Company Overview - Bank of Queensland Limited (BOQ) is an Australia-based entity engaged in retail banking, leasing finance and insurance products. The Bank operates in two segments: banking and insurance. Banking segment services include retail banking, commercial, personal, small business loans, equipment, debtor finance, treasury, savings and transaction accounts. Insurance segment services include consumer credit insurance, life insurance, accidental death insurance, funeral insurance and motor vehicle gap insurance. BOQ's operations comprise: Banking, BOQ Finance and BOQ Specialist. Retail banking includes savings and investment products, credit cards and personal and home loans. Business banking including business loans, transaction accounts, business charge cards and investment and statutory trust accounts. BOQ Finance incorporates the vendor finance businesses. BOQ Specialist delivers banking solutions to market segments, including medical, accounting and financial advisory professionals.

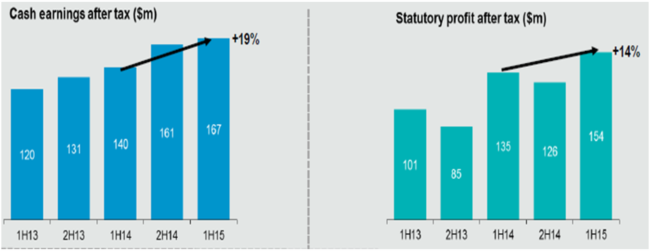

Analysis - Bank of Queensland Limited (ASX: BOQ) strategies and acquisitions have finally paid off as the group reported an increase of 19% of after tax cash earnings to $167 million for the first half of 2015, against $140 million in the corresponding period of last year. The increase was driven by the synergies from BOQ specialist acquired by the group during July 2014. BOQ specialist business contributed a net profit after tax of $19 million, which is in line with the company’s guidance and is well positioned to achieve a full year target of $38 million earnings guidance. The statutory profit after tax rose by 14% on a year over year basis to $154 million.

Cash earnings after tax and statutory profit after tax (Source: Company Reports)

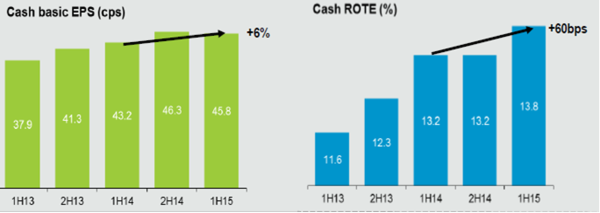

As a result, the underlying profit (before impairment expense and tax) surged 11% to $276 million, as compared to $249 million in the first half of 2014. Basic cash earnings per share improved to 45.8 cents against 43.2 cents in 1H14. Meanwhile, Bank of Queensland was able to improve its Return on total equity by 60 basis points to 13.8% during the period, as compared to 13.2% in the first half of 2014.

Cash basic earnings per share and ROTE (Source: Company Reports)

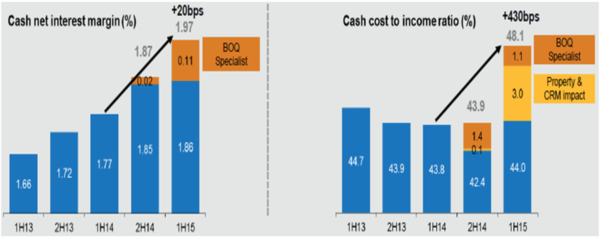

The group managed to deliver solid results during the period while maintaining competitive margins. Net interest margins improved by 20 basis points to 1.97% from 1.77% in the corresponding period of last year, driven by the high margin BOQ specialist. BOQ specialist has contributed 9 basis points. The Cost to income ratio rose to 48.1% from 43.8% due to one-off costs. Premises consolidation costs were $6 million while the pilot customer relationship management (CRM) system incurred $10 million during the period. The underlying expense increased by 3%, excluding these costs.

Cash net interest margin and cost to income ratio (Source: Company Reports)

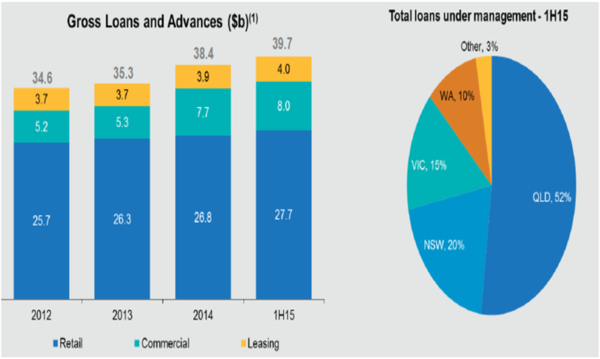

The total lending achieved an annualized growth of 7%, and is in line with the group’s expectation. BOQ’s initiatives of “customer in charge” strategy of broadening the channels has paid off, driving this growth. Bank of Queensland branch network witnessed an additional growth in BOQ business and the decreased the concentration on lower quality lending sectors like credit exposures. The gross loans and advances rose to $39.7 billion in the first half of 2015 from $38.4 million in 2014, driven by retail segment. Meanwhile, Queensland continue to dominate its portfolio, and represented 52% of the overall loans under management during the period, followed by NSW, VIC and WA, which accounts 20%, 15% and 10% respectively.

BOQ gross loans and advances and regional distribution (Source: Company Reports)

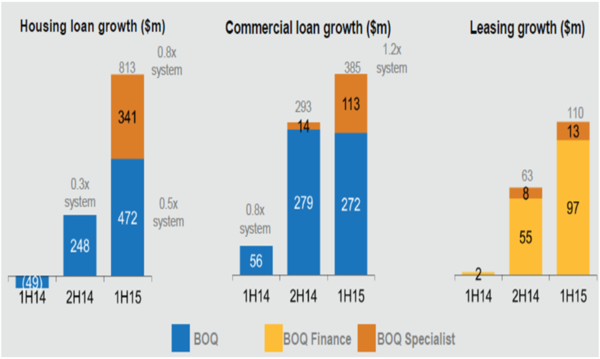

The housing loan surged to $813 million during the period, from $248 million in the second half of 2014, driven by BOQ specialist business and broker expansion. The diversification of the BOQ brand improved during the period as 57% of the applications were generated outside Queensland. On the other hand, the broker channel contributed 14% of the settlements during the period, driven by expanding Queensland market with 285 accredited brokers. Bank of Queensland has built a network of 1,932 brokers and intends a network of 2,500 brokers by the end of the fiscal year. As per the commercial loan highlights, this segment rose to $385 million during the period, driven by the BOQ specialist segment which increased to $113 million in the first half of 2015 from $14 million in the second half of 2014. The ongoing traction at New South Wales, Victoria and Western Australia contributed to this growth. The leasing segment also surged to $110 million during the period from $63 million in second half of 2014, driven by the BOQ finance business which rose to $97 million from $55 million in second half of 2014. Meanwhile, the BOQ finance portfolio witnessed an annualized growth of 6% to $4 billion in the first half, despite lower volumes and challenging plant and equipment investments. BOQ has launched several vendor and dealer business during the period, to enhance the group’s growth in the future.

Growth across all portfolios (Source: Company Reports)

Bank of Queensland has a stable funding coverage for 99% of lending balances. The house loans lending represent 69% of the assets, while the cash and highly liquid assets contribute 18% of lending. Meanwhile, Customer deposits accounts 67% of funding, followed by long term wholesale funding which represented 24%. The short term wholesale funding contributed 19% of the liabilities, which is mainly used to fund major liquid assets and trading securities.

Funding Mix (Source: Company Reports)

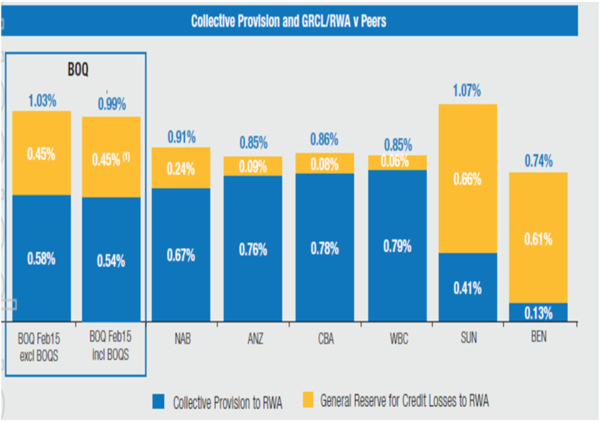

The credit quality of the bank’s portfolio continue to improve with loan impairment expenses decreasing to 18 basis points of lending against 26 basis points in 1H14. The impaired assets decreased by 13% on a year over year basis to $259 million in the first half. Meanwhile the collective provisioning levels (which includes GRCL) has slightly increased, and the group has maintained it at a premium as compared to the competitors. The impaired assets/GLA decreased by 20 basis points to 65 bps as compared to the corresponding period last year.

Impaired assets/ GLA performance against peers (Source: Company Reports)

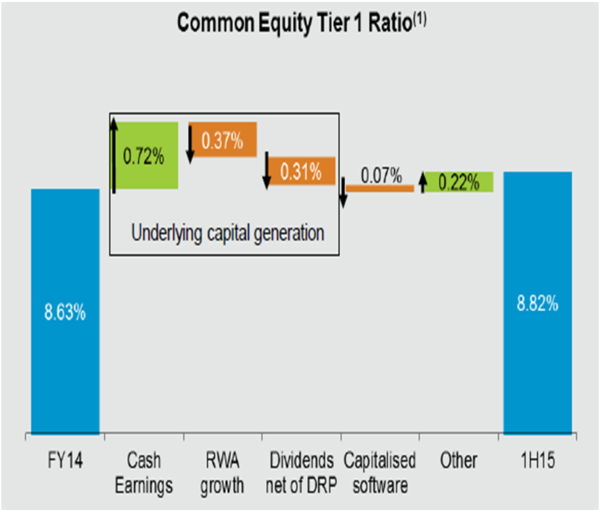

Meanwhile the common equity tier 1 ratio has improved to 8.82% in the first half of 2015, from 8.63% in 2014. The underlying cash earnings during the period was able to support loan growth of $1.3 billion and a 2 cent increase of interim dividends, resulting a 4 basis points of surplus capital. We believe that the present ROE has the ability to support further growth.

Common equity tier 1 ratio (Source: Company Reports)

In the month of May, BOQ priced $150 million of BOQ wholesale capital notes at a margin of 4.35% over the six month bank bill swap rate. The group intends to use these proceeds to qualify BOQ wholesale capital notes as additional tier 1 capital and for corporate purposes.

Outlook

The shares of Bank of Queensland has generated a year to date returns of over 9.9% and over 4.5% in the last four weeks alone. We believe that the group’s growth efforts through new channels like BOQ specialist, broker and virgin money mortgages will support its earnings in the coming periods. Moreover, we believe that BOQ is in line to achieve its guidance of 45% of cost to income ratio during the second half of the year. Bank of Queensland ongoing investments in digitized business will further enhance its productivity as well as benefits. Moreover, through BOQ specialist, the company is delivering expert marketing solutions to professional market sectors. Bank of Queensland efforts to offer on-balance sheet mortgages to BOQ specialist customers is generating better results than forecasted, which would further help BOQ to improve its earnings for the coming periods. Bank of Queensland is also a strong dividend player, with a dividend yield of 5.23%. BOQ increased the fully franked interim dividend by 13% to 36 cents per share during the first half of 2015, from 32 cents per share in the corresponding period of 2014.

.png) BOQ Daily Chart (Source - Thomson Reuters)

BOQ Daily Chart (Source - Thomson Reuters)

Based on the foregoing, we put a BUY recommendation on the stock at the current price of $13.39.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...