Company Overview - Australia and New Zealand Banking Group Limited (ANZ) provides a range of banking and financial products and services to retail, small business, corporate and institutional clients. The Company conducts its operations in Australia, New Zealand and the Asia Pacific region. The Company has 1,220 branches and other points of representation excluding Automatic Teller Machines (ATMs). The Company operates on a divisional structure with Australia, International and Institutional Banking (IIB), New Zealand and Global Wealth. ANZ’s business consists of raising funds through customer deposits and the wholesale debt markets and lending those funds to customers. ANZ also operates in other countries, including the United Kingdom and the United States.

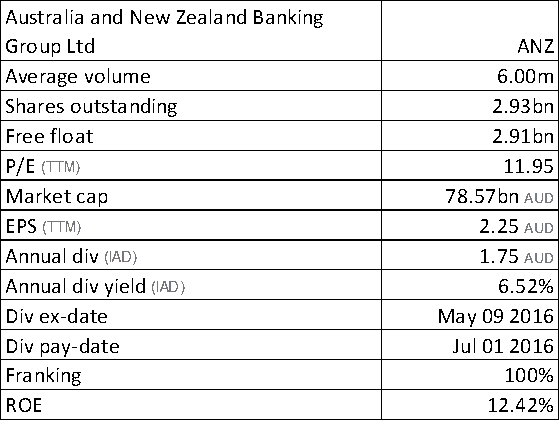

ANZ Details

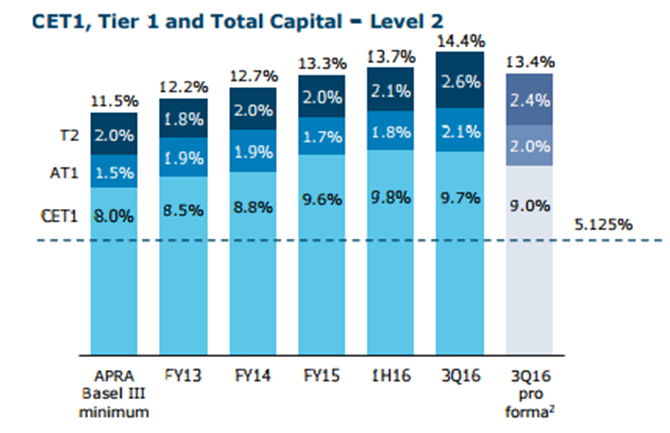

Boosting capital position to comply with APRA requirements: Australia and New Zealand Banking Group Ltd (ASX: ANZ) has allocated $1.3 billion under ANZ Capital Notes 4 Bookbuild and the Margin is set at 4.7% per annum. For this, ANZ has lodged the replacement prospectus. ANZ would use these proceeds to refinance CPS2 and for general corporate purposes. APRA has confirmed that the Notes will constitute an additional Tier 1 Capital for the purposes of ANZ’s regulatory capital requirements. Meanwhile, the CET1 Ratios for both the ANZ Level 1 Group and the ANZ Level 2 Group was 9.7% as on June 30, 2016 (including 2016 interim dividend).

ANZ Capital Position (Source: Company Reports)

ANZ intends to keep the payout ratio in the range of 60-65% over time while aiming an operating range for the CET1 Ratio around 9.0% during normal conditions. Moreover, on a pro forma basis, based on a credit risk weighting at the mid-point of the 25%-30% range recommended by the FSI, the ANZ Level 2 Group’s CET1 ratio would be over 9.0%. A further 1% increase or decrease to the credit risk weighting from the mid-point would have an impact on the ANZ Level 2 Group’s CET1 of approximate 0.06% that is around $250m.

Meanwhile, ANZ overall provision charge was $1.4 billion as of third quarter of 2016 which has individual provisions of $1.34 billion and a collective provision of $60 million. The third quarter individual provision charge was on track with the average of the first half.

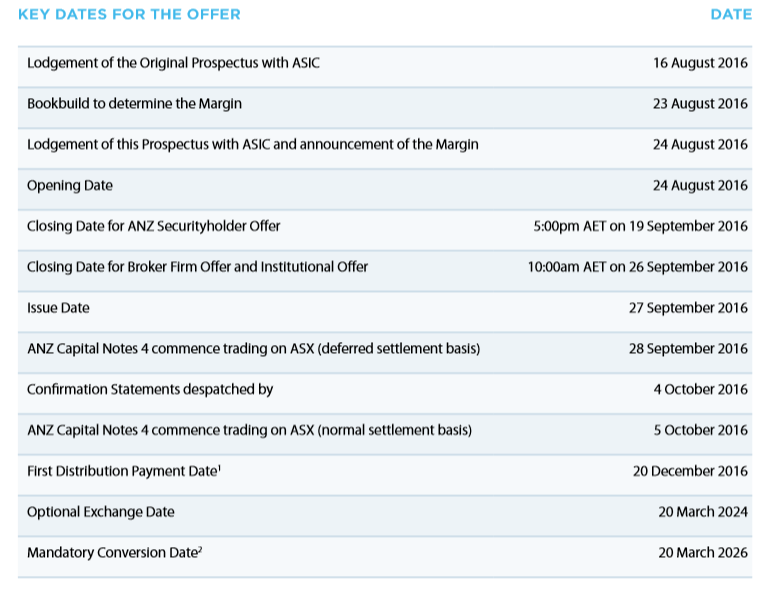

Offer Dates (Source: Company Reports)

Third Quarter 2016 Trading Update:As per the third quarter 2016, ANZ’s statutory net profit reached $4.3 billion, while cash profit reached $5.2 billion on an adjusted pro forma basis. The group's NIM was stable as the portfolio rebalancing in institutional has offset the increased funding costs and asset pricing competition. Management clearly stated that they are undertaking efforts to survive on a long term basis despite facing some short term pressures. Meanwhile, the bank continues to focus on the cost control, Asian business, as well as enhance the productivity of the bank by adopting new technology and digitizing the processes. However, the rising bad debts is still a concern due to which the profit adjusted for one off items mainly related to accounting timing differences fell 3% to $5.2 billion for the nine-month period ending June 30

th 2016. On the other hand, ANZ’s retail businesses in both Australia and New Zealand performed well and the third quarter individual provision charge was in line with the average of the first half. For the third quarter, markets income increased 14% over 2Q16 to $505 million, which has been in line with the quarterly average over the previous four quarters of $509 million.

This reflects an encouraging trend for revenue attrition tracking better relating to markets business. Global Markets income reached $1.5 billion, wherein 90% was from Customer Sales flows.

Adjusting risk appetite: ANZ is rebalancing the businesses with the focus on the Australian and New Zealand home owners and small businesses, and for the institutional clients driven by trade and capital flows between Australia, New Zealand and Asia. Moreover, ANZ is cutting risks by exiting low return and non-core businesses, as well as decreasing reliance on low-returning aspects of institutional banking while reducing the product and management complexity. Accordingly, the bank exited the low return Institutional lending assets while finished the sale of the Esanda Dealer Finance business and Wealth Oasis platform. Meanwhile, the bank continued to rebalance the Institutional business by further cutting the reductions in lower yielding assets coupled with ongoing business restructuring. The bank’s efforts of enhancing the quality of Risk Weighted Assets (RWA) has generated a $15 billion decrease in Credit Risk Weighted Assets (CRWA) on a constant currency basis. The group reported that they witnessed the similar momentum in this year to date with over a third of that total reduction in CRWA occurring in the third quarter of 2016. On the other hand, the divisional revenue fell by a lower percentage as compared to the reduction in RWAs. During the period end, the cost growth was in the low single digits as the group’s productivity initiatives have started generating benefits. The rebalancing of the business led a positive impact on its Division’s margins by over 5 bps (excluding Global Markets). However, Global Markets margins lost 5 basis points. Overall, the bank is said to have already completed A$30 billion out of a potential A$50 billion RWA run-off in the Institutional portfolio. It has been noted that the revenue decline from the above effort has been modest and the exposures were ‘low-yielding’ ones.

Market experts estimate about A$100 million of revenue headwinds for FY17 for ongoing run-off and the same is expected to deliver 2% overall revenue growth. There are also possibilities to lower the operating costs given the A$2.8 billion cost base of the institutional bank and corresponding 50% cost to income ratio. Once the bank completes capital re-allocation, there may be about 5% to 10% earnings upside. The bank thus appears to be in a better position to grow earnings.

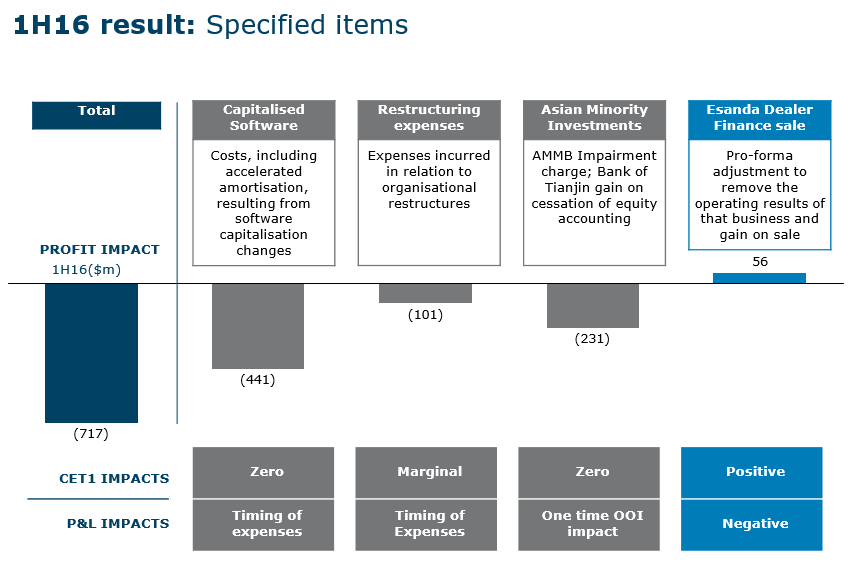

1H16 Result for Specified Items (Source: Company Reports)

Change in Moody’s outlook: ANZ has confirmed Moody’s decision to revise Australia’s macro profile which has led to a change in the outlook for the major Australian banks, including ANZ, from stable to negative.

Therefore, Moody’s has reaffirmed ANZ’s rating moving from Aa2 (Outlook Stable) to Aa2 (Outlook Negative) as the firm expects a more challenging operating environment for the banks for the remainder of 2016 and beyond. However, the ratings outlook change has not impacted Moody’s rating of ANZ’s baseline credit or the counterparty risk assessment.

Stock Performance:ANZ stock started recovering by 8.4% in the last three months (as of September 02, 2016), as the bank is making solid efforts to withstand the tough market conditions in Australia. The bank is one of the banks against which US class action complaint has been lodged regarding bank bill swap rate and ANZ is set to defend the same. On the other hand, the Retail businesses of the bank in Australia as well as New Zealand have performed well. Retail experienced modest asset growth and margin pressure in a competitive market for mortgages and deposits. Small Business Banking remains an area of good growth in both markets, even though conditions in Corporate and Business Banking remained highly competitive. Moreover, ANZ is establishing a dedicated Digital Banking Division to support the growth in priority areas and starting a strategic review of the Wealth, Asia Retail and NZ Asset Finance businesses, which may result in either the restructure or sale of some or all of these businesses. ANZ is also repositioning the minority investments in Asia as Group assets, and possibly exiting some of the non performing or less potential investments over time. On the other side, ANZ is exploring the strategic options for ANZ share investments and reviewing other assets in the portfolio. Overall, ANZ’s outlook statement does suggest a more challenging environment for revenue growth and BDD charges that can approach the through-the-cycle range of 25-30bp; nonetheless, the better capital and provision buffers, efforts on cost reduction, efforts on rebalancing lower return portfolios, and so forth appear to make the bank better placed than its peers to sail through the difficult time.

ANZ stock is having a good dividend yield and is trading at a low P/E. We believe long term investors could leverage the subdued levels of the bank as an entry opportunity. Based on the foregoing, we give a “Buy” recommendation on the stock at the current price of $27.25

ANZ Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...