Company Overview - Australia and New Zealand Banking Group Limited (ANZ) provides a range of banking and financial products and services to retail, small business, corporate and institutional clients. The Company conducts its operations in Australia, New Zealand and the Asia Pacific region. The Company has 1,220 branches and other points of representation excluding Automatic Teller Machines (ATMs). The Company operates on a divisional structure with Australia, International and Institutional Banking (IIB), New Zealand and Global Wealth. ANZ’s business consists of raising funds through customer deposits and the wholesale debt markets and lending those funds to customers. ANZ also operates in other countries, including the United Kingdom and the United States.

.png)

ANZ Dividend Details

Delivered a decent first quarter performance in spite of ongoing tough market conditions: Australia and New Zealand Banking Group (ASX: ANZ) reported a reasonable first quarter of 2016 performance and generated a cash profit rise of 5% to $1.85 billion as compared to the average of the third and fourth quarters of fiscal year of 2015 and an increase by 4% against the prior corresponding period (pcp). The statutory net profit reached $1.6 billion during the period. Management reported that their income improved better than the expenses, while the group had offset the rising technology investments and wage inflations by decreasing the staff number by 2.5%. The bank’s Net Interest Margin (NIM) remained more or less steady, with a decline by 2 basis points with the markets impact. But ANZ delivered a strong Retail and Commercial business in Australia and New Zealand driven by ongoing market share gains of the bank at home lending across major markets. Small business performance also enhanced in both the Australian as well New Zealand regions during the quarter. But Corporate Banking income performance was not as per expectations due to rising funding costs as well as competition. Even the steady Life Insurance lapse rates contribution to the wealth business was offset by the ongoing global as well as domestic market turmoil. As per the Institutional segments performance during the quarter, markets income improved by 6% year on year to $553 million while customer sales accounted over 56% of the total markets income which was in line as compared to the average of the second half of 2015 and fiscal year of 2015.

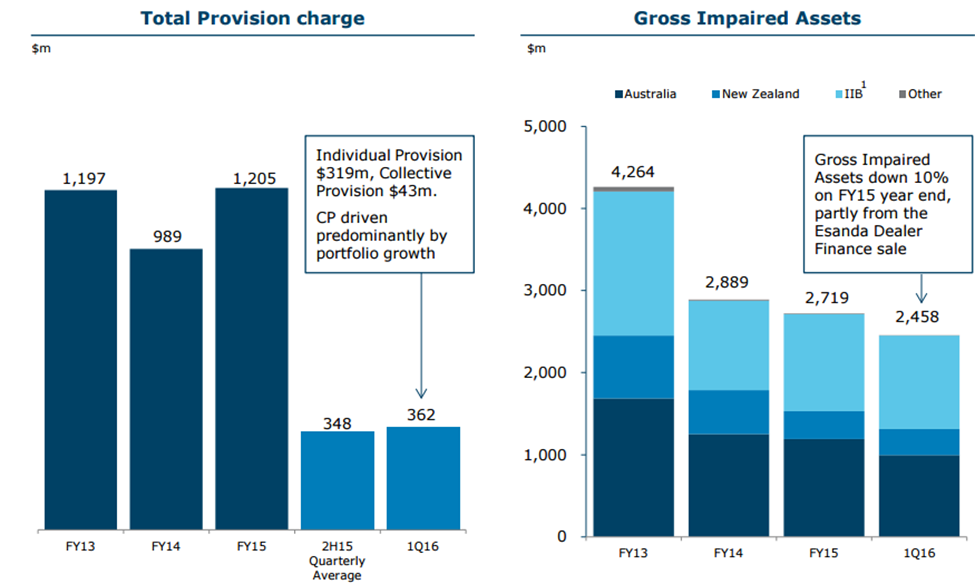

ANZ decreased its lower returning assets in Trade and Lending which contributed to its cash management performance. Moreover, a better Institutional net interest margins indicates the group efforts to enhance its asset mix and deposit pricing. But, the bank’s overall provision charge for the first quarter of 2016 reached $362 million while individual provisions were $319 million and the bank reported collective provisions of $43 million during the same period.

.png)

First quarter of 2016 performance (Source: Company Reports)

Improving credit quality: Australia and New Zealand Banking Group is enhancing its credit quality and accordingly decreased its Gross Impaired Assets by 10% in the first quarter of 2016 as compared to fiscal year of 2015 end, due to contribution from the Esanda Dealer Finance sale. The overall Credit Risk Weighted Assets (CRWA) as of December 2015 reached $344.1 billion, which is a decline by $5.7 billion of 1.6% as compared to the September 2015. This decrease in CRWA includes a $2.3 billion decrease from the foreign currency fluctuations and decrease in IRB. On the other hand, this decrease was partially offset by portfolio growth in Australia and New Zealand business contributed from the Internal Rating Based (IRB) Residential Mortgage as well as a revised risk treatment implemented from the Specialized Lending asset class leading to a rise in the Specialized Lending RWA. Meanwhile, ANZ Traded Market Risk RWA fell by 14% during the period due to improved diversification in the trading book coupled with a decrease in general market risk held over the quarter. But, the Operational Risk RWA was maintained in line with September 2015 levels indicating only a slight change in the ANZ operational risk profile. IRRBB RWA rose to $2.02 billion as of December 2015 due to realization of earlier gains.

The Credit risk weight intensity fell over 86 basis points during the quarter as well as improved performance across most of its asset classes. Lower RW intensive portfolios increases during the quarter (which even comprise 3.3% quarterly EAD growth in mortgages) was offset by the decrease in capital intensive exposures within Institutional. APRA Common Equity Tier 1 (CET1) ratio decreased to 9.4% as of December 2015 impacted by the group’s dividends. But, without the dividends impact, the CET1 ratio rose by 45 basis points as of December 2015 against the September 2015 boosted by the bank’s capital generation activities and proceeds from the Esanda portfolio sale. Recently, Australia and New Zealand Banking Group issued a $100 million subordinated notes for its Australian dollar debt issuance program. The bank also issued over JPY 20 billion of 1.183% fixed rate subordinated notes which is due at February 2026 pursuant to its US$60 billion Euro Medium Term Note Program.

Improving credit quality (Source: Company Reports)

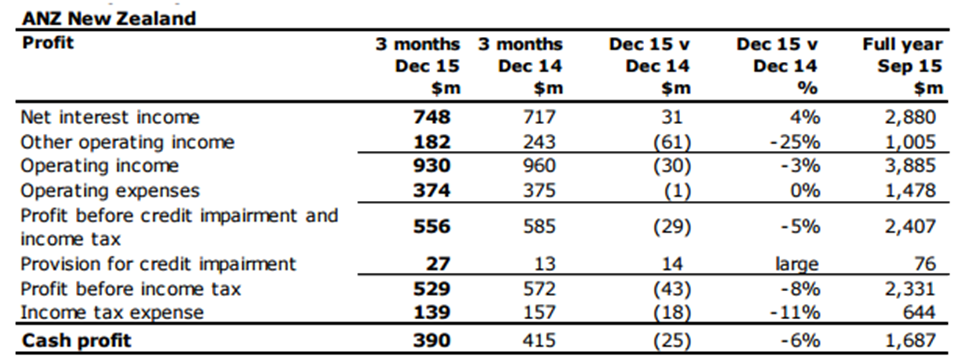

New Zealand division delivered a weak performance during the quarter: ANZ New Zealand divisions unaudited cash profit declined by 6% to NZ$390 million during the first quarter of 2016 as compared to NZ$415 million in the first quarter of 2015. Unaudited statutory profit fell by 18% to NZ$347 million during the period, as the region had to face the impact of credit risks which led to an increase in wholesale funding costs for the banks. But, Net interest income improved by 4% during the three months ended on December 2015 as compared to pcp, indicating the bank’s ongoing lending growth which rose by 8% during the period as compared to three months ended on December 2014.

Customer deposits rose by 4% in first half of 2016 against pcp while gross lending rose by 1% during the period. However, the interest margins have declined on the back of growing lending competition as well as the client’s choice for fixed-rate mortgages.

ANZ New Zealand performance (Source: Company Reports)

Stock Performance: The shares of Australia and New Zealand Banking Group continued to be under pressure even in 2016 and fell over 18.05% during this year to date (as of February 26, 2016) due to turmoil in the global markets and the group’s growth concerns in Asian regions which has been delivering a slower growth during first quarter of 2016. Management reported that the challenging manufacturing sector across Asia-Pacific, especially in South-East Asia have affected the group’s credit books. The group expects a further rise in market volatility and estimates its credit conditions to be more challenging during the second quarter of fiscal year of 2016. Therefore, Australia and New Zealand Banking Group estimates its overall Group credit charge to reach slightly above $800 million during the first half of 2016 as compared to its present market consensus of $735 million. Gross Impaired Assets during the first half of 2016 is estimated to be on track with the second half of 2015 even though the first quarter of 2016 performance was not on par with expectations. On the other hand, the bank was able to deliver a solid retail and small business performance in Australia and in New Zealand regions during the first quarter of 2016. ANZ also undertook restructuring efforts which include decreasing costs, strictly managing its credit and capital position as well as repositioning its business to enhance its efficiency in the coming periods. The bank is prudently allocating its resources to derive the best returns from its customer’s as well as from the shareholders.

ANZ was able to deliver a decent first quarter performance driven by its solid expense and margin management and we believe that the group would continue to control its expenses in the coming periods. We also note that DBRS Ratings Limited (DBRS) stated that the 1Q16 results of Australia and New Zealand Banking Group Limited indicate continued robust underlying fundamentals of the Australian banking sector while earnings headwinds owing to economic slowdown in Asia still prevail. Meanwhile, the heavy correction in ANZ stock has placed them at very attractive valuations which is trading at a lower P/E. The bank also has an outstanding dividend yield. Based on the foregoing, we give a “BUY” recommendation on ANZ at the current price of $22.40

.PNG)

ANZ Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...