Company Overview - AWE Limited (AWE) is an energy company focused on upstream oil and gas exploration and production. The Company’s segments include South East Australia, Western Australia, New Zealand, the United States, Indonesia and Exploration Activities. South East Australia includes production and sale of gas, condensate and Liquefied petroleum gas (LPG) from the BassGas and Casino gas projects. Western Australia includes production and sale of crude oil, gas and condensate from the Cliff Head oil project and an oil and gas fields in the Perth Basin, onshore, Western Australia. New Zealand includes production and sale of crude oil from the Tui Area oil project. The United States includes production and sale of gas, LNG and condensate from the Sugarloaf AMI (Texas, the United States).

Analysis - On 15

th May, the company announced that it has secured a new four-year $400 million secured multicurrency syndicated bank loan facility to replace its existing unsecured $300 million unsecured loan facility. According to the CFO of the company Ayten Saridas, the new facility further strengthens company’s capacity to deliver its expanding portfolio of major growth projects and take advantage of emerging opportunities. The company had net debt of $47 million as on 31st March 2015, comprising cash of $62 million and $109 million of drawn debt from the loan facility.

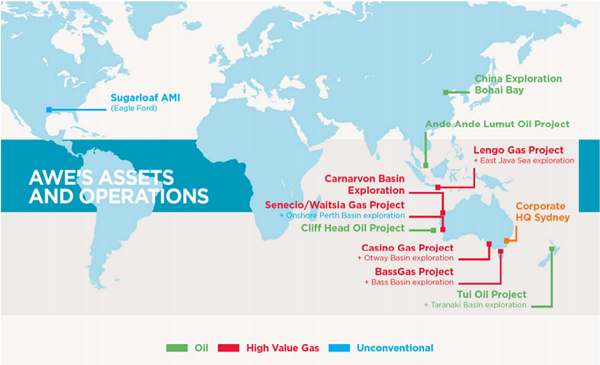

Geographical Reach (Source - Company Reports)

Geographical Reach (Source - Company Reports)

The company also published its latest quarterly report on 29

th April with results up to 31

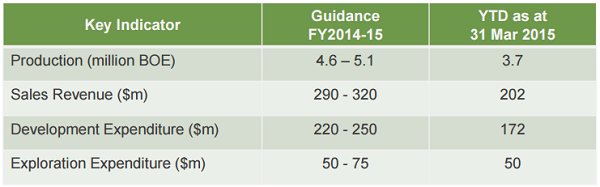

st March 2015, whose highlights were a 46% decline in quarterly sales revenue and two new offshore exploration permits. The decline in revenue was attributed to lower production, as well as significantly lowers oil prices. The average realized oil and condensate price for the quarter was $57.33/bbl compared to $80.78/bbl for the previous quarter. Quarterly production was 1.11 mmboe that is a decline of 6% from the previous quarter, which was attributed to facilities shut down for major redevelopment activity. However financial year to date production was 3.67 mmboe, which is in line with full year guidance.

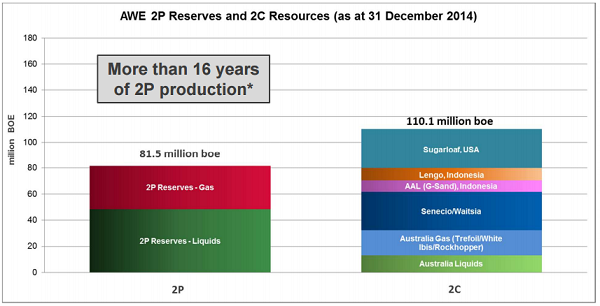

Strong base of reserves & resources (Source - Company Reports)

Strong base of reserves & resources (Source - Company Reports)

The quarterly revenue was $41 million, of which $18 million was from gas, $3 million from LPG, $13 million from Condensate and $7 million from oil. Liquids provided for 46% of total quarterly production and gas providing 54%. Field EBITDAX for the period was $15 million down 60% as compared to previous quarter mainly due to lower production and significantly lower oil prices. Field operating costs including royalties of $4 million were $27 million down 34% on the previous quarter. Development expenditure for the March quarter was $77 million an increase of 46% over the December quarter. Exploration expenditure for the quarter was $10 million up 38% on the previous quarter.

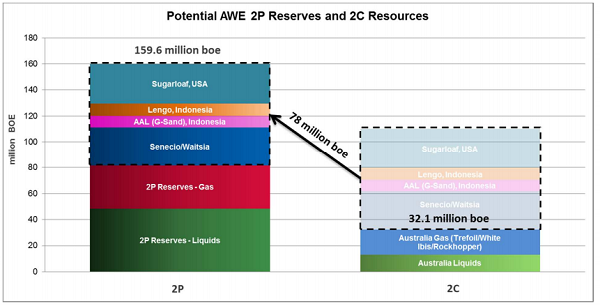

Potential Reserves & Resources (Source - Company Reports)

Potential Reserves & Resources (Source - Company Reports)

The future growth of the company is built on three key platforms – high value gas, oil and unconventional energy sources. High value gas is focused on markets with pricing and demand upside, which are identified as Australia and Indonesia. There is a long-term price upside on oil and the currency play is also expected to be favourable. The key markets for oil are Indonesia, China, New Zealand and Australia. Unconventional energy sources are which are liquid rich and are placed close to infrastructure sites. USA, Australia and Indonesia are key markets for this energy source. The company plans to increase its production to 10 mmboe and increase EBITDAX to $500 million, without significant capital expenditure. The company’s portfolio of assets spans the full upstream cycle – exploration, appraisal, development and production. The company is an active manager of assets and aims to ensure that AWE’s equity interest reflects the appropriate balance between risk and reward at every stage of lifecycle.

Guidance Maintained (Source - Company Reports)

AWE is well positioned for low prices. Operations of the company continue to perform well, as production is on track to achieve full year guidance. The company is also on track to achieve all the development milestones. The diversified asset base of the company provides it optionality, and an ability to prioritize development and exploration. Gas contracts are currently CPI linked and the company is planning to recontract significant gas reserves and resources. The company is also aiming to cut costs in an environment of low oil prices to maintain margins. The company claims to have already received significant savings on Sugarloaf drillings and completions and opportunities identified to reduce operating costs on a number of assets.

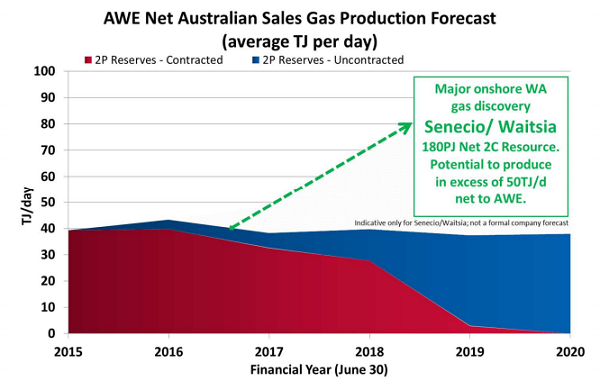

Gas Production Forecast (Source - Company Reports)

Gas Production Forecast (Source - Company Reports)

The company added two major development projects to its portfolio in the last 12 months, the Senecio/Waitsia gas project in the onshore Perth Basin and the Lengo gas project offshore Indonesia. The Perth Basin project, together with BassGas, Sugarloaf and Ande Ande Lumut, are core elements of AWE’s growth strategy. The company’s stated policy has been further exploration of conventional and unconventional potential of Perth basin. One of the major exploration success last year was the Waitsia gas field and the flow testing at Senecio 3 confirms the commercial potential of the conventional Waitsia gas field. Waitsia field appraisal well will commence drilling from May. The company also achieved many critical milestones at Tui, Bassgass, Sugarloaf and Lengo. The company also discovered gas in Irwin-1 well in Perth basin. After the Senecio-3 well flowed at up to 18.5 mmscfd, expectations may be increasing that AWE is sitting on a commercial gas field.

Gas Discovery at Irwin -1 (Source - Company Reports)

Production from BassGas was 201 kboe in the March quarter, 2% below the Dec qtr. There were 23 days of downtime in the March quarter, and whilst AWE flagged 20 days downtime, we had assumed this would be spread between the March and June qtrs. After 39 days' downtime in the December quarter there have been 62 days downtime to date, with more expected in the June qtr. The drilling of the 2 Yolla development wells commenced in March, with production from these wells now unlikely until late in the June qtr.

AWE Chart (Source - Thomson Reuters)

AWE Chart (Source - Thomson Reuters)

Maintaining diversity of production and projects across geographies is one of the key components of company’s growth strategy. The company was awarded two new exploration permits in Western Australia and expansion of onshore exploration permit in New Zealand was approved in the latest quarter ending on 31

st March 2014. The company made gas discovery in the Dongra Wagira formation at the Irwin 1 exploration well.

While the interruptions at both Tui and BassGas have weighed on production, solid initial production rates at Pateke-4H, limited planned downtime and the ongoing ramp-up at Sugarloaf should support production in the current quarter which will see AWE deliver towards the top end of its guidance range.A robust balance sheet and strong operating cash flows are crucial in allowing the company to stay in control of its exploration and development agenda and deliver growth. Given the strength of AWE’s assets and balance sheet. We believe that the stock is worth buying at the current price of $1.39.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...