Company Overview - Aveo Group Limited, formerly FKP Property Group, is an Australia-based company. The principal activities of the Company include: investment in, and development and management of, retirement villages; development for resale of land and residential, retail, commercial and industrial property; investment in, and management of, income producing retail, commercial and industrial property; commercial, industrial and residential building and construction for the Group; and funds and asset management. The Company operates in two segments: Retirement, which develops and operates retirement villages and aged care facilities to produce rental and other income; and Non-retirement, which develops residential, commercial and retail property. Developed commercial and retail property may be sold or held to produce rental income and capital appreciation. The Company has interests in approximately 75 retirement villages in Queensland, Victoria, Tasmania, New South Wales and South Australia.

Analysis - Aveo Group (ASX: AOG), the leading, well known owner, operator and manager of retirement communities spread across Australia, reported the underlying net profit after tax of $ 24.1 million for the six months ended 31 December 2014 (FY15) which represents an increase of 26% over the same period in the previous year. The encouraging results and the performance to date have led the company lift its previous guidance from a 15% to 20% increase on FY14 underlying profit to a figure in excess of 20% on FY14 result.

A new group finance facility of $275 million was finalised in December 2014 which consolidated and refinanced the existing facilities. The new structure greatly simplifies and clarifies the debt structure along with improvements in margins. $150 million in interest rate hedges have reduced the level to 47% of outstanding debt and reduce the average weighted cost of debt to 5.8%. The year FY15 started with $585 million worth of non-retirement assets to be spun off. From FY15 to FY18, $ 225 million of the proceeds will be invested in retirement development working capital. The balance of the surplus will include increasing the capital in retirement development, increasing the level of acquisitions and securities buybacks.

HY15 Results (Source: Company Reports)

As per the company, the strong performance for FY2015 is directly a result of the transformation to the pure retirement strategy implemented in the middle of 2013. The company is on track to deliver immediate returns on retirement assets of between 6% and 6.5% by FY2016. Though there is more to be achieved, the progress attained in the transformation to a pure retirement business could provide even greater value for shareholders in the coming years. The results for HY2015 indicate sales from the Retirement established business touching the record figure of 370 units sold. The total profit contribution from the same business was $23.8 million which was a growth of 18% over the previous year and the momentum was driven by more lucrative margins. The decline in underlying EPS from five cents per share to 4.8 cents per share was entirely because of the additional shares which were issued as part of the capital raising exercise in December 2013. Net assets of $1.5 billion were up 2% from June 2014; and NTA per stapled security of $2.85 grew by 3% from June 2014.

With record unit sales achieved and higher transaction margin levels, the Retirement established business again performed strongly on sales volumes for non-new product of 358 units which grew 11% over the previous year, and drove portfolio turnover to 11.4%, indicative of a leading position in the industry and towards the top of the target range of 10%-12%. Sales prices were in line with valuation pricing while deposit levels continued to be robust providing momentum into the second half. The Business is on track to improve on last year’s record sales levels.

Established Business Results (Source: Company Reports)

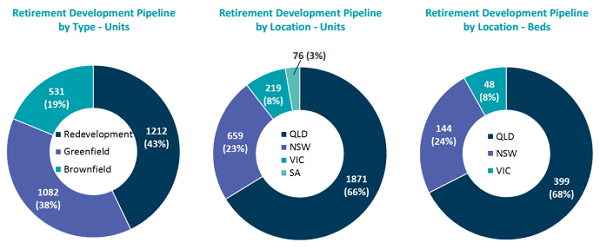

The Retirement division achieved considerable growth in contribution from its development activities driven by higher margins and produced development revenues of $9.6 million, up 174% from the previous year. Development projects currently in hand and scheduled for completion in FY15 include Albany Creek (12 units), The Parks (14 units); Cleveland (7 units) and Durack (14 units) all in Queensland; Island Point), NSW (8 units); and Mingarra, Victoria (7 units). Planning and construction activity is also progressing well for 182 units to be delivered in FY16 to meet the development profit target of $10 million to $12.5 million in that year. The company continues to target a further 224 deliveries in FY17 and 553 in FY18. Acquisitions to be announced shortly should increase the targets for FY17 and FY18 delivery.

As part of the pure retirement focus, plans have been finalised to enhance and build up in-house aged care capabilities on a stand-alone basis. This approach enhances higher potential returns while the company continues to have operational control across all aspects of care offering in its village. Plans have also been announced to expand the present 209 aged care beds to 800 over the next six years. Strategic relationships have been finalised for in home low care support services with RDNS covering 47 villages across NSW, Queensland and Victoria; RSL Care covering 15 villages in Queensland and St Ives covering 10 villages in Victoria, all of which will operate on a revenue or profit sharing basis. In addition, the company has recently completed the acquisition of 50% interests in two related health businesses, Mobile Rehab and The Physio Co. These rapidly expanding businesses will focus on physiotherapy services to the aged and are expected to contribute to the goals of $ 3 million to $ 3.5 million in care earnings by FY16 and $ 6.5 million to 8 million by FY18.

Capital Management_HY15 Metrics (Source: Company Reports)

Non-retirement assets continue to be spun off and the sale of the commercial property at Miller St in Pyrmont, Sydney has been completed for $20 million. Previously announced sales of Albion Stage 1 and Gasworks Stage B have also been completed for $ 24 million. Negotiations are in progress on the potential sale of the Gasometer 1 & 3 retail/commercial assets in Brisbane. The divestment of non-retirement assets is on track to hit the target 20% weighting by FY16. The sales of residential land were down in the half-year but volumes for FY15 are expected to be considerably higher than the figure for FY14. Land banks at Rochedale are targeted for sale by FY18 and at Point Cook and Peregian Springs by FY19.

The considerable progress with pure retirement strategy in HY15 and the transformation continues to gain momentum. The Retirement established business with its record sales levels, the retirement development pipeline on track to meet profit and unit delivery targets in FY15 and FY16, and the increased care and support services will continue to strengthen. The non-retirement assets provide a source of strong cash flows for reinvestment in retirement growth projects. The guidance of a full year FY15 distribution of 5 cents per security has been reaffirmed.

Interest Bearing Liabilities and Gearing History (Source: Company Reports)

We view AOG as essentially a retirement operator which also has other businesses because roughly 65% of their earnings come from the retirement business. Residents at the units have an obligation to pay deferred management fee to the company and this constitutes the principal source of income though there may also be revenues from capital gains and the development of retirement units. We can see a number of positive indicators for attractive growth fundamentals both for the industry as a whole and this company in particular.

Development Pipeline (Source: Company Reports)

The demographics of the Australian population suggest that an ever-increasing number of people may be forced to consider retirement units. Moreover, many of these future retirees may have insufficient income to maintain the retirement lifestyle that they would like. However, many of them have considerable amounts of home equity in their family homes and, considering that purchase prices for retirement homes are below family home prices, the retirement home could be an attractive investment alternative for this home equity.

AVEO Daily Chart (Source - Thomson Reuters)

We believe that the company has sound long-term growth fundamentals and, with this in mind, there is room for considerable price growth on the present value of the stock. In other words, there seems to be a buying opportunity with a price per earnings ratio of about 24. There has been ~36% jump in the price in 12 months to 30 April 2015 indicative of good growth.

Accordingly, we put a BUY recommendation for this stock at the current price of $2.72.

.png)

.png)

.png)

.png)

Please wait processing your request...

Please wait processing your request...