Company Overview - Automotive Group Holdings Limited (AHE) is a diversified automotive retailing and logistics group with operations in Australia and New Zealand. AHE has three segments: automotive retail, other logistics and property. The automotive retail segment has 132 dealerships franchise sites operating within the geographical areas of Australia and New Zealand. AHE's other logistical operations segment comprises AHG’s automotive parts warehousing and distribution businesses, motorcycle distribution and vehicle storage and engineering. The property segment comprises AHG’s direct property interest in land and building. In July 2013, the Company announced that it has completed the acquisition of the Jason Mazda dealership in Perth’s northern suburbs. In September 2013, the Company announced that it has completed the acquisition of the business of Davie Motors Holden in New Zealand. In August 2014, Automotive Holdings Group Ltd completes acquisition of Bradstreet Motor Group.

Analysis - Automotive Holdings Group Limited (AHE) is known as a diversified automotive retailing and logistics group and is the largest provider of temperature-controlled transport and cold storage services. During the Annual General Meeting 2014, the Company reported that its revenue is in excess of $4.7 billion and market capitalization of ~$1.2 billion. AHE also allegedly has a strong interest cover. The business of the Company includes three core divisions, namely, Automotive, Refrigerated Logistics and Other Logistics.

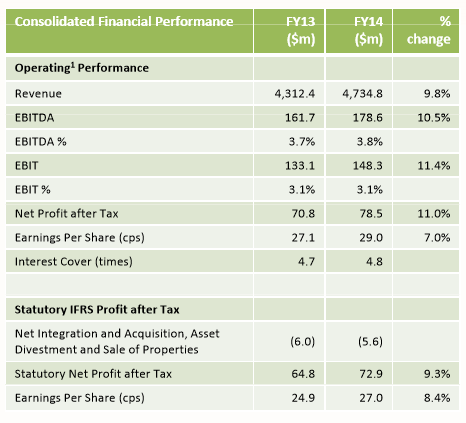

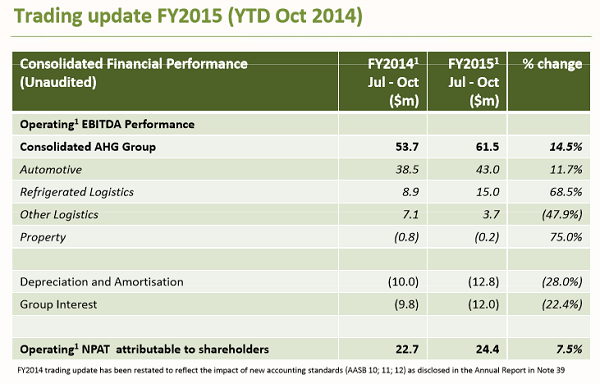

Financial Performance (Source – Company Reports)

Financial Performance (Source – Company Reports)

AHE now has about 169 franchises at 95 dealership across four Australian states and New Zealand under the Automotive Division. The acquisition of the Bradstreet Motor Group in Newcastle in August 2014 is the key highlight. The Other Logistics operations include AMCAP, Covs, Genuine Truck Bodies, Vehicle Storage and Engineering, and WMC. AHE now employs more than 7,300 people across Australia and New Zealand with the acquisitions of Scott’s, JAT and the Bradstreet Motor Group.

Refrigerated Logistics (Source – Company Reports)

Refrigerated Logistics (Source – Company Reports)

The Company believes that its overall macro settings look reasonably supportive with recent acquisitions enhancing profitability. Primarily, AHE has the confidence in having a high quality business reinforced by organic growth and acquisition prospects. During the year ended June of 2014, sales were $4.73 billion indicating an increase of 11.1% as opposed to 2013 ($4.26 billion). FY14 was the fifth consecutive year of sales increases. During the 12 months ending 30 June 2014, AHE paid dividends totaling $0.21 per share.

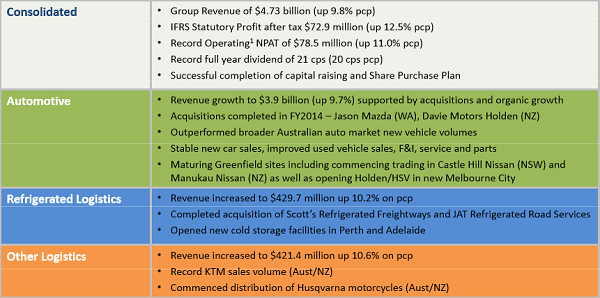

Division-wise Summary (Source – Company Reports)

Division-wise Summary (Source – Company Reports)

An overview of AHE’s divisional performance in FY14 reveals that its Automotive business witnessed strong revenue and profit growth with effective integration of new acquisitions in WA, VIC and NZ in support of the successful market campaigns. The increased new vehicle sales accompanied multiple revenue streams. It is also noted that Melbourne City Holden/HSV, Melbourne City Hyundai, Clarkson Nissan and Manukau Nissan (NZ) have been opened. The Bradstreet acquisition also finalized with 13 franchises at seven dealerships (completed in August 2014). This segment outlook suggested that there is a strong retail demand in support from manufacturer incentives. The private sector sales remain the key strength.

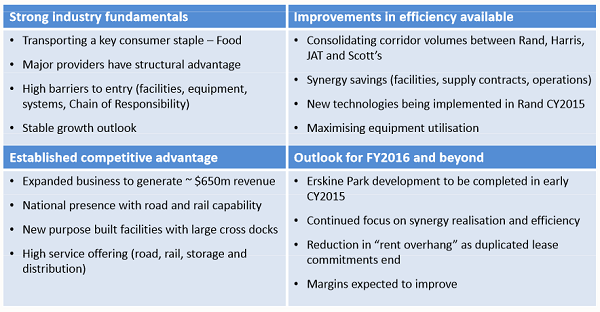

For the Refrigerated Logistics, FY14 was reported to be little challenging in view of weather extremities and costs associated with new facilities in Perth and Adelaide added to provide additional storage capacity. The acquisition of Scott’s and JAT strengthened the Company’s brand of Australia’s largest Refrigerated Logistics provider. Further, AHE believes that the new Erskine Park (NSW) cold store will be complete by early 2015. The Company expects that its Refrigerated Logistics division will witness about $650m revenue in FY2015 based on greater customer value proposition and operational synergies. It would also be the primary supplier to national manufacturers, wholesalers and major retailers. Other attributes like the custom?designed facilities, road transport capacity with ~ 370 owned prime movers and ~ 780 road trailers, rail capacity with ~ 420 refrigerated rail containers and humongous network of sub?contractors will be the add-ons.

Outlook for the Refrigerated Logistics Business (Source – Company Reports)

Outlook for the Refrigerated Logistics Business (Source – Company Reports)

For the Other Logistics division, AHE witnessed record sales volume in KTM with unit sales up 14.6% to 8,978 units (7,837 pcp). Further, growth in NZ market for KTM was reported. AMCAP/Covs also performed as per expectations. The other important point was with regards to restructuring GTB/VSE for lean manufacturing. As per the division’s outlook, the Company expects to have continued strong sales from motorcycle division but accompanied with lower FY2015 margins owing to weaker $A. AHE believes that increased model range for both KTM and Husqvarna would help balance weaker $A. Further, tuck & trailer and mining services are expanding in WA and nationally.

Investment Led Growth (Source – Company Reports)

Investment Led Growth (Source – Company Reports)

The recent trading update for Jul-Oct 2014, i.e., first 4 months of FY15 appeared to be in line with expectations. This indicated a continued growth in the Automotive and Refrigerated Logistics divisions with support from acquisitions. In fact, the group EBITDA of $61.5m is reported to be up 14.5% year-on-year with NPAT of $24.4m increased by 7.5%. As per the Company’s trading update, the Automotive division depicted stable trading in established dealerships. Healthy NSW performance aided in equipoising weaker WA market. Growth in New Zealand was witnessed with improved economic position and addition of Davie Motors. The truck market remained slow with volumes substantially down on prior period. AHE further reported that this division is supporting trading losses in Melbourne City greenfield development. The EBITDA was $43m year-to-date which rose by 11.7% based on the aforementioned factors. The Bradstreet acquisition although contributed for half the period is performing as per AHE’s anticipations.

For the Refrigerated Logistics, the trading update FY2015 (YTD Oct 2014) indicated Scott’s/JAT operating well while trading is in line with expectations. AHE mentioned that the cost base in Rand is supporting duplicated facility lease costs of older premises. The operating EBITDA of $15m which was 69% ahead of pcp was reported.

With regards to trading update FY2015 (YTD Oct 2014) for the Other Logistics Division, AHE witnessed EBITDA of $3.7m which was down 48% on pcp. This was primarily owing to KTM EBITDA going down due to weaker $A and new model releases. AHE also stated that Mitsubishi change in Perth metro distribution model has reduced AMCAP EBITDA. There have been some losses incurred in Q1 of FY2015 with regards to VSE/GTB for building up in inventory and transition to lean manufacturing processes.

Trading Update (Source – Company Reports)

Trading Update (Source – Company Reports)

AHE’s expectations for driving shareholder value in FY2015 entails focusing on cost control and managing balance sheet capacity to fund growth; persistently investing in facilities and systems to support growth; maintaining business leading performance; improving returns by applying the Company’s proven auto-dealership model to acquisitions and Greenfield sites; and focusing on integration of Scott’s and JAT to deliver business efficiencies and have synergy savings in FY2015 and beyond.

AHE Daily Chart (Source - Thomson Reuters)

AHE Daily Chart (Source - Thomson Reuters)

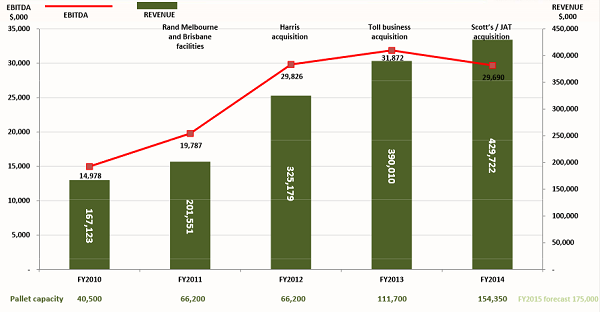

Nonetheless, few factors to be wary of constitute economic slump affecting consumer and business confidence, fluctuations in interest rates affecting finance costs for dealers, acquisition and integration risk in terms of associated costs etc., a flat to marginally down new car market expected in FY15, and execution risk in Logistics business. However, proven business model, healthy balance sheet, and expectation that acquisitions may benefit FY15 revenue by more than $600m, speak for some good positives. For instance, the Logistics division will benefit in FY15 from the Scott’s acquisition and increased Rand capacity. The current capacity of 102,050 pallets may be expanded to 140,250 by the end of FY15.

Based on the foregoing, we put a

BUY recommendation for this stock at the current price of $3.77.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...