Company Overview - AWE Limited (AWE) is an energy company focused on upstream oil and gas exploration and production. The Company’s segments include South East Australia, Western Australia, New Zealand, the United States, Indonesia and Exploration Activities. South East Australia includes production and sale of gas, condensate and Liquefied petroleum gas (LPG) from the BassGas and Casino gas projects. Western Australia includes production and sale of crude oil, gas and condensate from the Cliff Head oil project and an oil and gas fields in the Perth Basin, onshore, Western Australia. New Zealand includes production and sale of crude oil from the Tui Area oil project. The United States includes production and sale of gas, LNG and condensate from the Sugarloaf AMI (Texas, the United States).

Analysis – AWE delivered a small 4% production miss for the June Quarter. The miss was driven mainly by the timing of Sugarloaf wells – the operator drilled 40 wells but only brought seven online. It is now on track to drill the 100 – 110 wells originally targeted for calendar year 2014, which will flow through to production in FY15. We like AWE based on its solid existing production base and projects that carry a strong likelihood of success – BassGas MLE Phase 2, Sugarloaf Austin Chalk and AAL.

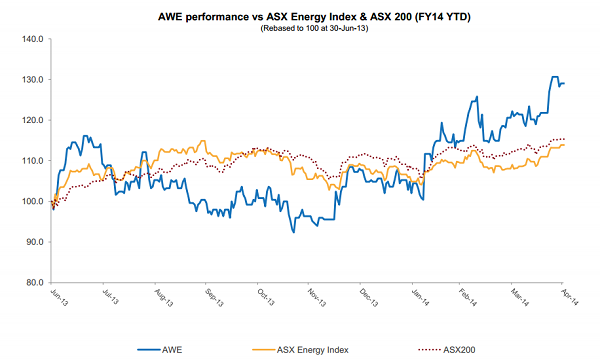

AWE Share Performance (Source - Company Reports)

Quarterly production was 1.31mmboe and revenue was A$60m. The large revenue miss was mostly because Tui made zero oil shipments during the quarter, which added 0.17mmbbls in Tui inventory to largely unwind over 1H FY15. FY14 production of 5.6mmboe exceeded conservative guidance of 5.0-5.5mmboe and FY14 revenue of A$328m exceeded guidance of A$290-320m on production and higher A$ oil price. FY14 capex of A$201m was better than guidance of A$210-230m.

The operator Marathon drilled just eight wells in Sugarloaf AMI in the March Quarter but dramatically increased the rate to drill 40 wells in June Quarter. It has now drilled 48 out of the 100-110 wells it intended to spud at the start of CY14. Because of the slow start and the tendency to change its plans we were skeptical that Marathon would allocate enough rigs to the area. We previously assumed 80 but now assume 105 wells in CY14. Note that only seven gross wells were added to production in June Quarter to enable efficient batch fraccing /completion. We believe the 41 wells in inventory will translate to a large uplift in Sugarloaf production in 2HCY14 as they are brought online.

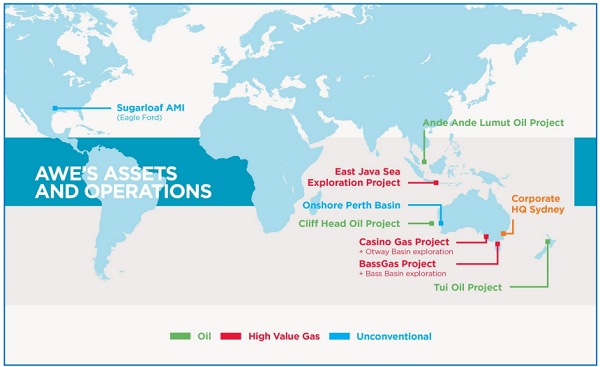

AWE Assets (Source - Company Reports)

AWE acquired 100% interest in the Northwest Natuna PSC, in early 2012 for USD139 million. The Northwest Natuna PSC contains the Ande Ande Lumut (AAL) Oil project and a Plan of Development for the project has been approved by the Indonesian regulator. The optimised development plan involves drilling 33 longer reach horizontal wells into the K-Sand reservoir to achieve total recover of 101 million barrels of oil, an increase of 25 million barrels over the original development plan. An independent audit and certification of the AAL field was completed by Perth-based consultant, RPS Energy Services, in May 2013. The timing of final investment decision for AAL appears to have slipped by 6 months. It is now mid CY15 and first oil is expected in late CY17.

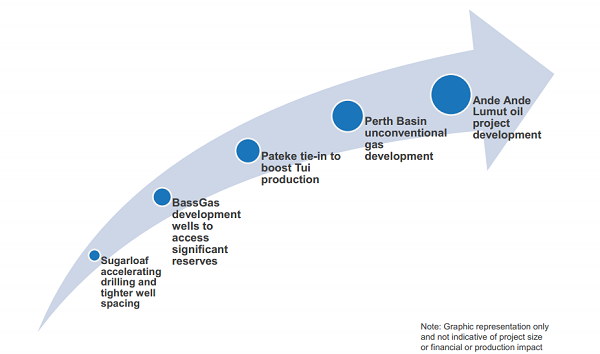

AWE Growth Opportunities (Source - Company Reports)

Cliff Head production was disappointing but this was more than compensated by the outperformance of the much larger casino area assets. Despite performing well recently we still believe that a fundamental gap persists between share price and fair value. We think a further overrun beyond the current budget for the BassGas MLE Phase 2 is now reflected in the share price. Identifying specific catalysts for AWE is troublesome. We were surprised with the strong outcome of the Ande Ande Lumut farmout to Santos recently did not result in a more permanent rerating. Perhaps the market is waiting for FID in FY15. In any event an operator of Santos’ experience represents a strong stamp of approval in our view.

AWE Production Growth (Source - Company Reports)

We think many of AWE’s other assets are solid potential earners. We like the 10% of Sugarloaf AMI which is in the liquids rich zone of the Eagle Ford shale in Texas. The Sugarloaf AMI covers a number of leases totaling approximately 24,000 acres, located in the Eagle Ford Shale reservoir, which is being developed through the innovative use of long-reach horizontal drilling and multiple fracture stimulations of the shales. The Perth Basin unconventional frac testing showed modest flow rates – these may be significantly improved upon as the well designs move from exploration towards more commercial pilot configuration. Despite the dry nature of the gas we think it has potential due to proximity to the Perth market and high Western Australian gas prices. AWE is studying feasibility on its 50-100bcf (8.6-17.2mmboe) Senecio tight gas field.

AWE New Permits (Source - Company Reports)

AWE continues to test the unconventional potential in the Perth Basin. Positive gas flows were achieved from the High Cliff Sandstone (0.78mmscfd) as well as 1.35 mmscfd from the Sensecio-2 well. The acreage is close to existing infrastructure and has the potential to supply the domestic WA gas market, where long term gas prices have risen above $8/GJ. AWE has got substantial uncontracted domestic gas position. Industry experts forecast the domestic gas price to rise sharply over the next 5-10 years. Over 50% of AWE’s 2P gas reserves are uncontracted.

AWE Chart (Source - Thomson Reuters)

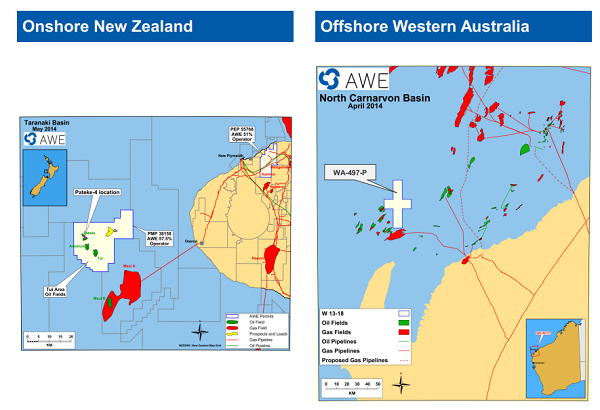

Also strategic portfolio management is being done by AWE which includes :- 1) Sale of 50% interest in the Ande Ande Lumut Oil project to Santos. 2) Acquired additional 15% in Tui Oil fields and 6.25% on Oi exploration well from Mitsui E&P Australia. 3) Acquired a 60% working interest in Vic/P67 from WHL energy.4) Sales of Yemen exploration asset (Block 7) to Petsec Energy announced. 5) Awarded new onshore exploration permit, PEP 55768 in New Zealand’s Taranaki region. 6) Awarded new offshore exploration permit WA-497-P in the North Carnarvon Basin, Western Australia.

AWE is on target to achieve its strategic objectives. It has got a highly liquid balance sheet with significant capacity. With production assets performing well and active management of asset portfolio, AWE is on track to maximize the value of its existing portfolio along with continuing to review new opportunities. We put a BUY recommendation on the stock at the current price of $1.745.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...