Kalkine has a fully transformed New Avatar.

Company Overview: Base Resources Limited is an Australia-based mineral sands producer. The Company is engaged in the operation of the 100%-owned Kwale Mineral Sands Operation (Kwale Operation) in Kenya. The Company's segments include Kwale Operation and Other operations. The Kwale Operation is located approximately 10 kilometers inland from the Kenyan coast and over 50 kilometers south of Mombasa, the principal port facility for East Africa. The Kwale Operation generates revenue from the sale of rutile, ilmenite and zircon. The project has annual production of approximately 80,000 tons of rutile, over 360,000 tons of ilmenite and approximately 30,000 tons of zircon. The Company's subsidiaries include Base Titanium (Mauritius) Limited, Base Titanium Limited and Base Exploration Tanzania Limited.

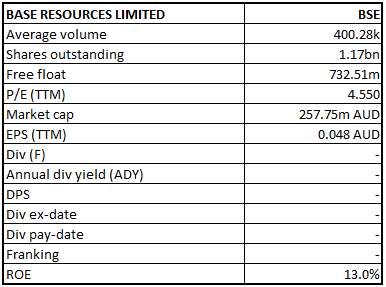

BSE Details

Decent Top-line Performance with CAGR above 50% over FY14-19: Australia based, African focused Base Resources Limited (ASX: BSE) is involved in the operation of the Kwale Mineral Sands Operation in Kenya and the development of the Toliara Project in Madagascar, which the Group is progressing through an accelerated feasibility study program, that aims to advance towards a decision to proceed to construction in 2020. Looking at the past performance over FY14 to FY19, total revenue of the company has grown with a CAGR (compounded annual growth rate) of 50.99%. Group’s total revenue improved from US$26.7 Mn in FY14 to US$209.5 Mn in FY19, and net income improved from a loss of US$12.9 Mn in FY14 to a profit of US$39.2 Mn in FY19.

FY19 has been a rewarding year for the company, where its Kwale Operation in Kenya delivered decent performance along with the development at its world-class Toliara project in Madagascar. Strong price improvement for rutile and zircon boosted the company’s turnover and established a platform to further grow its business. Its major focus point for FY20 involves optimization, consistent performance of the Kwale Operations on the South Dune, mine life extension at Kwale and progress and funding of Toliara Project.

The Toliara project is gaining significant momentum on the ground with 5,500 local men and women registering to qualify for participation in a wide range of training programs, including heavy mobile equipment operation, brickmaking, bricklaying and plastering. Medium and long-term dynamics for the company’s products continue to be encouraging, underpinned by decent global demand and restricted supply. Moreover, total recordable injury frequency rate at Kwale operation for the financial year 2019 was reported ‘nil’, with no medical treatments, which is a remarkable achievement for any mining operation in any jurisdiction.

Historical Ilmenite/Rutile prices (Source: Company Reports)

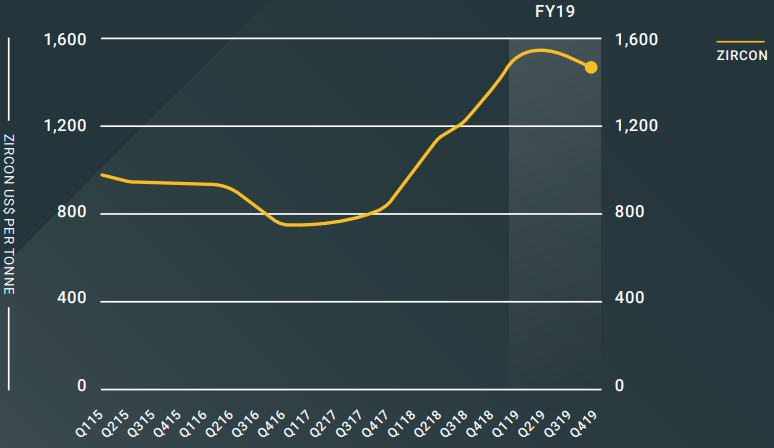

Historical Zircon prices (Source: Company Reports)

Key Highlights of September’19 Quarter: At the end of June, following the transition from the fully depleted Central Dune orebody, Kwale Mineral Sands Operations in Kenya has successfully ramped up mining operations at the South Dune orebody. The mining ramp-up exceeded expectations with an annualized mining rate of close to 20 Mtpa, higher than the 18Mtpa plan. Moreover, the bulk loading operations at the company’s Likoni Port facility operated smoothly while dispatching more than 72kt of ilmenite, rutile and low-grade zircon during the period.

Due to higher power costs associated with the additional mining volume and pumping distance, and an increase in the non-cash rehabilitation expense associated with clearing of land ahead of mining activities, total operating costs were higher than the previous quarter. Lower production volumes, along with higher total operating costs led to a higher unit operating cost of US$173 per tonne produced as compared to US$127 per tonne in the last quarter. Costs of goods sold comprising operating costs, adjusted for stockpile movements, and royalties, was reported at US$213 per tonne sold, higher than COGS in the previous quarter, which was reported at US$180 per tonne. This was due to the higher operating cost per tonne produced and sales mix. The average revenue per tonne marginally reduced to US$469 per tonne as compared to US$482 per tonne in the previous quarter due to a higher proportion of ilmenite sold in the quarter. With this, the September quarter revenue to cost of goods sold ratio reduced to 2.2 as compared to 2.7 in the previous quarter.

Net cash as on September 30, 2019, was reported at US$30.6 Mn, which comprised cash and cash equivalents of US$45.6 Mn and revolving credit facility debt of US$15.0 Mn. The company has issued 1,166,623,040 fully paid ordinary shares along with 48,586,062 performance rights, issued according to the terms of the Base Resources Long Term Incentive Plan.

Quarterly Key Financial Metrics (Source: Company Reports)

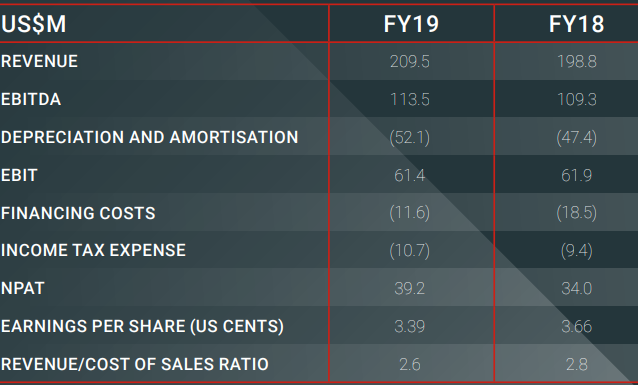

FY19 Key Highlights for the period ended June 30, 2019: Revenue for the period increased by 5% to US$209.5 Mn, mainly due to the improvement in average price movement for both rutile and zircon. Rutile price for the period improved by 22% and zircon price improved by 28%. Earnings before interest, tax, depreciation and appreciation (EBITDA) for the period increased by 4% to US$113.5Mn, and net profit after tax (NPAT) increased by 15% to US$39.2Mn. The company closed the period with no debt and cash balance of US$19.2Mn.

FY19 Key Financial Metrics (Source: Company Reports)

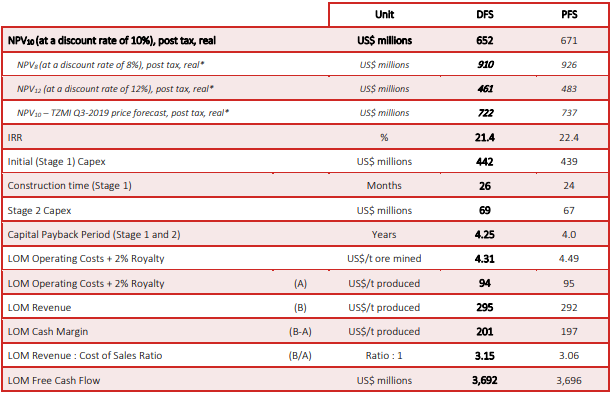

Definitive Feasibility Study for Toliara Project Aligns with Pre-Feasibility Study Outcomes: On December 12, 2019, the company published its definitive feasibility study (DFS) on its Toliara Project in Madagascar, where DFS closely aligns with the Pre-Feasibility study (PFS) outcomes, which was released in March 2019. It confirms a post-tax/pre-debit (real) NPV10 of US$652 Mn and an average revenue to cost ratio of 3.15 over the initial 33-year mine life. Capital expenditure for the Stage 1 to establish a 13 Mtpa mining processing operation was reported at US$442 Mn, and for Stage 2, which comprised increase of operation to 19 Mtpa, was reported at US$69 Mn. In the first 26 years of full production, despite the expectation of global supply deficit of titanium dioxide feedstocks and zircon, the Toliara Project is expected to produce an average of 814kt of ilmenite, 55kt of zircon and 7kt of rutile annually. This production profile, along with a competitive revenue to cost of sales ratio is expected to generate estimated average annual free cash flows of US$140.2 Mn over these years. The company aims to upgrade the Ranobe Mineral Resources and Ore Reserves estimates along with concluding the funding arrangements towards a final investment decision planned for September 2020. The project is expected to create transformational opportunities for the communities, economic prosperity for the Toliara region and a flagship foreign investment for the government, which is expected to generate in excess of US$1 Bn in government revenue and community development expenditure over the 33-year mine life.

Under annual averages, excluding the first and last partial operating years, production of 780 kt ilmenite (sulphate, slag and chloride), 53kt zircon and 7kt rutile have been estimated. Revenue has been estimated at US$248.2 Mn, with maximum distribution from ilmenite (65%) then zircon (32%) and rutile (2%). Operating costs for the period have been estimated at US$76.9 Mn, inclusive of 2% Government royalty. Non-operating costs involving costs associated with community, external affairs, marketing, etc., have been estimated at US$7.1 Mn. EBITDA and NPAT have been estimated at US$164.3 Mn and US$110.2 Mn, respectively. Free cash flow has been estimated at US$132.4 Mn.

Outcomes for Toliara Project Definitive Feasibility Study (Source: Company Reports)

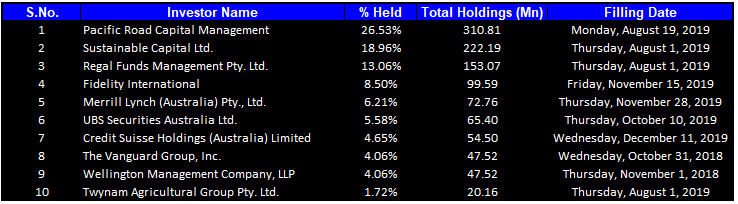

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 93.33% of the total shareholding. Pacific Road Capital Management and Sustainable Capital Ltd. hold maximum interests in the company at 26.53% and 18.96%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

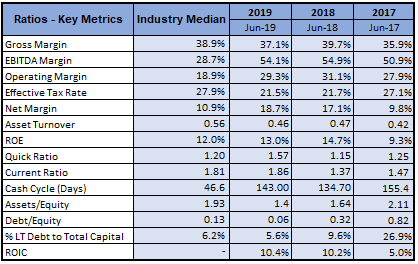

A Quick Look at Key Metrics: Its EBITDA margin and net margin FY19 stood at 54.1% and 18.7%, better than the industry median of 28.7% and 10.9%, respectively, implying decent fundamentals of the company. Its current ratio for FY19 stood at 1.86x, better than the industry median of 1.81x, implying the company’s decent liquidity position. Its debt to equity multiple for FY19 stood at 0.06x, lower than the industry median of 0.13x.

Key Metrics (Source: Thomson Reuters)

Key Risks: The company is susceptible to certain risks such as actions by governments, political events or tax authorities; global economic uncertainty and liquidity; natural catastrophes; climate change; etc.

What to Expect: Kwale operations production guidance for FY20 has been kept unchanged from the previous update. Production for Rutile, Ilmenite and Zircon have been estimated in the ranges of 64,000 to 70,000 tonnes, 315,000 to 350,000 tonnes and 25,000 to 28,000 tonnes, respectively. The above guidance includes assumptions such as MSP feed rate at an average of 75tph; Mining of 18.0Mt at an average HM grade of 3.58%, with all FY20 volume coming from Ore Reserves; and MSP product recoveries of 100% for ilmenite, 99% for rutile and 77% for zircon.

Industry Outlook: Titanium minerals are facing tight market conditions because of ongoing constraints on the global supply of sulphate ilmenite and high-grade chloride feedstocks (including rutile), which has resulted into positive price momentum. The global market is witnessing a decent demand for ilmenite due to an increase in Chinese pigment production. Despite global uncertainties due to macro-economic concerns, leading to cautious buying behavior along with maintaining low inventory levels, demand from most major chloride pigment producers remains positive and is expected to operate at high production levels. The zircon market faced a renewed contract pressure due to global uncertainties, underpinned by major global zircon suppliers offering price rebates and discounts to their customers for the remainder of the CY2019, which has led to a slight decline in zircon price for the coming quarters.

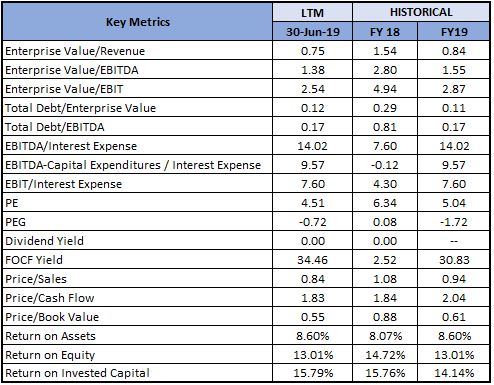

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: Price to Earnings (PE) Multiple Approach.png)

Price to Earnings (PE) Multiple Approach (Source: Thomson Reuters), *1 USD = 1.46 AUD

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock price fell by 10.20% in the past six months. Currently, the stock is trading towards its 52-week low of $0.195, proffering an opportunity for accumulation. Company’s top-line has shown a decent performance over the past five years, with CAGR above 50%, whereas the bottom-line has improved drastically from a loss in FY14 to a profit in FY19. Strong development at its world-class Toliara project in Madagascar is further expected to boost the company’s earnings in the coming times. The company has kept FY20 production guidance unchanged and with the cooling-off of macro-economic concerns, especially the USA-China trade war, global growth is expected to revive in the coming times, which, in turn, is likely to help the company to improve its margins. Looking at the business prospects over the long-term, we have valued the stock using a relative valuation method, i.e., Price to Earnings (PE) multiple, and arrived at a target price of double-digit growth (in % term). Hence, we give a “Buy” recommendation on the stock at the current market price of A$0.220 per share on December 18, 2019.

BSE Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...