Kalkine has a fully transformed New Avatar.

Company Overview: Baby Bunting Group Limited is a retailer of baby goods, primarily catering to parents with children from newborn to three years of age and parents-to-be. The Company is engaged in the operation of Baby Bunting retails stores and its online store, www.babybunting.com.au. The Company's product categories include prams, cots and nursery furniture, car safety, toys, babywear, feeding, nappies and associated accessories. The Company offers over 6,000 products. The Company sells private label and exclusive products. Private label products are sold by the Company under its own brand, 4Baby. The Company operates approximately 40 stores across all Australian states and territories, except Northern Territory and Tasmania. The Company offers additional services to its customers, including lay-by, car seat fitting, parenting rooms, which include baby weight scales, and an in-store/online gift registry.

.png)

BBN Details

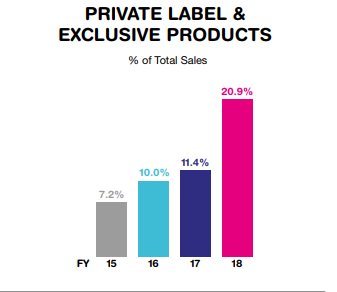

Opening of New Stores Supported Top-line Growth: Baby Bunting Group Limited (ASX: BBN) happens to be the leading specialty retailer of the baby goods which mainly caters to the parents, especially those with children from new-born to 3 years of age as well as parents-to-be. Mr. Matt Spencer is the Managing Director and CEO (or Chief Executive Officer) of Baby Bunting Group while Mr. Darin Hoekman is the CFO of the company. On February 19, 2019, the company’s market capitalization stood at ~$275.64 million and it is having the annual dividend yield of 2.66% (according to Australian Securities Exchange or ASX). The company had generated sales amounting to $303.1 million in FY 2018 reflecting the rise of 9% on the YoY basis on the back of the growth witnessed from opening of the 5 new stores in FY 2018 as well as annualizing benefit of the 6 stores which were opened in FY 2017, and these aspects supported the company’s top-line growth in FY 2018. The growth in the comparable store sales, in FY 2018, was flat on a YoY basis. The company stated that price deflation, which was of 3.6%, constrained the comparable stores sales growth. The primary reason for the price deflation was because of significant price discounting throughout the year by the distressed retailers. The sales from the private label and exclusive products witnessed a rise of 100% in FY 2018 on a YoY basis. It represented 20.9% of the total sales in FY 2018, i.e. an increase from 11.4% in FY 2017. The growth was mainly encountered by the support of key suppliers expanding the range of their products sold exclusively via Baby Bunting. Over past five years to FY 2018 (FY 2014- FY 2018), the company has witnessed an improvement in the return on equity (or ROE), which looks attractive. In FY 2014, the company’s ROE stood at 6.6% while in FY 2018, it was 9.2%.

.png)

Improving Sales and Private label & Exclusive Products as a % of Sales (Source: Company Reports)

Decent Standing from Net Margin Perspective: Baby Bunting Group is progressing well when it comes to its net margin as it has improved in the five years to FY 2018 (FY2014-FY2018) under the tight macroeconomic scenario which reflects the company’s capability to convert its top line into the bottom line. In FY 2018, the company’s net margin was 2.9% while in FY 2014 it was 2.7%. The company’s gross margins stood at 33.3% in FY 2018 which is higher than the industry median of 26.5%. The company’s liquidity position has also improved from the past five years to FY 2018 (FY2014-FY2018) placing it in a better position to make further deployments towards growth catalysts. In FY 2014, its current ratio stood at 1.31x while in FY 2018 it was 2.06x.

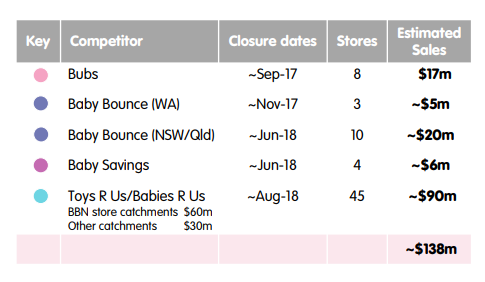

As demonstrated in 2018 AGM presentation, there have been changes with respect to the competition in the markets since September 2017. The changes with regards to the competitive landscape with the closure of Bubs, Baby Bounce & Babies R US gives a substantial opportunity for the BBN moving forward.

Changes in the Market in terms of sale (Source: Company Reports)

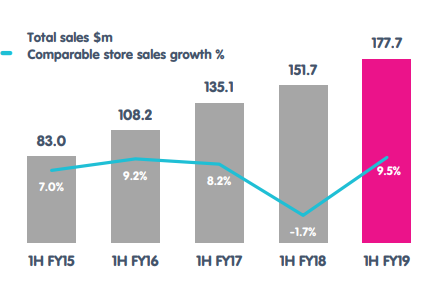

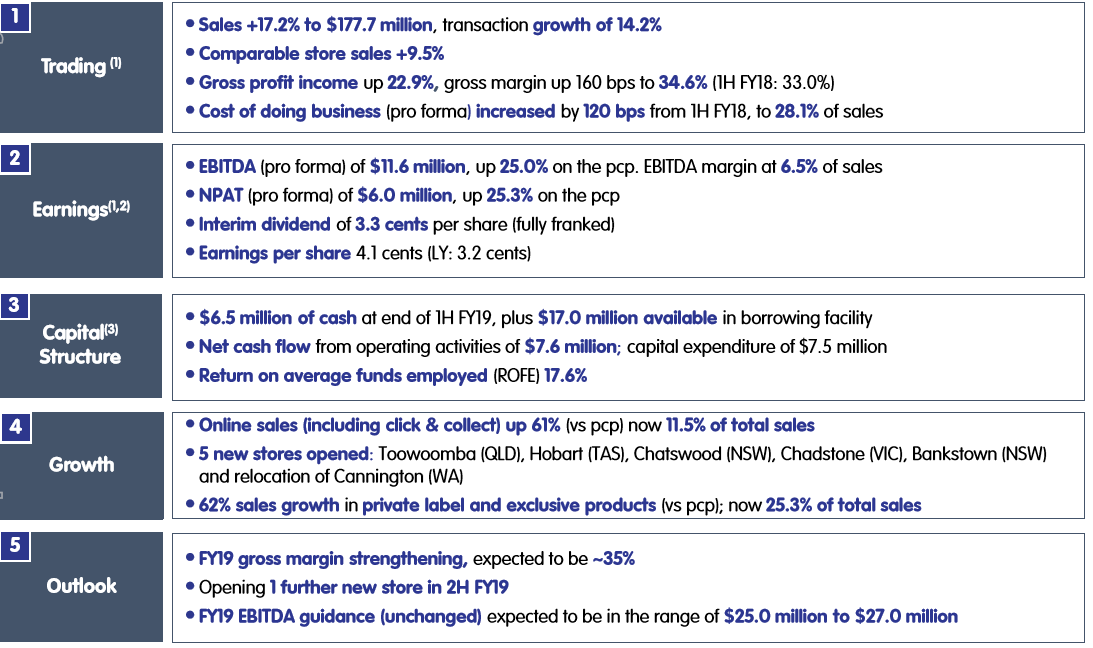

Sales Rose 17.2% for 27 weeks ended December 30, 2018: Baby Bunting Group’s total sales amounted to $177.7 million which reflects the rise of 17.2% on prior corresponding period or PCP. In the 27 weeks ended December 30, 2018, the company’s gross profit witnessed the rise of 22.9% and stood at $61.5 million and its gross margin stood at 34.6% reflecting an improvement of 160 basis points or bps. The recovery in the gross profit margin was witnessed on the back of increases in the direct overseas purchasing, improvements with respect to the supply chain as well as further expansion of private label and exclusive products. The company’s online sales represented 11.5% of the total sales for the FY 2019 half year which implies the rise of 61% as compared to the prior corresponding period. Based on the first half year performance, the company has made an announcement of the interim fully franked dividend which amounted to 3.3 cents per share, and the record date happens to be March 1, 2019 while dividend payment date is March 15, 2019.

1H FY 2019 Total Sales and Comparable Store Sales Growth (Source: Company Reports)

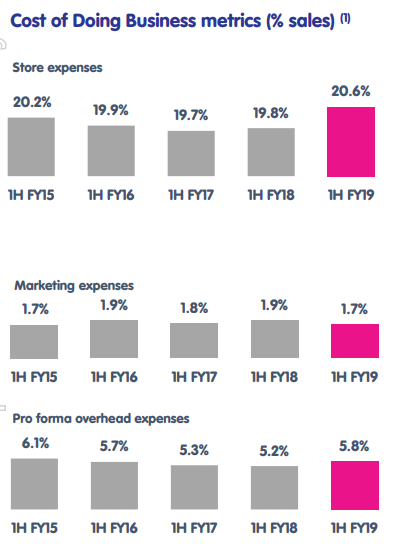

Future Growth Would be Aided by CODB: Baby Bunting had stated that in 1H FY 2019, its CODB (pro forma) was 28.1% of the sales. The company’s store expenses witnessed a rise of $6.7 million as compared to PCP. These expenses got influenced by the timing impact of opening three stores in December, enhanced award wage cost around 3.5%, and growth in Afterpay/ Zip Pay transactions which has resulted in the rise of merchant charges by 30 basis points. However, a rise in the store expenses also reflects an amount of $4.2 million which is related to the new as well as annualizing stores. This strategic deployments towards opening new stores, marketing campaign, and overhead expenses might drive future growth of the company.

CODB Metrics (% Sales) (Source: Company Reports)

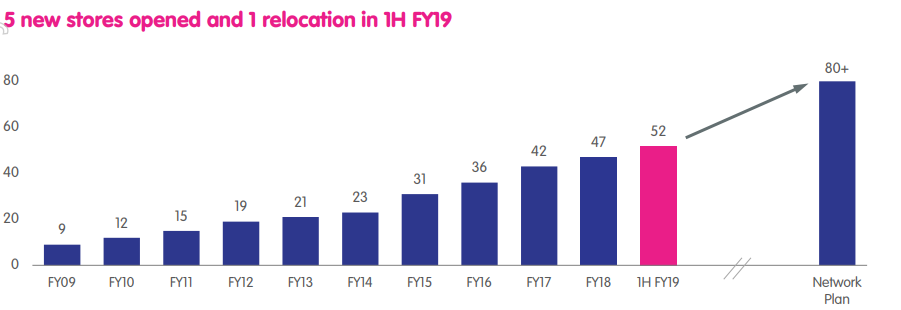

Business Strategy: Baby Bunting Group’s growth strategy revolves around deployments towards the digital initiatives to deliver best possible customer experience throughout the channels, deployments so that the sales can witness growth from the existing stores, growth from the new markets as well as improvement with respect to the EBITDA margin. With regards to investment to grow the sales from the existing stores, the deployments towards the customer experience, digital marketing as well as ancillary store services and store to door online fulfilment hubs might support the company. In 1H FY 2019, the company had opened five new stores, as well as relocated one store. This equates to 52 stores as on 30 December 2018 and the company intends to open more than 80 trade catchments on the basis of demographic, location, and competition parameters.

Growth from New Markets (Source: Company Reports)

Drivers for Future: In 2018 AGM presentation, Baby Bunting had provided certain information related to the supply chain strategy. The evolution of the supply chain would be lowering the current cost model, improve customer experience via speed to market as well as increase the on-shelf stock availability. There are expectations that the company would be posting the EBITDA between $25 million-$27 million in FY 2019 which demonstrates the rise of approximately 34%- 45% excluding the employee equity incentive expenses.

The guidance is based on the assumption that the comparable store sales growth would be in the mid to high single digits for the year, gross margin would be around 35% in FY 2019 as well as total 6 new stores have been slated for opening for FY19. In the 27 weeks to December 30, 2018, out of the total sales, 25.3% was garnered from private label and exclusive products which reflects the rise as compared to the prior corresponding period as well as 2H FY 2018. In pcp, the percentage was 18.4% while in 2H FY 2018, it was 23%. Over the long-term, the company has been targeting 50% of total sales from the private label and exclusive products. Also, the company has taken immediate actions to grow the market share as well as profitability in FY 2019 which includes capitalising on market share opportunities from the closures of the competitor, stabilising the gross margin without compromising the value, securing the prime sites for the store network, driving private label and exclusive product expansion program as well as deployment with respect to people and systems to support the growth.

1H FY19 Performance Summary (Source: Company Reports)

Stock Recommendation: On the daily chart of Baby Bunting Group, Exponential Moving Average or EMA has been applied and default values were used for the purposes. After careful observation, it was noticed that the company’s stock price had crossed the EMA and, after the crossover, had trended in the downward direction which signifies some bearish trend.

However, fundamentally, there are expectations that the company might benefit from the rollout of the new stores as well as from the deployments towards the digital initiatives moving forward. Moreover, the company’s gross profit margin has also witnessed a recovery which might attract the market players’ attention. Also, another primary factor which could drive the growth of the company moving forward is the changes which have been done with respect to the competitive landscape which has provided the company with a significant opportunity.

BBN stock has delivered the return of -8.02% in the span of previous six months while, in the period of last three months, BBN’s stock posted the return of -0.91% and is trading slightly towards 52-week higher levels with PE multiple of 26.59x. Hence, considering the above-mentioned factors and current trading level, we give a “Speculative Buy” recommendation on the stock at the current market price of A$2.210 per share (up 1.376% on February 19, 2019).

BBN Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...