Kalkine has a fully transformed New Avatar.

.PNG)

In response to the changing strategic environment in Australia, including increased strategic competition, technological changes, introduction of more capable military systems, etc., the Government has set out some important adjustments to the 2016 Defence White Paper, as stated in the 2020 Defence Strategic Update, issued on 1st July 2020. Three new strategic objectives in the update are - (a) to shape Australia’s strategic environment, (b) to deter actions against Australia’s interests, and (c) to respond with credible military force, when required. The Strategic Update also signals more job opportunities as Australia’s increasingly capable and sovereign defence industry grows.

The 2016 Defence White Paper had set out six drivers that would shape Australia’s strategic environment. These included the roles of the United States and China; challenges to the stability of the rules-based global order; the enduring threat of terrorism; state fragility; the pace of military modernisation in the region; and the emergence of new, complex non-geographic threats. While all these factors remain relevant to the national interest, some of them have accelerated since 2016 and have exposed the country to new challenges. The above-mentioned strategic objectives have been incorporated in response to the changing environment, particularly in relation to the economic and strategic consequences of the COVID-19 pandemic.

2020 Force Structure Plan: The Government released the 2020 Force Structure Plan (FSP), containing adjustments to its Defence capability plans as per the new strategic objectives set out in the 2020 Defence Strategic Update. The FSP builds on investments made in the 2016 Defence White Paper (DWP16) and is a result of a more regular review of Defence policy settings and force structure.

Budget Highlights: Over the next ten years, total Government funding to the Defence sector will be around $575 billion, including ~$270 billion invested in Defence capability to 2029-30. The Government has also provided Defence with funding certainty to deliver on the new strategic defence policy. In the Defence Budget statement, the Government has announced that Defence funding, including Australian Signals Directorate (ASD), will grow over $73.7 billion by 2029-30. The funding budget has been divided into three major categories – (a) Acquisition of new capability which includes the estimated costs of acquiring new capability including military equipment, facilities and infrastructure;(b) Sustainment of existing capability which includes the costs of sustaining existing capability in service and the estimated costs of planned future capability;(c) Workforce which is largely comprised of military employee expenses to support Defence outcomes including military capability..png)

Proportional Capability Investment (Source: Department of Defence)

.png)

Defence Funding – Including ASD (Source: Department of Defence)

Under the plan, the Government talks about adapting to emerging technologies and planning investments as new opportunities arise. These investments will range from the adoption of remotely piloted or autonomous systems for a range of missions, such as air combat, strike, air-to-air refueling, etc., to high-speed missile systems to provide the Government with more deterrence options.

Capabilities Covered in the Force Structure Plan: Investments in the Defence sector will be focused on capabilities such as, enhancing Defence’s posture and partnerships in the Indo-Pacific region, more durable supply chain arrangements and strengthened sovereign industrial capabilities to increase ADF’s self-reliance, capabilities to respond to grey-zone activities, including improved situational awareness, electronic warfare and information operations, and developing detailed planning for the provision of equipment, facilities and logistics to enhance Australian Defence Force (ADF) support to civil authorities.

Workforce Plans: The above complex capabilities require further growth in the workforce and the Government plans to implement an initial increase in ADF and Australian Public Service over the next four years and longer-term growth across the next two decades. By FY2023-24, the Government is aiming for growth of around 650 permanent people in the Navy Workforce, ~50 permanent people in Army Workforce, ~100 permanent people in Air Force Workforce and ~250 increase in Australian Public Service headcount.

Investment in Cyber Security: Towards the end of June, the Government announced the largest ever investment in cyber security, with $1.35 billion to be infused over the next decade to enhance the cyber security capabilities and assistance provided to Australians through the Australian Signals Directorate (ASD) and the Australian Cyber Security Centre. The investment was announced to fight back the rising malicious cyber activity by ensuring adequate availability of tools and capabilities. The package is a part of the Federal Government’s investment in cyber and information warfare capabilities under the Defence’s 2020 Force Structure Plan, discussed above.

Components of the Cyber Security Package: The first component involves an investment of over $31 million to enhance the ability of ASD to disrupt cybercrime offshore. Over $35 million will be invested in delivering a new cyber threat-sharing platform, enabling industry and government to share intelligence about the malicious cyber activity. An investment of over $12 million will be directed towards new strategic mitigations and active disruption options by blocking known malicious websites and computer viruses at speed. Over $118 million has been set aside for the expansion of ASD’s data science and intelligence capabilities, along with an investment of $62 million to deliver a national situational awareness capability, to better enable ASD to understand and respond to cyber threats on a national scale. Over $20 million will be used to establish research laboratories to better understand threats to emerging technology. The package also includes an investment of $470 million for the creation of 500 new jobs with ASD and expand the cyber security workforce.

The boost in defence spending has been proposed to safeguard national interests in a highly uncertain economic environment, with respect to the rising regional tensions and challenges in the post-COVID period. Recent India-China dispute over territorial claims across the Indo-Pacific region has compelled the Government to focus its efforts on the region and prepare for any potential adversities. Plans for increased spending in Defence and cyber-security have opened doors for businesses to avail of new growth opportunities. Let us have a look at few stocks which seem to be potential beneficiaries of the new packages announced by the Australian Government.

1. The Citadel Group Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 253.45 Million, Annual Dividend Yield: 3.35%)

Robust 1HFY20 Results: The Citadel Group Limited (ASX: CGL) is an enterprise software and services company that specialises in handling information in complex surroundings via people, integrating know-how, and systems to offer data and information anywhere and anytime. In 1HFY20 for the period ended 31 December 2019, the company reported total revenues of $61.1 million, up 24.4% year over year. The company’s shift in the business mix along with International expansion positively impacted performance. Notably in 1HFY20, total software revenues increased 18.9% year over year and came in at $18.9 million. During the period, the company successfully completed the acquisition of Wellbeing Software Group Limited to leverage several growth possibilities and alter its business into a global healthcare software company.

Outlook: For FY20, CGL expects revenues to be in the band of $128-$132 million and EBITDA to be between $28-$30 million. The successful integration of Noventus acquisition is expected to achieve over $20 million revenue in FY20, representing an increase of more than 11% on expectations. Further, post Wellbeing buyout, CGL expects to diversify its recurring revenue base, with recurring revenues increasing in the range of 41% to 48% of FY20 pro forma revenue. The company remains on track to invest in core Health and Enterprise Software and focus on developing secure cloud-based software solutions that have large addressable markets.

Citadel’s customer base predominantly comprises Health and Government clients on long-term contracts supporting business-critical software applications. The company has been on track to increase the size of SaaS business, gain multiple contract wins, and leverage a substantial pipeline of opportunities. The company has made an investment in developing the platform capabilities of the Citadel-IX offering, which increased the company’s customer engagement, positioning the Group with significant opportunities to scale. Moreover, the company also secured additional contracts in Defence and National Security in FY19. Notably, the company’s Citadel-IX offering has experienced a whopping 157% revenue growth in FY19 and will position Citadel for a consistent recurring revenue stream from a significantly larger and diverse client base. The Government has taken the necessary measures to invest ~ $1.35 billion over the next decade to enhance the cyber security capabilities and fight back the rising malicious cyber activity. With an increased focus on digital enablement and curbing the risk in all aspects of emerging technologies including cyber, data, AI, and cloud, the company may benefit from upcoming opportunities with regard to this major investment by the Government.

Key Risks: On the flip side, loss of any key contracts and key personnel, failure to commercialise R&D expenditure along with disruption through technological advances or product failures remain a potential headwind for the company..png)

Valuation Methodology: P/E Multiple Based Relative Valuation (Illustrative)

.png)

P/E Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

.png)

A-VIX vs CGL (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: In the last six months, the stock has corrected by 34.02% on ASX and is currently trading close to the average of its 52-week trading range of $1.205 - $5.920. After the market fallout, the stock of the company is now witnessing stable movements, supported by continued delivery on performance objectives. The company is focusing on making higher investments for product enhancements and new technological capabilities. CGL has implemented various contracts that will support revenue growth in the coming years and will drive the stock, going forward. We have valued the stock using the P/E multiple based illustrative relative valuation method and arrived at a target price of low double-digit upside (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $3.3, up 2.484% on 6th July 2020.

2. Quickstep Holdings Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 64.21 Million, Annual Dividend Yield: NA)

Q3 Results: Quickstep Holdings Limited (ASX: QHL) is an independent aerospace-grade advanced carbon fibre composite component manufacturer in Australia, operating from state-of-the-art aerospace manufacturing facilities in Geelong, Victoria. For the third quarter of FY20, the company reported sales of $19.2 million, which increased 16% year over year. Year-to-date sales went up 14% on pcp and came in at $57.7 million. During the quarter, the company reported operating cash flow of $0.1 million. The Company’s net bank debt at the end of the period stood at $6.6 million. The group held $3.1 million in cash and $0.7 million in restricted term deposits.

Outlook: Based on current operating conditions, the company predicts sales to grow more than 10% year over year in FY20, reflecting expected benefits from incremental orders on existing contracts. The company further expects FY21 revenue to be up 5-10%, with additional growth potential from flare housings and other bids in the pipeline. FY20 EBITDA is expected to be ~8 to 9% of sales on a like for like basis. In addition, the company expects to deliver positive NPAT and positive operating cash flow for FY20.

The company remains in a decent position despite the COVID-19 led uncertainty on its business operations within the Aerospace and Defence market. The company expects to enter FY21, with increased growth in its existing orders, on the back of continued strong performance on quality, delivery, and cost attractiveness. This depicts the company’s reputation as a highly dependable supplier in an increasingly stretched supply chain environment. Moreover, the company’s F-35 production ramp-up has continued according to plans and the company is running with full-rate production on the base contracts. Demand for the company’s C-130J has increased which will benefit both FY20 and FY21. In the coming 10 years, total Government funding to the Defence sector is expected to be ~$575 billion, which includes ~$270 billion invested in Defence capability to 2029-30. The company has a clear vision to increase revenue and diversify its customer base in the Aerospace and Defence sector, while expanding its abilities to grow the business globally in the Aerospace, Defence, and other advanced sectors.

Key Risks: The operating environment led by COVID-19 outbreak is unpredictable and dynamic. Further, failure to meet the working capital requirement, supply chain disruption and stiff competition are potential risks for the business..png)

Valuation Methodology: P/E Multiple Based Relative Valuation (Illustrative)

.png)

P/E Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

.png)

A-VIX vs QHL (Source: Refinitiv, Thomson Reuters)

Stocks Recommendation: In the last six months, the stock has corrected by 23.4% and gave a positive return of 32.35% in the last 3 months. The company remains well focused on supply chain performance, implementation of cost control measures, suspension of non-essential capital expenditure and maintaining health and safety of its employees and workers. As markets returned to stable grounds after the shockwave sent across by COVID-19, the stock of the company gained momentum and demonstrated rapid recovery, reflecting the strength of the business. The COVID-19 outbreak did not impact the company’s performance, with all its key customers continuing production in line with the plan. A strong pipeline of contracts and a diverse customer base will be the key catalysts driving the stock, going forward. We have valued the stock using the P/E multiple based illustrative relative valuation method and arrived at a target price of low double-digit upside (in percentage terms). Hence, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.1, up 11.111% on 6th July 2020.

3. Austal Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 1.19 Billion, Annual Dividend Yield: 1.8%)

FY20 Guidance Increased: Austal Limited (ASX: ASB) is engaged in the design, manufacture and support of high-performance vessels for commercial and defence customers worldwide. In a recent announcement, it was updated that Austal USA has delivered its 12th Independence-class Littoral Combat Ship (LCS) to the U.S. Navy, depicting its commitment and capability to deliver in a challenging operating environment. As per another recent update, the United States Government, Department of Defense, has announced a US$50 million Defense Production Act Title III Agreement (DPA Agreement) with Austal USA, to maintain, protect, and expand U.S. Domestic Production of steel shipbuilding capability and capacity through capital projects to begin in June 2020 and to be executed over the next 24 months. During 1HFY20, revenue of the company stood at $1.039 billion, up 22% on pcp. EBIT came in at $59.9 million, up 48% on pcp. NPAT for the period went up by 72% and came in at $40.8 million.

Outlook: The company increased its FY20 group revenue guidance to ~$2.0 billion and Group EBIT guidance to $125 million, as compared to $1.9 billion and $110 million announced earlier, reflecting the continued strong performance of the business, limited COVID-19 impact in April and May 2020, new contracts, etc. FY19 revenue and EBIT stood at $1.852 billion and $92.795 million, respectively.

In May 2020, Austal Australia was awarded a $324 million contract to design and construct six evolved Cape-class Patrol Boats (CCPBs) for the Royal Australian Navy. The new, evolved Capes provided added national security at this critical time during the COVID-19 pandemic. With the recent boost in Defence capability investment, the Government will seek contracts with trusted suppliers to promote national security amid the current economic disturbances. Austal Limited, with a strong foothold in the defence sector, remains a potential beneficiary of the above proposition.

Key Risks: Any adverse impact on US programs can impact the financial performance of the company. Moreover, the availability of US government funding may get affected due to budgetary or debt ceiling constraints. Changes in customer priorities or their ability to meet contractual requirements, additional costs, or schedule revisions represent other risk factors for the business..png)

Valuation Methodology: P/E Multiple Based Relative Valuation (Illustrative)

.png)

P/E Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

.png)

A-VIX vs ASB (Source: Refinitiv, Thomson Reuters)

Stocks Recommendation: In the last six months, the stock has corrected by 13.95% and gave a positive return of 17.25% in the last 3 months. As of 31st December 2019, the company had a strong balance sheet with a net cash position of $152.4 million. The FY20 guidance is underpinned by a strong customer base, with the majority of the company’s order book represented by defence vessel programs with the US Navy and Commonwealth of Australia (CoA). The recently secured contracts coupled with a revised FY20 guidance have driven remarkable movements in the stock as depicted in the chart above. Contribution from these contracts and further potential business opportunities will be the key catalysts, going forward. We have valued the stock using the P/E multiple based illustrative relative valuation method and arrived at a target price of low double-digit upside (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $3.33 on 6th July 2020.

4. Electro Optic Systems Holdings Limited (Recommendation: Hold, Potential Upside: Low Double-Digit)

(M-cap: A$ 790.39 Million, Annual Dividend Yield: NA)

Contract negotiations with the Commonwealth of Australia: Electro Optic Systems Holdings Limited (ASX: EOS) is primarily engaged in space, defence systems and communications business activities. During FY19, the company reported revenue from ordinary activities amounting to $165.98 million, as compared to prior year revenue of $87.13 million. During the year, an increase in production plant utilisation to beyond 50% of capacity in the EOS Defence sector, drove a three‑fold increase in overall sector EBIT from $7.4 million to $22.3 million.

Outlook: Due to COVID-19, there have been delays in the range of 3-6 months for some H2 2020 tender opportunities. Delivery issues have resulted in delays of 6 months to $100 million of cash flow receipts. $70 million of the revenue has been deferred to 2021. The deferral of a substantial amount of activity and its associated revenue from 2020 to 2021 led to a reduction in expected growth from 70% to 25% over 2019 performance.

As per a recent announcement, the company has entered into contract negotiations with the Commonwealth of Australia for the acquisition of 251 Remote Weapon Stations and related material, which forms part of the $270 billion capability upgrade for the Australian Defence Force, under the new 2020 Force Structure Plan. The execution of the agreement with the Commonwealth of Australia is subject to negotiation and may include certain conditions. The above agreement marks the beginning of benefits to be derived out the Government’s Defence capability investment plans. Moreover, the increased investment may further offer growth opportunities in the years to come.

Key Risks: If the emerging macro‑economic risk pertaining to COVID-19 continues for a prolonged period, the company might witness adverse financial impacts, including slower revenue growth and obstruction to the plan towards increased profitability. Further, the company is exposed to market interest rates risk primarily due to its cash holdings. Moreover, any default on contractual obligations by the counterparty exposes the business to credit risk..png)

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

.png)

EV/Sales Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

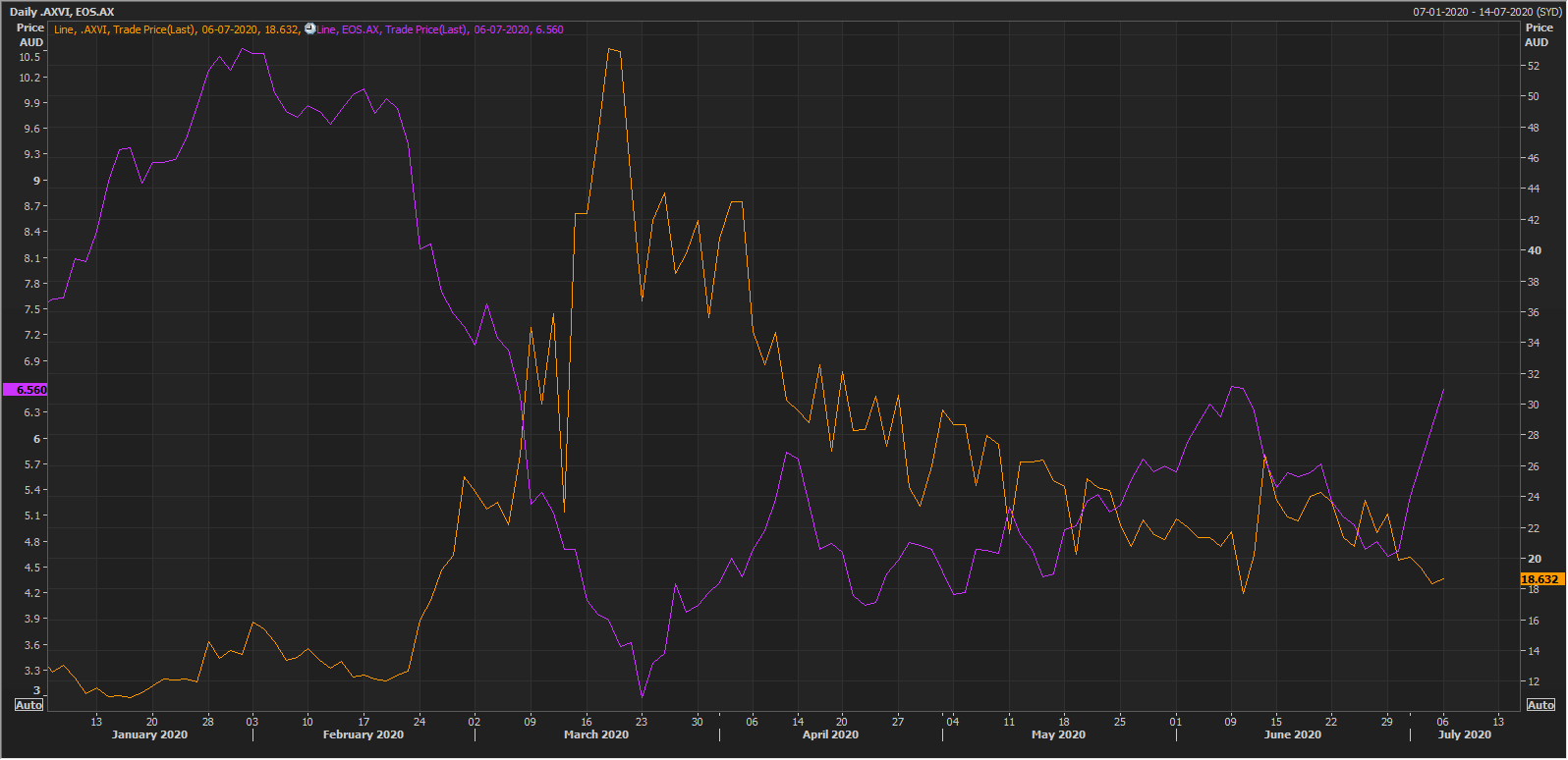

A-VIX vs EOS (Source: Refinitiv, Thomson Reuters)

Stocks Recommendation: In the last six months, the stock has corrected by 29.07% and gave a positive return of 23.15% in the last 3 months. The stock of the company has increased sharply due to the ongoing contract negotiations with regard to the Government’s new 2020 Force Structure Plan. Despite the impact of COVID-19 and subsequent revision to FY20 growth guidance, the recent developments reassure us about the company’s capabilities to drive further growth in the business. We have valued the stock using the EV/Sales multiple based illustrative relative valuation method, and arrived at a target price of low double-digit upside (in percentage terms). Hence, we give a “Hold” recommendation on the stock at the current market price of $6.56, up 23.308% on 6th July 2020.

(2).PNG)

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...