Kalkine has a fully transformed New Avatar.

Company Overview: Baby Bunting Group Limited (ASX: BBN) is one of the largest retailers of baby specialty goods in Australia, which is mainly supporting the parents with children from newborn to three years of age. The company’s main products range from prams, cots and nursery furniture, car safety, toys, babywear, etc. The core purpose of the company is to help the new and expectant parents in the early years of parenthood. The business model of BBN revolves around the sale of the third-party produced and branded baby goods via its store network and digital channel and is also engaged in selling private label and exclusive products..png)

BBN Details

.PNG)

Decent Growth in Revenue and Profit: Baby Bunting Group Limited (ASX: BBN) is Australia's largest specialty retailer of baby goods , which is primarily catering to parents with children from newborn to three years of age. The company’s principal products include, prams, cots and nursery furniture, car safety, toys, babywear, etc. As on 24 March 2020, the market capitalization of the company stood at $204.1 million. During FY19, the company witnessed an increase of 20.9% in revenue to $368 million and a growth of 27.3% in gross profit to $128.4 million. These results were mainly driven by increased focus of the company on growing its market share, securing prime sites for its store network and investing in people and systems to support growth. The growth in revenue and gross profit resulted in an increase of 43.3% in statutory net profit after tax to $12.4 million. Over the span of 4 years from FY15 to FY19, the company witnessed a CAGR (Compound Annual Growth Rate) of 19.54% in revenue and a CAGR of 20.01% in gross profit, reflecting gross margin expansion by an increase in scale, supply chain improvements, improved sourcing and the expansion of its private label and exclusive products offering. The company also benefitted from focused execution of its strategy, along with operational excellence. During the year, BBN opened several new stores and has developed a shopping centre format. The company also declared a fully franked final dividend of 5.1 cents per share, bringing the total dividend to 8.4 cents per share. This is equivalent to roughly 70% of BBN’s FY19 pro forma NPAT.

The company has recently released its interim results for the period ending 31 December 2019 wherein it reported strong growth in market share and profitability. The company is modernizing its brands and has introduced a contemporary brand, reflecting the brand essence of supporting new and existing parents in the early years of parenthood.

Baby Bunting Group Limited is targeting to expand its network of stores to over 80 stores throughout Australia and aims to open four to eight new stores a year, with the present number at 56. It is also focused on delivering a leading service offering supported by well-trained team members with an excellent product knowledge and is continuously expanding its services to grow sales from its existing stores.

.png)

FY19 Financial Highlights (Source: Company Reports)

Details of Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of Baby Bunting Group Limited. AustralianSuper is the largest shareholder in the company, with a percentage holding of 10.74%.png)

Top 10 Shareholders (Source: Thomson Reuters)

Increased Profitability and Stability in Balance Sheet: During 1H20, gross margin of the company stood at 36.9%, higher than the industry median of 11.4%. In the same time span, EBITDA margin of the company stood at 12.8% as compared to the industry median of 7.4% and net margin of the company was 2.6%. A higher gross margin with an increase in EBITDA margin indicates that the company is managing its costs well and is able to convert its revenue into profits. During 1H20, Return on Equity of the company witnessed an improvement over the past two corresponding halves and stood at 5.2%, up from 4.4% in 1H18. This indicates that the company is well deploying the capital of its shareholders and is capable of generating profits internally. In the same time span, current ratio of the company witnessed an improvement over the previous half and stood at 1.17x, up from 0.97x. This indicates that the company is liquid enough to pay off its current liabilities using its current assets. During 1H20, Assets/Equity ratio of the company stood at 3.01x as compared to the industry median of 3.32x. This indicates that the business is financed with a significant proportion of investor funding and a small amount of debt, resulting in a financially stable balance sheet..png)

Key Margins (Source: Thomson Reuters)

Strong Growth in Sales and Improvement in Gross Margin: The company has recently released its interim results for the period ended 31 December 2019, wherein it reported significant progress on several operational objectives for the year. The company witnessed a rise in number of stores, improved sales and growth in market share. During 1H20, total sales of the company went up by 8.1% to $186.4 million, and EBITDA witnessed an increase of 21.7% to $14.3 million. The company has seen a healthy start to the second half with a growth of 5.7% in sales, both in-store and online. During 1H20, gross profit of the company was $68.9 million, reflecting an improvement of 15% on the prior corresponding period. In the same time span, gross profit margin has witnessed a substantial growth of 223 basis points to 36.9%. This was mainly as a result of working with supplier partners on range improvements, improvements in trading terms, optimizing supply chain opportunities and increase in direct import volumes. The company has also opened three new stores during the first half, bringing the total number of stores to 56 across Australia. The decent financial and operational performance of the company enabled the Board to declare a fully franked interim dividend of 4.1 cents per share which was paid on 13 March 2020. The company also reported a stable balance sheet with a cash balance of $10.4 million and inventory of $80.8 million..png)

Pro Forma Sales (Source: Company Reports)

Future Expectations and Growth Opportunities: The company had a solid start to FY20 and is on track to deliver significant results in the year. It is focusing on capitalizing on the market share opportunities which may arise due to competitor closures and is aiming to secure any potential property opportunities from the Toys R Us / Babies R Us store network. BBN also brought forward some investment in capability, people and systems to support the market share opportunity and is targeting to alleviate its gross margin without compromising its consumer value. The company is in its final stage of completing its latest network plan review, incorporating the addition of shopping centre format stores, store trading performance, updated market share performance post competitor landscape changes and ongoing changes and shifts in the retail landscape. BBN is leveraging its scale to deliver improved ranging; service offers and profitability.

The company also expects to open one new store in 2H20, assuming no disruption from coronavirus. Baby Bunting will continue to trade in stores, online and via click & collect, supporting parents and parents-to-be who are well advanced in pregnancy. However, the company has withdrawn the previously issued FY20 earnings guidance owing to the increased uncertainty.

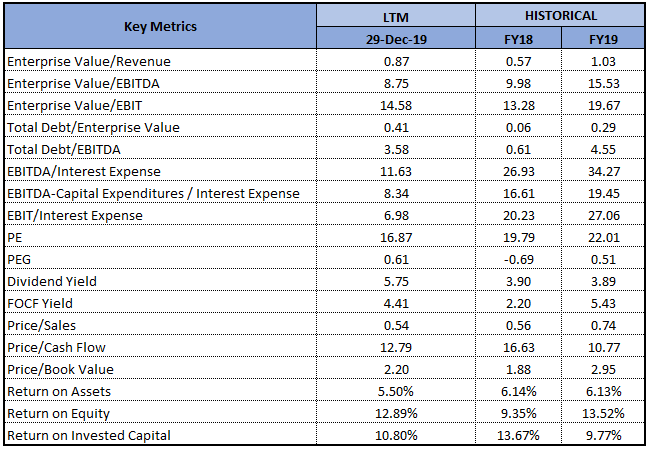

Key Valuation Metrics (Source: Thomson Reuters)

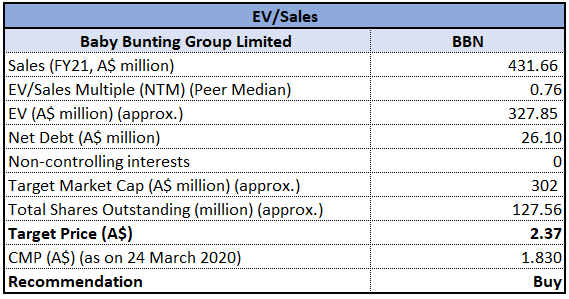

Valuation Methodology: EV/Sales Multiple Based Relative Valuation Approach

EV/Sales Multiple Based Relative Valuation Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTN: Next Twelve Months

Stock Recommendation: As per ASX, the stock of BBN is trading very close to its 52-weeks’ low level of $1.510, proffering a decent opportunity for accumulation. During the second half to date (30 December 2019 to 22 March 2020), total sales growth of the company stood at 12.4%, and comparable store sales growth was 6.2%. The company is making appropriate adjustments to reduce costs and capital expenditure and is continuously investing in business transformation to build capacity for future growth. Considering the trading levels, decent financial performance, improvement in margins and modest outlook, we have valued the stock using EV/Sales multiple based relative valuation approach and have arrived at a target price with an upside of lower double-digit (in percentage terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $1.830, up by 14.375% on 24 March 2020.

.png)

BBN Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...