Kalkine has a fully transformed New Avatar.

I. Sector Landscape and Outlook

Transport sector is the lifeline of an economy. The entire supply chain, commercial freight and personal movement depend on road transport, rail, aviation, and marine. The sector also showcases a range of operators – airline companies, air freight companies, logistic companies, trucking, tour and travel service providers, toll operators, shipping companies. The earnings of these operators get influenced by many factors, such as oil prices, debt, regulations, etc.

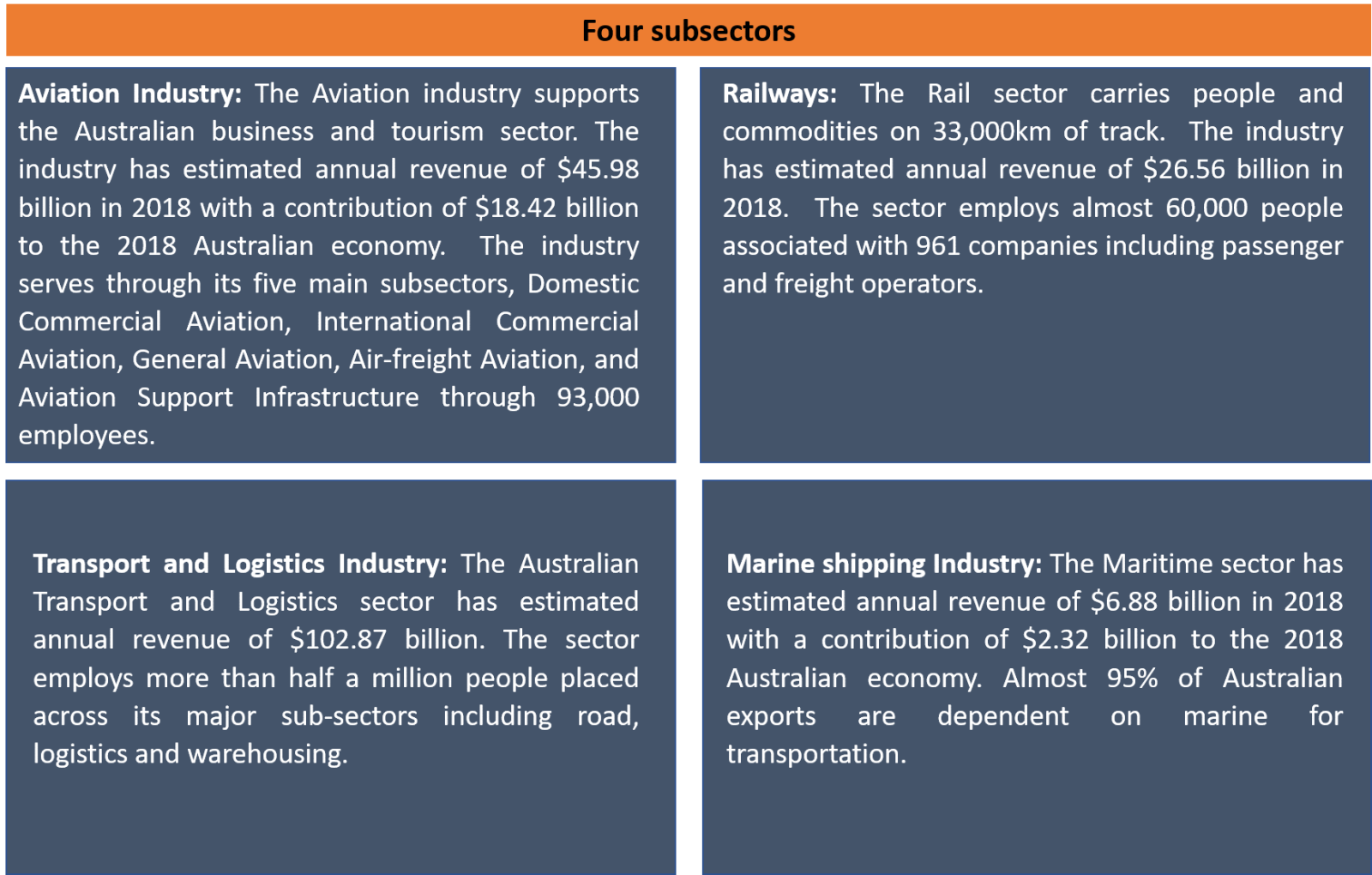

Fig 1: Four subsectors within transport sector

Source: Kalkine Secondary Research

The pandemic has stalled businesses of many subsectors except domestic road transport or domestic freight movement necessary to meet the country’s supply chain demand. However, COVID-19 restrictions easing from April have pushed industry operators to commence limited activities.

In light of that, in this sector report, we have exhaustively examined the dynamics that influence the earnings and competition and analyse the performance of the companies operating within the industry.

Understanding key factors that affect the transport sector

With social distancing in place and lockdown imposed nationwide, meeting the supply chain requirements has become a big hassle. To operate in optimum at such a challenging environment is a humongous task for the transport operators. Deemed as essential businesses, the transport sector is also experiencing a labour shortage, creating hindrance in day-to-day operations. With industry experts across anticipating recession, the world economy is yet to pick up pace in its way to recovery. Let’s see how the various factors affect the earnings of the transport industry.

Oil price

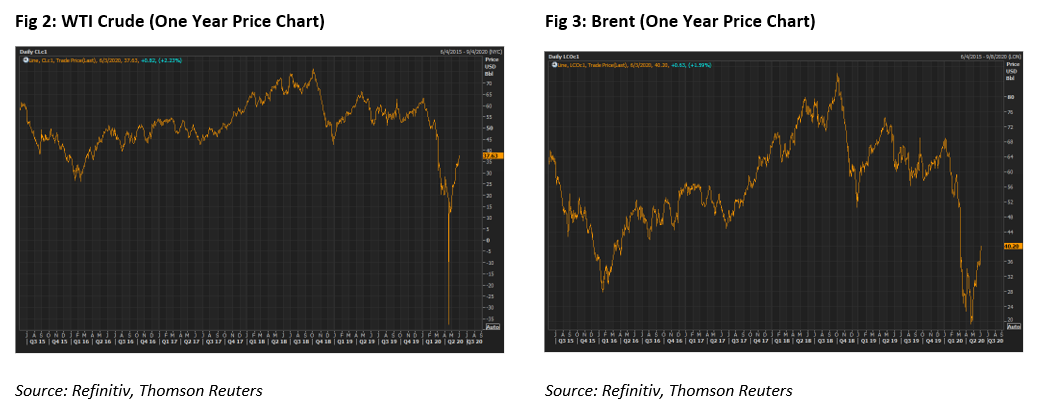

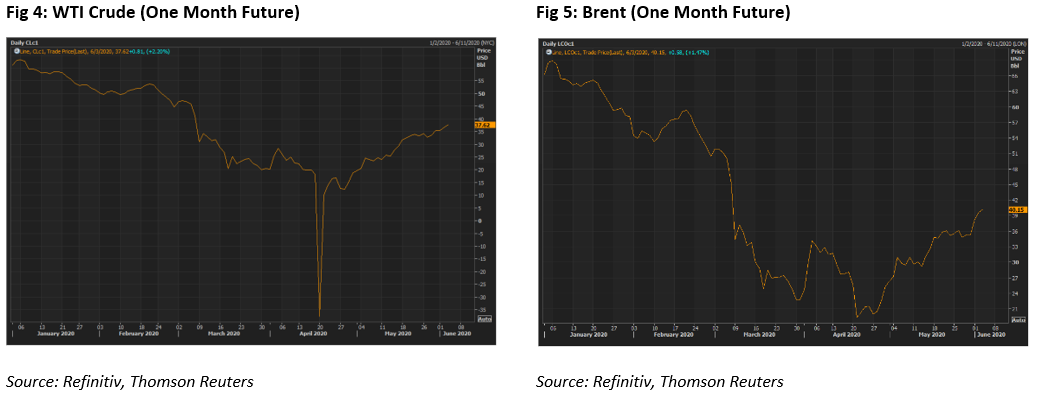

Oil prices impact Transportation companies heavily. Fluctuations in the oil price affect the earnings of the companies and prompt them to be more fuel efficient. All operators, whether airlines or road transport service providers such as trucking companies or logistics companies are depended on fuel to run their business. Higher the price, less will be the profit margin. The COVID-19 pandemic had a profound impact on the crude oil prices with both WTI Crude and Brent experiencing a setback in the month of April and oil prices have staged a recovery in May, 2020.

However, given the abysmal state of the economy, a recovering oil-price indicates recovery of the economy as well, which will create demand for transportation services.

Capital investment

The transportation companies not only have to invest heavily to acquire heavy duty or light commercial vehicles but in maintenance costs as well. Airlines spend millions for the acquisition of planes and in their maintenance as well. These financial costs lead to a considerable amount of long-term debt on a company’s balance sheet.

Regulations

The transportation industry is subjected to regulations as it carries business risk and individual risk. Regulation on license, training and certifications requirement affects driver supplies.Shortage of drivers increases the cost of acquisition of drivers and also affects operations, impacting business performance.

Now that we know about factors affecting the transport sector, let us ponder on the demand dynamics in the transport sector.

Understanding the transport sector demand dynamics

Transport demand occurs when there is a need for a transport-based service for which the user is willing and able to pay a fare for availing the transport service. Stronger an economy, stronger will be its agriculture and manufacturing sector which will create demand in the tertiary sector and consequently demand for transport services. Let us understand the industry.

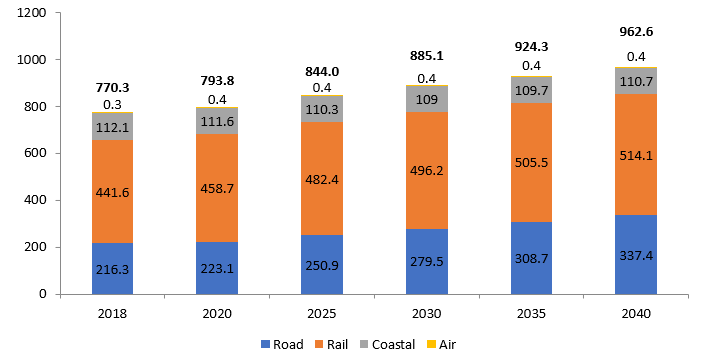

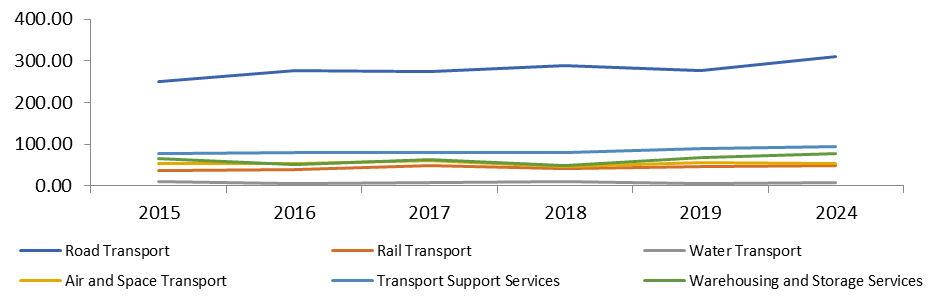

Freight forecasts by transport mode

According to the Bureau of Infrastructure, Transport and Regional Economics (BITRE), total domestic freight volumes are projected to grow by approximately 25% between 2018 and 2040, which is significantly slower than historical rates of growth— largely as a result of slower future expected commodity export growth and slightly slower domestic economic growth.

Fig 6: Projected future freight task, by major transport mode, 2018–2040, billion tonne

Source: BITRE

According to BITRE,

- Road freight volumes are estimated to increase by 56% from 2018 to reach 337 billion tonne kilometres by 2040. If the growth rate is below average, then road freight is expected to reach 310 billion tonne kilometres. The demand for road freight will be driven by the construction and retail industry growth prospects, whose businesses are highly dependent on road freight services.

- Rail freight volumes are expected to touch 515 billion tonne kilometres in 2040, estimating a growth rate of ~16.4% from 2018 to 2040. In case of below average growth rate, rail freight volumes are expected to hit 465 billion tonne kilometres. The demand for rail freight will depend on the growth of major export commodities and specific markets such as agricultural and energy and resources.

- Domestic coastal shipping volumes are expected to hit around 109 billion tonne kilometres in 2040. If the growth rate is below average, total coastal shipping freight volumes is expected at less than 78 billion tonne kilometres. The demand for coastal freight also depends upon major export commodities and specific markets such as agricultural and energy and resources commodities

- Airfreight volumes are expected to grow by around 17% to around 393 million tonne kilometres in 2040 from ~337 million tonne kilometres in 2018. Passenger aircrafts carry Australia’s domestic air freight which mostly carries low-density freight including mail, parcels and high value items.

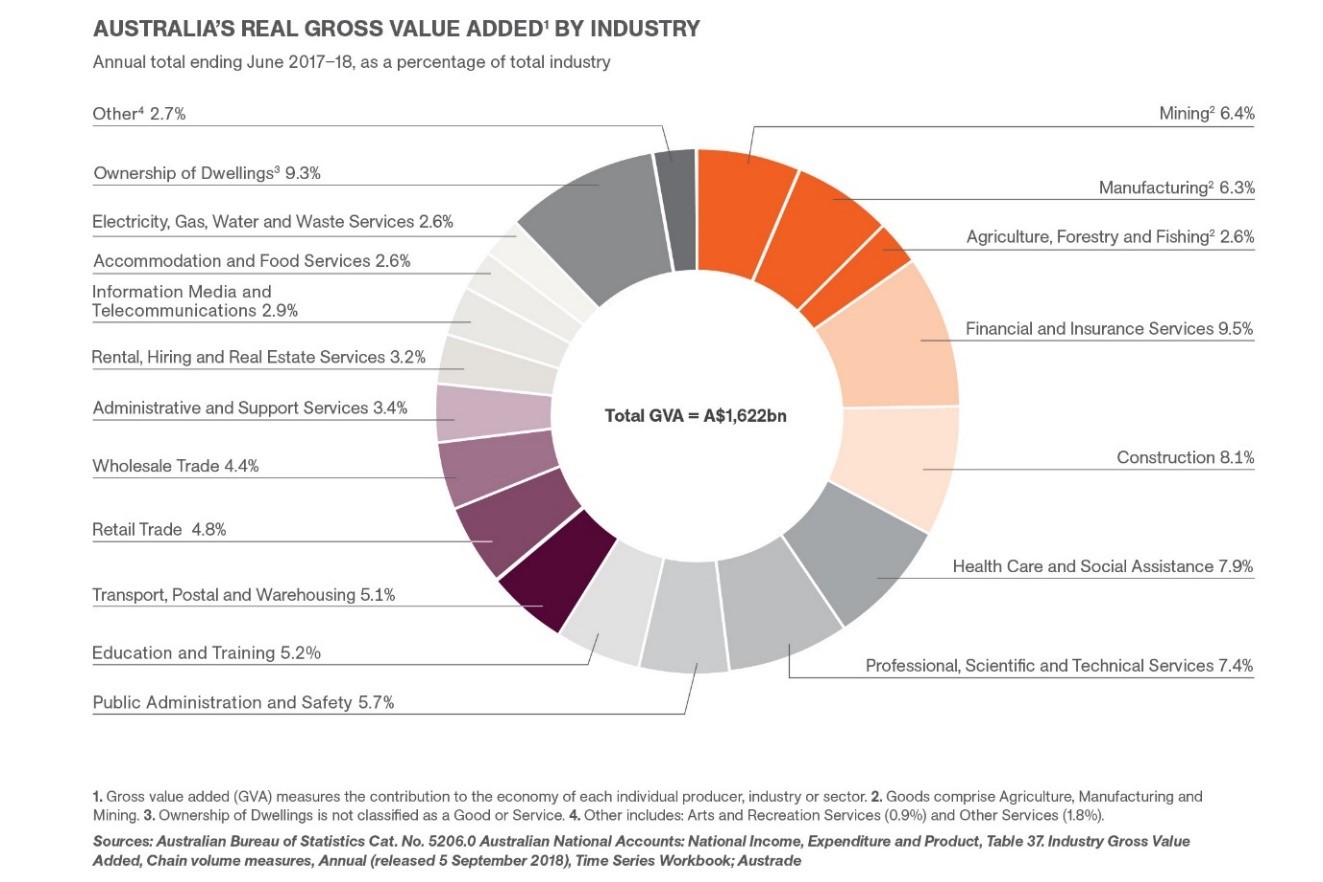

According to Australian Trade and Investment Commission, the transportation sector along with postal and warehouse, contributed 5.1% to the Australian gross value asset ending June 2017-18. The Australian economy is expected to record a contraction in GDP of around 10% over the first half of 2020. Australia intends to invest in many road and rail related projects to boost the Australian economy.

Fig 7: Australia’s Gross Value Added By Industry

Source: Australian Trade and Investment Commission

Now, that we understand about the demand dynamics in the industry, let’s look at the supply side scenario.

Understanding transport sector Supply dynamics

Labor Availability

A booming economy creates more jobs and boosts the service operators’ business. Road Transport employs maximum people with Water Transport being the smallest.

Fig 8: Employment level and projection (‘000s)

Source: National Industry Insights

The Australian transport industry is already experiencing a truck driver shortage. The pandemic has created an additional challenge affecting the transport industry significantly. Various companies are experiencing decreased demand in services citing COVID-19 restrictions or business closures as a reason.

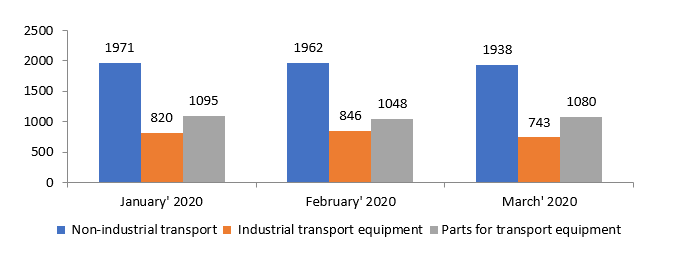

Availability of transport infrastructure

Despite the COVID-19 outbreak, Transport Equipment import remained consistent with minimal impact

Fig 9: Transport Equipment Imports During Pandemic

Source: ABS

Having understood the demand and supply conditions, let us have a look at the current risk factors ailing the Transport sector.

Understanding the effect of the pandemic on the transport subsectors

The Aviation Sector

The effect of the pandemic has been felt across the sectors. With international borders closed and domestic flights on hold, the aviation industry is severely impacted with no passenger traffic or air-freight. Costs such as maintaining workforce also add to the burden. Many are strengthening their balance sheet by acquiring additional debt. Sydney Airport Limited received an additional bank debt facility of $850 million while Qantas Airways Limited secured a debt funding of $550 million to meet up the loss as the airline extended flight cancellations through to the end of July. During the pandemic, flight departures and arrivals reduced significantly

- In March 2020, overseas visitor arrivals to Australia for short-term trips decreased 51.9% since February to 307,900 trips. Australian resident returns from overseas decreased 23.3% since the previous month to 706,200 trips.

- In April 2020, out of 21,600 estimated trips, 15,100 were Australian citizens, a decrease of 98.7% compared to the same month last year.

With COVID-19 restrictions being lifted progressively from April, the aviation sector is witnessing a rise in the number of domestic flights operating. Currently, air-travel is limited within few cities though. Qantas is operating between capital cities and to 36 regional destinations until the end of June 2020.

Road Transport Sector

During pandemic, the road transport operators are running on reduced capacity which is increasing operational costs and proving detrimental for the business. NatRoad, has appealed for government support to take action regarding reducing operating costs for road transport industry members.

Toll Operators

The business of toll operators depends upon the rise and fall of the transport sector. As inter borders are sealed by various states, the general public movement has stalled. The toll collectors’ primary source of revenue earning has become limited to trucking companies delivering essential commodities. With Australia opening up its economy by phases, road transportations are also witnessing an uptick with toll operators commencing their business. For example, Transurban Group has commenced toll activities at various federal highways

Logistics Industry

The business of Logistics the industry depends upon the rise and fall of the retail sector and home-delivery market. With social distancing, the industry is facing labour shortage with respect to the delivery man and other operational issues. The shortage of drivers is also prompting retailers to embrace driverless trucks and drones for delivery. For example, retailers such as Wokitup! and Sushi Hub and others from Canberra and Logan are using the services of Wing, a subsidiary of Google’s parent company Alphabet, Google through his subsidiary Wing, is making deliveries for businesses.

Shipping Industry

IMO (International Maritime Organization) 2020 regulation that came into effect this year, levies an extra component to the freight rate called Low Sulphur Surcharge, upon using cleaner fuel on ships. The surcharge will escalate cost by $15 billion for the worldwide shipping industry.

Railway industry

Agricultural commodities and energy and resources depend heavily on railways for the transportation of goods. As the Agricultural commodities fall under the essential commodities section, demand for rail freight will continue to persist. A reduction in demand for mining and energy related commodities, however, may put a damper on the volume of railway freight and eat away profits.

Domestic freight across all transport modes are expected to pick up pace as the Australian economy moves out of COVID-19 effect gradually. Once Australia opens its international borders, a surge in passenger movement and international airfreight is also expected. In view of the growth in the subsectors, the outlook of the transportation sector looks bullish in the medium to long term.

II. Investment Theme and Stocks under Discussion (AZJ, ALX, QUB and TCL)

After gauging through the transport industry market dynamics, let us take a detailed look at the companies operating in this sector, in terms of their performance and outlook. We have assessed the companies’ stocks based on Discounted Cash Flow (DCF) method or Price to CashFlow.

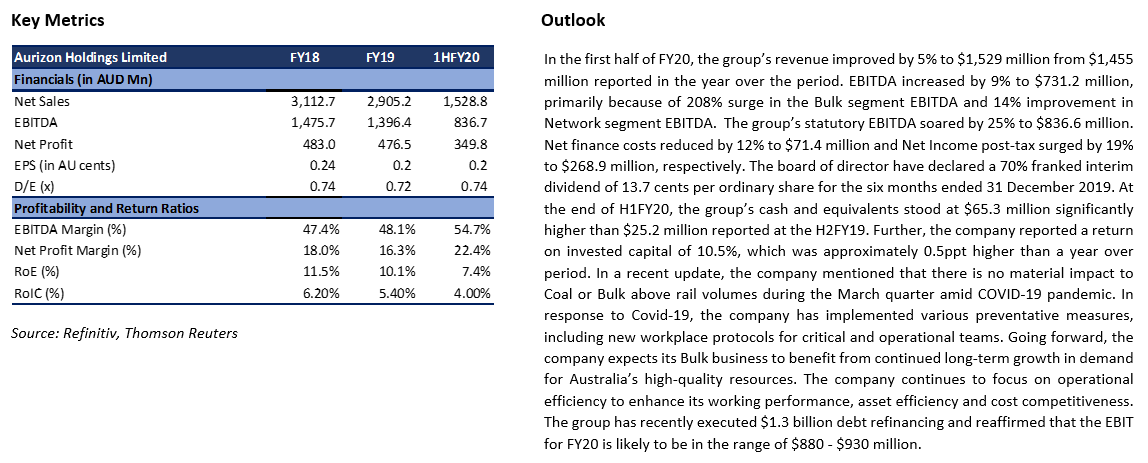

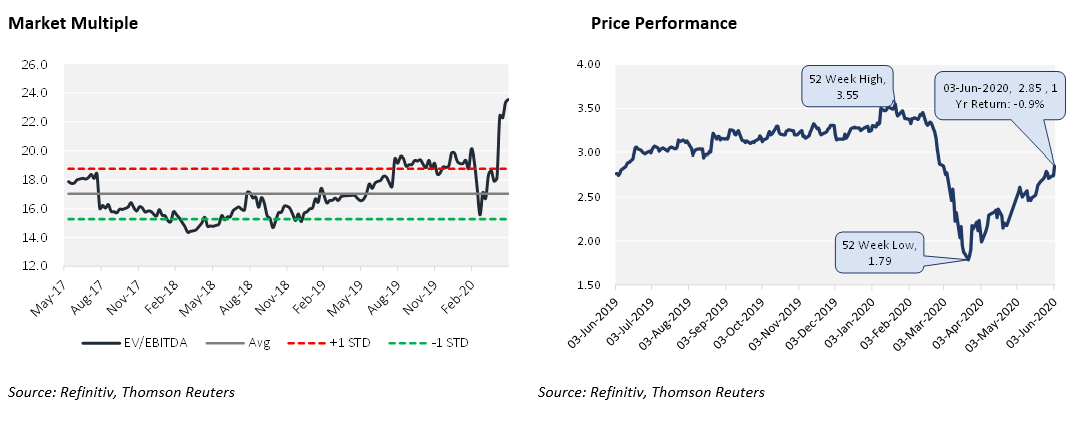

1. ASX: AZJ (AURIZON HOLDINGS LIMITED)

(Recommendation: Buy, Potential Upside: Low Double Digit, Mcap: AUD 9.39 Billion)

Aurizon Holdings Limited is an Australia based company that operates a rail-based transport business. The group operates through three segments, namely coal, bulk and network.

Valuation

Our illustrative valuation model suggests that stock has a potential upside of ~17% on 3 June 2020 closing price. At the same market price, the stock is offering a dividend yield of ~6%.

.png)

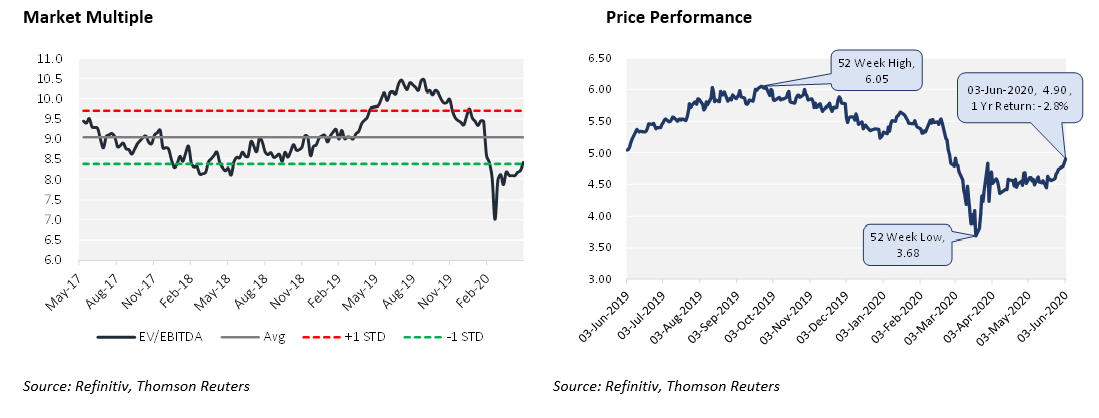

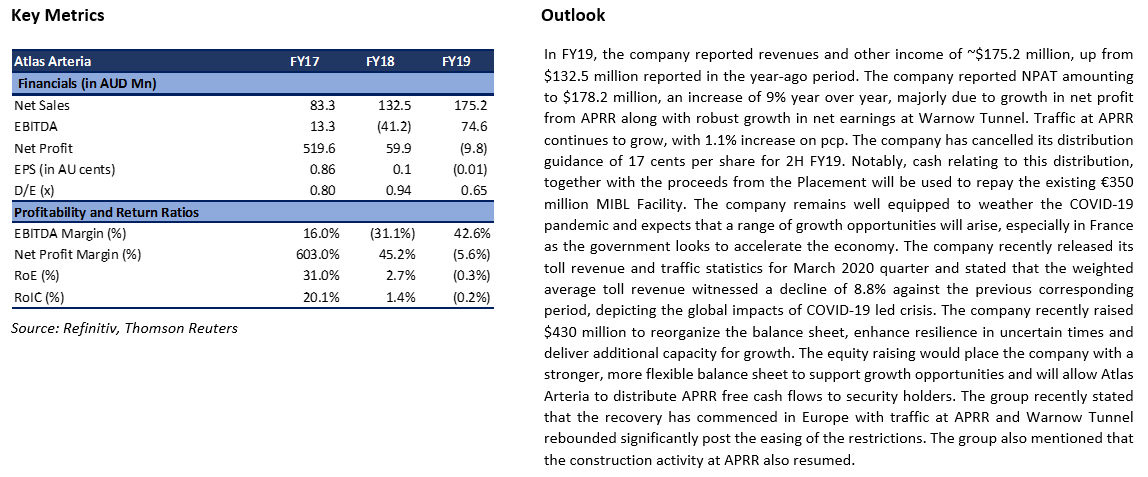

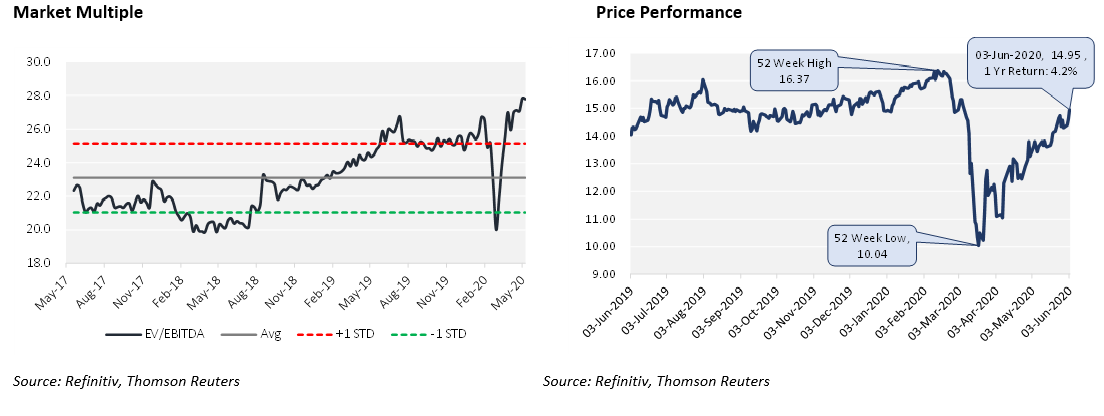

2. ASX: ALX (ATLAS ARTERIA LIMITED)

(Recommendation: Buy, Potential Upside: Low Double Digit, Mcap: AUD 6.48 Billion)

Atlas Arteria is involved in managing and controlling a portfolio of toll road assets.

Valuation

The group witnessed a decline in traffic owing to travel restriction imposed by the government. The group recently stated that recovery has commenced in Europe with traffic at APRR and Warnow Tunnel rebounded significantly post the easing of the restrictions. The group has recently raised capital in terms of equity offering amounting to $430 million, which is likely to reorganise its balance sheet. The group has a decent liquidity position of EUR 3.2 billion which seems sufficient to meet the near to medium term requirement, which includes the repayment of debt (EUR 1.8 Billion) in the next two years. We have valued the group by using P/CF methodology, and for this purpose, we have considered Transurban Group (ASX: TCL), Qube Holdings Ltd (TSX: QUB) and Sydney Airport Holdings Pty Ltd (TSX: SYD) etc. as a peer group. Our illustrative valuation model suggests that the stock has a potential upside of ~17% on 3 June 2020 closing price. At the same market price, the stock is offering a dividend yield of ~2.2%.

.png)

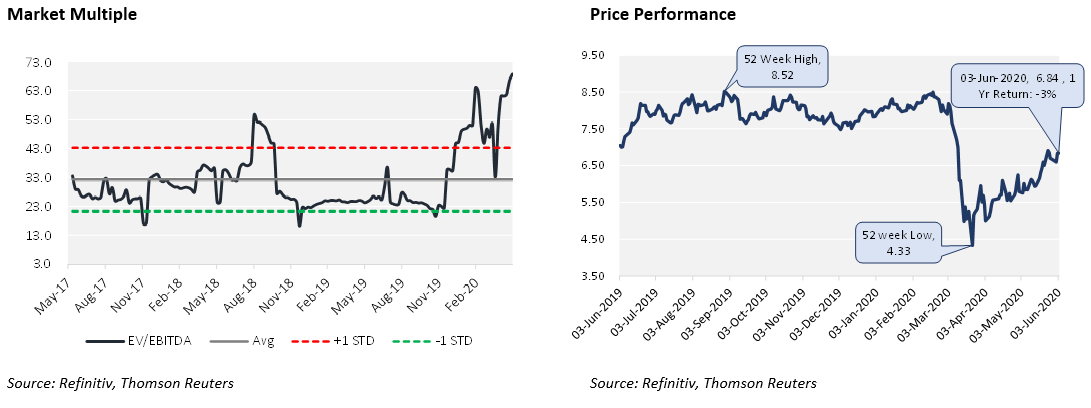

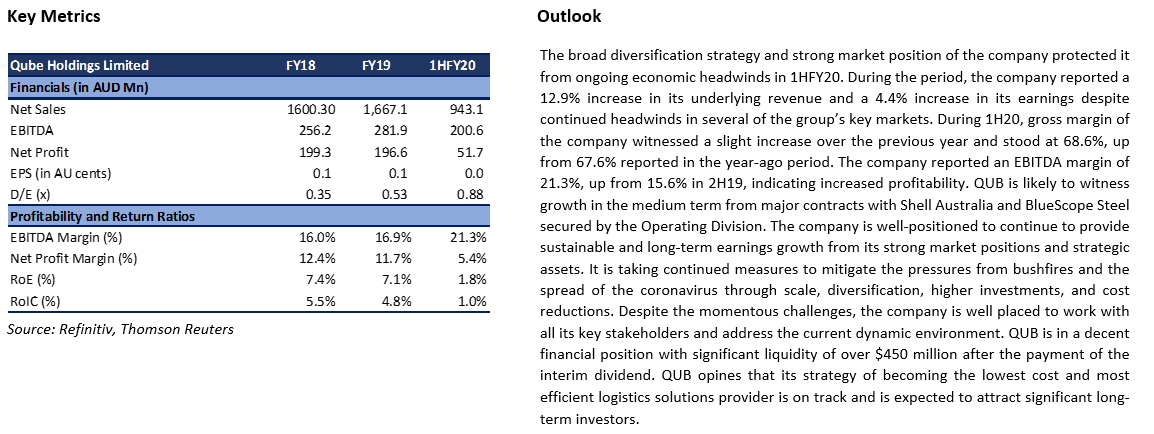

3. ASX: QUB (QUBE HOLDINGS LIMITED)

(Recommendation: Buy, Potential Upside: Low Double Digit, Mcap: AUD 5.37 Billion)

Qube Holdings Limited is engaged in providing complete logistics solutions across multiple aspects of the import-export supply chain.

Valuation

Our illustrative valuation model suggests that stock has a potential upside of ~18% on 3 June 2020 closing price. At the same market price, the group is offering a dividend yield of ~2.9%..png)

4. ASX: TCL (TRANSURBAN GROUP)

(Recommendation: Hold, Potential Upside: High Single Digit, Mcap: AUD 40.89 Billion)

Transurban Group is engaged in owning, operating, and developing electronic toll roads and intelligent transport systems..png)

Valuation

Our illustrative valuation model suggests that stock has a potential upside of ~8% on 3 June 2020 closing price. At the same market price, the group is offering a dividend yield of ~4.2%..png)

Note: All the recommendations and the calculations are based on the closing price of 3 June 2020. The financial information has been retrieved from the respective company’s website and Thomson Reuters. All the recommendations are valid on 4 June 2020 price as well.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...