Kalkine has a fully transformed New Avatar.

SECTOR OVERVIEW

A country’s banking sector and the economic cycle go hand in hand, and it is a fact that the performance of the banking industry is a mirror image of the economic cycle. By looking at the banking sector, one can have an idea about the performance of the country, in a way. Because of this reason, financial stocks generally dominate the benchmark equity index of any state. In Australia, Financial stocks have more than 28% of weightage in ASX 200; primarily led by the big four banks as they account for close to 19% of the index in terms of market capitalisation.

In this report, we shall be deep diving the banking sector to understand more about the drivers and current trends, which are impacting the performance of the companies operating in the industry.

.png)

Let’s take a detailed look at the key elements of the sector.

- Current interest rate environment: Cash Rate is the key policy rate which gives the direction to the general interest rates and is managed by the Reserve Bank of Australia (RBA). The apex bank cut the cash rate by 25 basis points to a record low of 0.75% in its monetary policy meeting held on 1 October 2019. The primary reason behind the rate cut was to provide support to employment, increase income and manage inflation target. October rate cut was the third cut in 2019. Inflation number has also shown an upward movement as December quarter data increased to 1.8% from 1.6% recorded in June quarter. Following the series of rate cuts, liquidity is expected to increase in the market which, in turn, will help the RBA to manage inflation which is at present below its target range of 2% to 3%. Also, the unemployment rate declined to 5.1% in December 2019 from 5.3% recorded in October 2019.

.png)

- Lower interest rate scenario to persist: Going forward, interest rates are expected to remain low in the economy, and there is a market-wide expectation that the RBA might cut the cash rate by another 25 basis points in the near term. And, if these rate cuts are not able to help RBA in achieving its goals, which are inflation management and liquidity creation to revive the growth, the apex bank might be forced to focus on the unconventional ways to create liquidity. In line with the hint provided by the Governor of the RBA earlier, the regulator might also start pumping money directly into the economy by conducting open market operations or introducing quantitative easing, which will be the first in its history.

However, lower interest rates are expected to act as a shot in the arm for the property prices. According to the Australian Bureau of Statistics’ (ABS) release, property prices grew 2.4% in the third quarter of 2019, marking it as the strongest quarter since 4Q2016 in terms of price rise. The prices are expected to remain northward following the RBA’s easing stance towards liquidity and the introduction of the government’s “First Home Loan Deposit Scheme”.

.png)

- Series of rate cuts and the credit growth:TheRBA is trying hard to increase the liquidity in the system, but the number shows that desired results are yet to be achieved. Credit growth remained tepid since the first-rate cut announced in June 2019. If we look at the monthly numbers, total loans grew 0.2% (each month) in July, August and September. In October, the RBA introduced another rate cut, but the credit growth further slowed down to 0.1% (each month) in October and November.

In 12 months ending November 2019, total loans grew 2.3% y/y compared to 4.4% growth recorded in November 2018. The slowness persisted across all segments; housing loans increased 2.9% y/y against 4.9% while business loans growth fell to 2.5% vs 4.4%. However, personal loans contracted most, marking a decline of 4.9% compared to a 1.7% decline recorded in November 2018.

.png)

2020 is now expected to be a better year in terms of credit growth based on the following facts:

- Current lower interest rate environment would act as a booster to the consumers who are planning to buy homes. The trend is visible in the latest data released by the ABS. November data shows that new loan commitment for housing increased by 1.8% m/m.

- The government’s new initiative “First Home Loan Deposit Scheme” is expected to provide a further boost to the credit expansion in the economy.

- The aftermath of bushfire will require some rebuilding activities which may fuel demand for construction and business loans.

- Regulatory developments: In July 2019, the Australian Prudential Regulation Authority (APRA) asked the banks to increase their capital adequacy ratio by three percentage points. All of this can be managed through the tier 2 instruments. The deadline to meet these new requirements is 1 January 2024. In addition to this, the APRA asked ASX big three banks to put aside an additional $500 million to strengthen risk management. The government introduced “First Home Loan Deposit Scheme” from 1 January 2020 for first time home buyers.

In the related parlance, the Reserve Bank of New Zealand revised the regulatory capital requirements for the banks operating in New Zealand, in December 2019. Followings are the key details:

- New tier 1 ratio requirement is 16% for the systematically important bank, while other banks need to maintain a tier 1 ratio of 14%

- Total capital adequacy ratio requirement is 18% for the systematically important bank, while other banks need to maintain a capital adequacy ratio of 16%

- These new requirements will be effective from July 2020, with 7 years of transition period

- Transition from outlook of 2019: Almost all the banks struggled to expand their loan book following a slowdown in credit formation in the economy, as seen in 2019. Most of the banks reported a decline in their net profits primarily driven by a dip in non-interest income. This, in turn, resulted in a lower RoE for the banks. A hit on profitability forced some banks to cut down on their dividend distribution. However, given some form of stability coming into the sector, 2020 outlook is expected to be on a positive side.

- A general view on the sector: The prices of most of the banking stocks witnessed a downward trend in recent past on the back of company specific reasons and a general downturn in the industry. However, these stocks have a history of paying decent dividends. The average payout ratio of these stocks stood above 75% in 2019. Average dividend yield stood in the range of ~5% to ~8%; which is a decent return in an environment where interest rates are at historic low levels. In a nutshell, an investor can pick these stocks specifically for the dividend return based on the individual investment objective and risk appetite. Capital gain, if any will act as an icing on the cake.

BANKING SECTOR STOCKS' OVERVIEW AND DETAILS

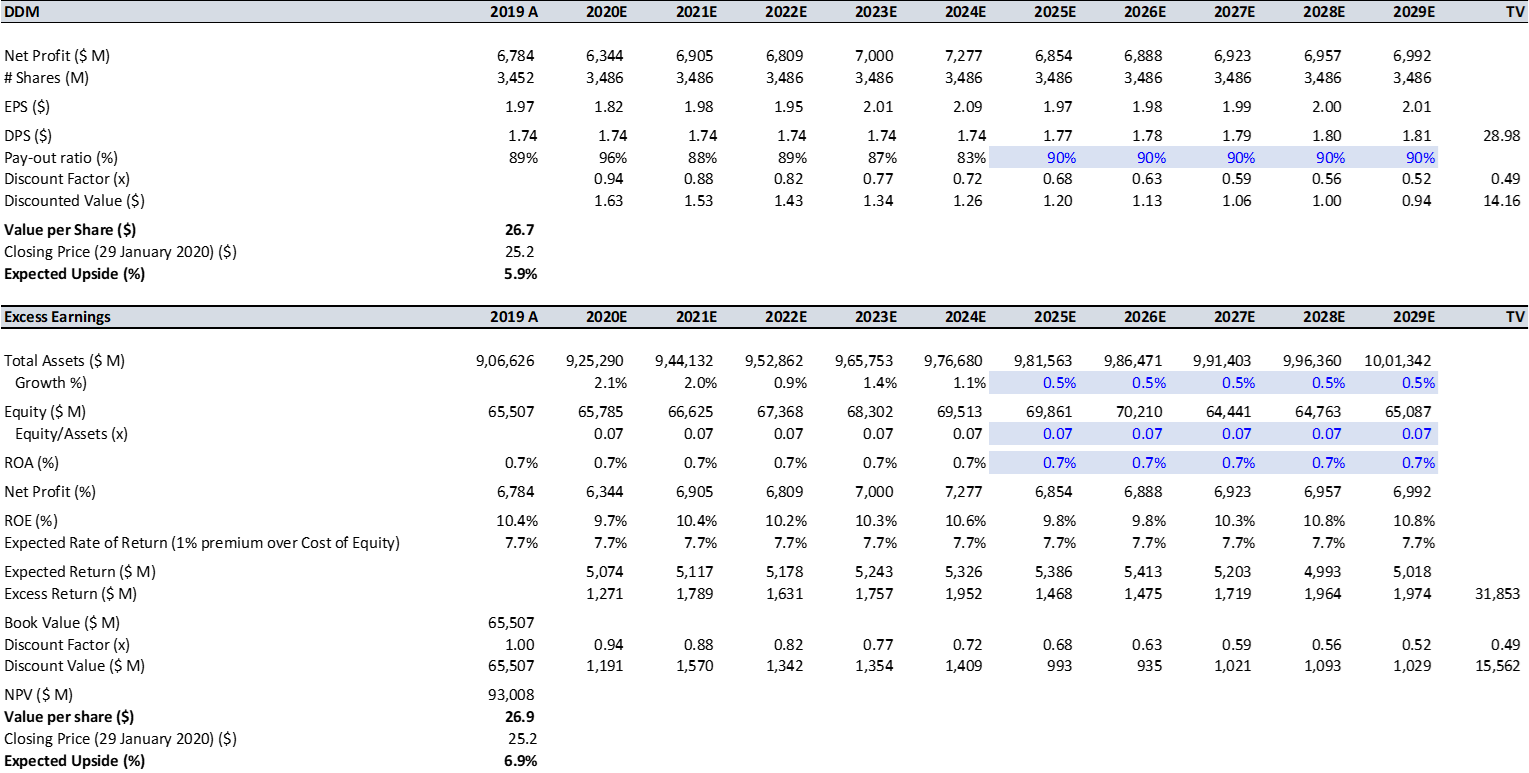

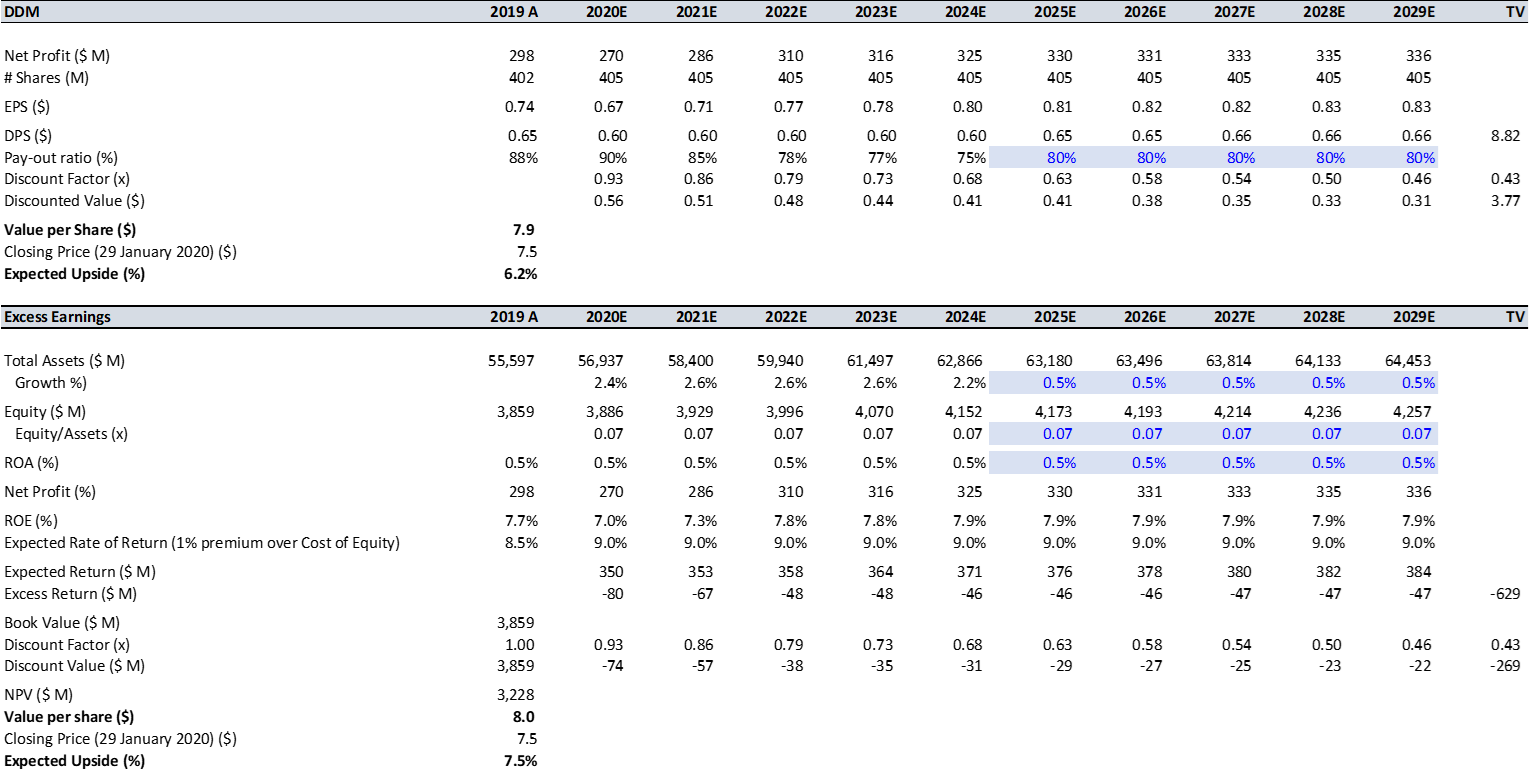

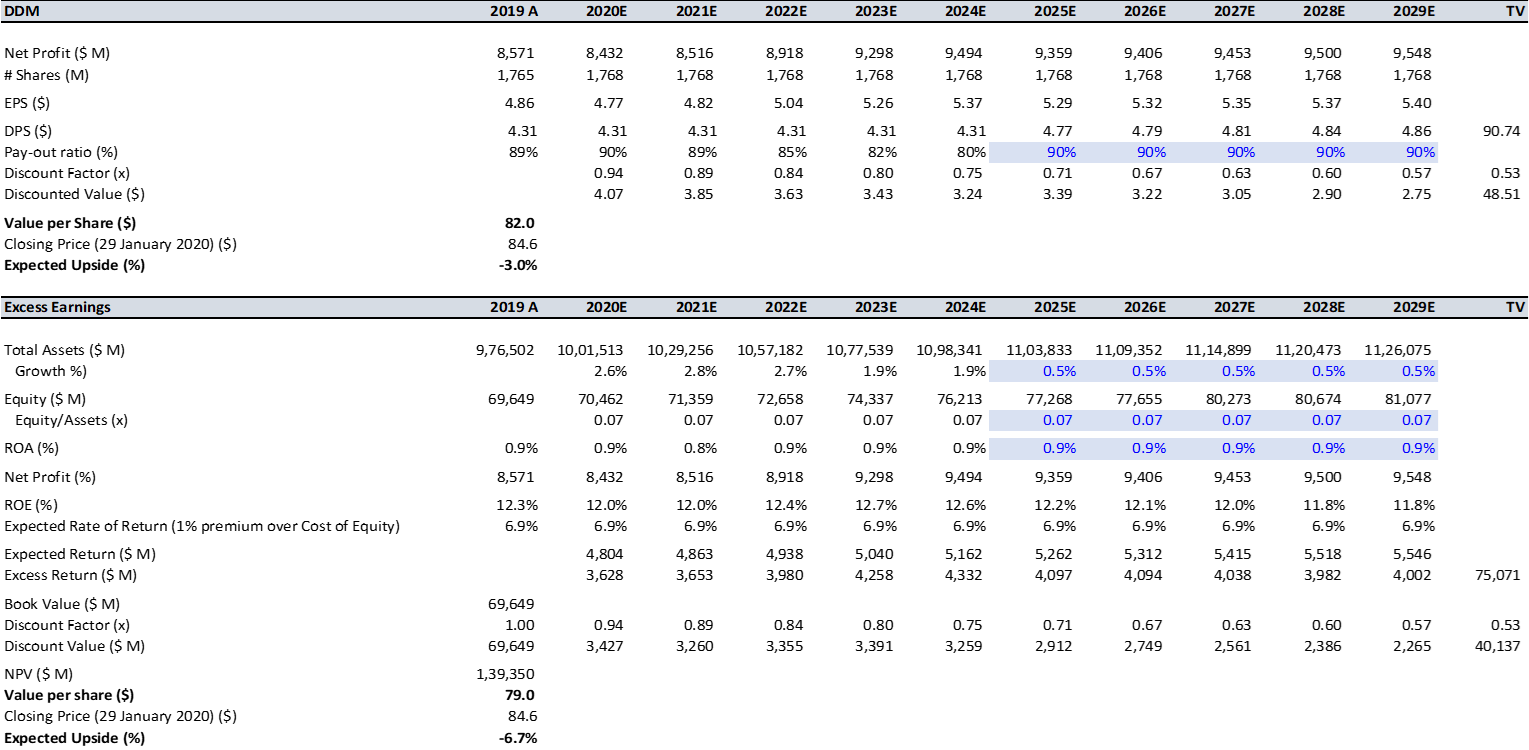

After understanding the key trends of the sector, let’s take a detailed look at five banks in terms of their outlook and performance. To gauge the potential of the banking stocks, we have used two metrics ‘Dividend Discount Model’ (DDM) and ‘Excess Earnings Methods’. DDM is established over a presumption that the current fair price of an underlying stock equals the sum of the company’s future dividend payments that is discounted to its present value. Excess Earnings Method discounts the company’s future earnings which it is expected to generate above a required rate of return or cost of equity.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

Valuation

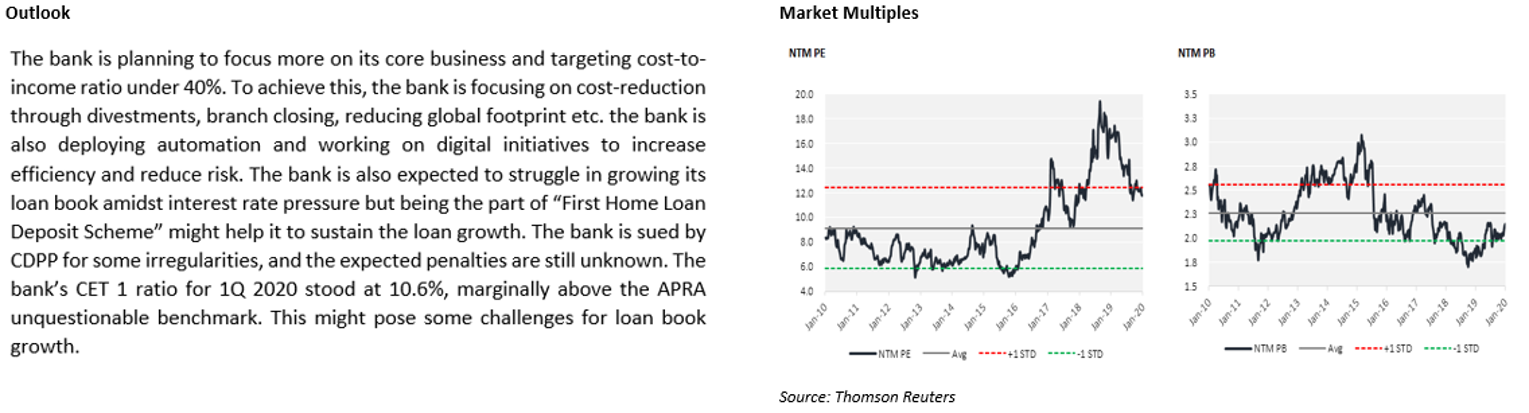

Our valuation models suggest that stock has potential downside in the range of ~3% to ~7% on 29 January 2020 closing price. As on 29 January, the bank’s dividend yield stood at ~5.1%.

Source: Kalkine Research

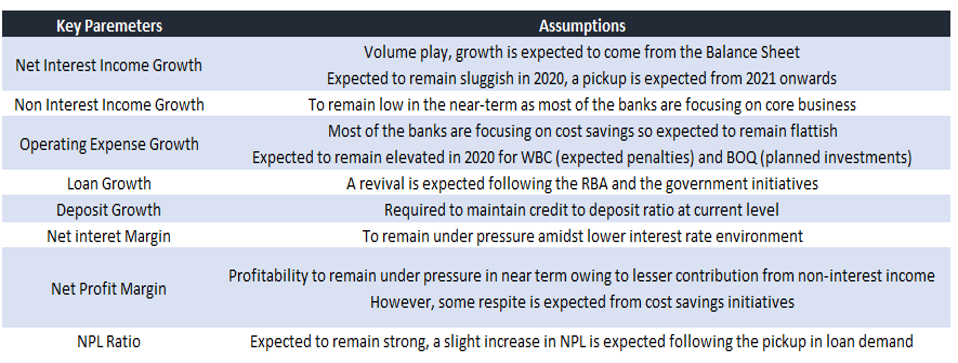

Key Assumptions Driving our Models

Note: All the recommendations and the calculations are based on the closing price of 29 January 2020. The financial information has been retrieved from the respective company’s website and Thomson Reuters.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...