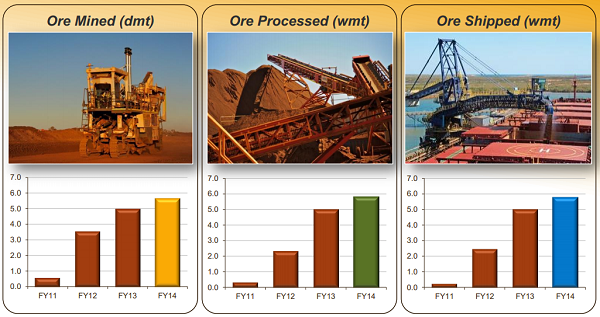

NJV Operational Performance (Source - Company Reports)

NJV Operational Performance (Source - Company Reports)

BCI’s value is currently most leveraged to near term iron ore prices given its relatively short mine life (5 years on reserves). The acquisition of IOH will shift this value leverage to the longer term. The Buckland project (DFS completed) adds further long term value leverage. Acquiring IOH will give BCI a second source of revenue with the mine gate sales agreement with Iron Ore Holdings set to commence in the current quarter. IOH has just completed a feasibility study on the Buckland project which has the potential to produce 8mtpa for an all-in capex of $877m.

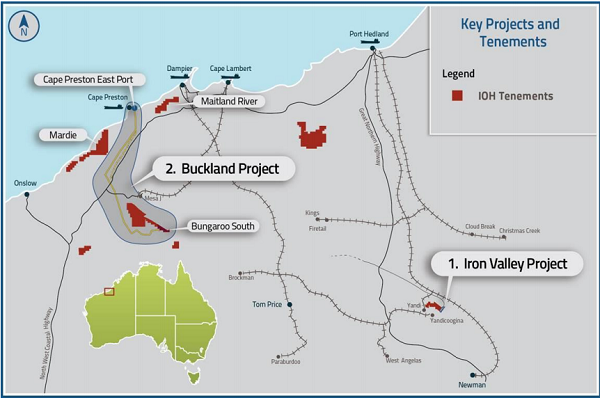

IOH Projects (Source - Company Reports)

IOH Projects (Source - Company Reports)

BCI has announced that subject to board approval it will pay a $0.15/share final dividend lifting the FY14 payout to $0.32/share. We had expected only a $0.06 final dividend and the increased payment provides some comfort that dividend will continue. We note that the dividend is likely to come under pressure in FY16 and FY17 as peak debt during the Buckland construction occurs but beyond that an 8-10% yield looks sustainable in the medium to long term.

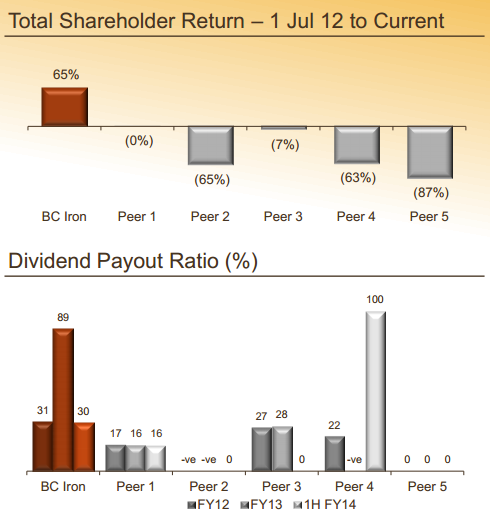

Total Shareholder Return (Source - company Reports)

Total Shareholder Return (Source - company Reports)

IOH has provided an indicative earnings range for the Iron Valley agreement. Using assumptions of US$90-110/t FOB iron ore (62% Fe equivalent), currency of US$0.90/A$ and production of 4-6Mtpa, the company expects annual EBITDA to IOH of $20-75m. This EBITDA estimate is after third party and state government payments. Given the disclosed information, IOH’s indicative potential earnings from the agreement and using assumptions consistent with other Pilbara iron ore producers we estimate the agreement could earn IOH annual EBITDA of around $25m and could be worth around $150m.

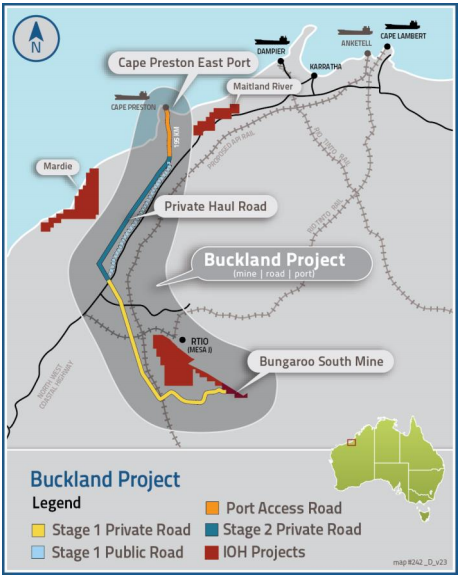

Buckland Project (Source - Company Reports)

Buckland Project (Source - Company Reports)

IOH has completed a feasibility study for its 100% owned Buckland Project, examining a 8Mtpa mine-truck-barge-ship iron ore development at the company’s Bungaroo South Tenements. The DFS suggests total capex of $877m and life of mine cash operating cost of $48/t. IOH’s CAPEX estimate includes the development of a sealed haul road and a new 20Mtpqaa transshipping port at Cape Preston East. A final investment decision on the Buckland project is expected to be made in Q4CY14. IOH’s Buckland resource has one of the lowest levels of silica and alumina compared to other iron ore resources of ASX listed iron ore producers and developers. However the resource is also high in phosphorus levels and iron ore products sold will likely incur a quality discount of 6-7% to the benchmark price.

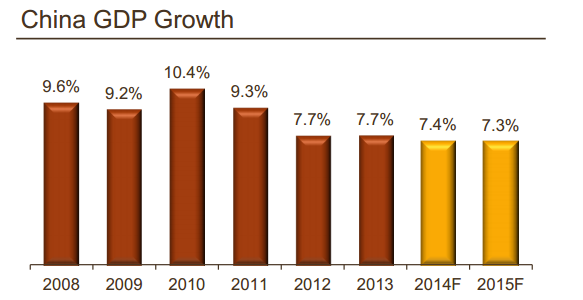

Chinese GDP Growth (Source - Company Reports)

Chinese GDP Growth (Source - Company Reports)

The key advantage of the transaction is the resource expansion and growth optionality provided by Iron Valley and Buckland. Iron Valley is likely to be a modest earnings contributor given that it is essentially a mine gate sale to Mineral Resources Limited (MIN), however it has a +20 year mine life at its targeted 5Mtpa rate of production (ramp up expected through FY15). Furthermore at the request of MIN, IOH has recently extended the mining approval to 10Mtpa from the current 6 Mtpa, potentially adding further upside if MIN looks to utilize this. The production split at Iron Valley is approximately 70% fines, 30% lump, helping offset some of the discounting pressure on the medium grade iron ores.

BCI Daily Chart (Source - Thomson Reuters)

The Buckland project adds growth optionality albeit at this stage there remain questions around funding and development strategy. The recently completed DFS contemplated an 8Mtpa operation for 15 years at C1 costs of $48/t and all in costs of $57/t. Overall the combined resource stands at 6X the size of BCI alone. With this transaction BCI’s growth focus shifts away from Brazil back to Australia. This may be seen as a positive by those concerned about BCI’s move to Brazil.

Through using primarily scrip for the transaction, BCI’s balance sheet remains in good shape. Proforma debt remains unchanged at $54m, and the cash position lifts to $194m (from June 30 balance of $159m). There are small level of corporate and overhead synergies that could be extracted. IOH also has unutilized tax losses of approximately $14m which BCI would be able to utilize (providing tax shelter of approximately $45m). The West Pilbara region has seen a step change in interest levels with Baosteel taking over Aquila, and with it the West Pilbara Iron Ore project. We believe that project requires greater scale to make the economics work given its large capex. The Bungaroo South Mine (the Buckland project mine) could easily fold into Anketell. Mineral resources has also demonstrated its interest in the region with its counter offer for AQA that ultimately failed. IOH management have indicated that they are already having discussions with Baosteel.

The acquisition of IOH is earnings dilutive for BCI and will place some pressure on the dividend particularly in FY16 and FY17. However Buckland does provide longevity for BCI, extending its production and earnings outlook by over 10 years. We believe there are a number of lower capital options for Buckland that BCI could pursue, including using Baosteel’s planned Anketell Point infrastructure that could see significantly lower capex and reduce pressure on dividends during construction. We reiterate our BUY recommendation on the stock at the current price of $3.15.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...