Kalkine has a fully transformed New Avatar.

Company Overview: Australia and New Zealand Banking Group Limited provides a range of banking and financial products and services. The Company's segments include Australia; New Zealand; Institutional; Asia Retail & Pacific; Wealth Australia, and Technology, Services and Operations (TSO) and Group Centre. The Company's operations span Australia, New Zealand, and a number of countries in the Asia Pacific region, the United Kingdom, France, Germany and the United States. The Australia division consists of the retail and the corporate and commercial banking (C&CB) business units. The New Zealand division consists of the retail and the commercial business units. The Institutional division services global institutional and business customers. The Asia Retail & Pacific division consists of the Asia retail and the Pacific business units. The Wealth Australia division consists of the insurance and funds management business units. The TSO and Group Centre division provides support to the operating divisions.

.png)

ANZ Details

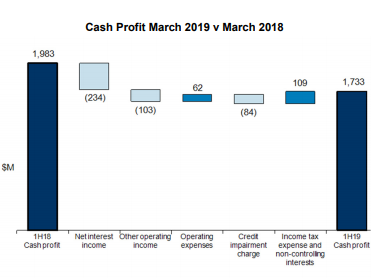

Marginal Rise in Cash Profit in 1HFY19 Amidst Certain Challenges: Australia and New Zealand Banking Group Limited (ASX: ANZ) recently released its half-yearly report ended March 2019 in which its cash profit from continuing operations witnessed a rise of $71 million (or 2%) as compared to March 2018 half and stood at $3,493 million. However, excluding the movements of foreign currency translation, the bank’s cash profit encountered a rise of $42 million (or 1%). The bank’s net interest income witnessed a fall of $51 million (or 1%) mainly because of 13 bps decrease in net interest margin, partially offset by the growth of 6% in the average interest earning assets. The bank’s lower net interest margin implies growth in the lower margin Markets Balance Sheet trading activities, a rise in the funding costs, changes with respect to asset mix, asset price competition, as well as the unloading of Asia Retail and Wealth businesses. The bank’s other operating income witnessed a fall of $73 million (or 3%) mainly because of net divestment impacts amounting to $81 million, a $64 million decrease in net fee and commission income, $60 million reduction in other, as well as a $29 million rise encountered in the customer remediation. The bank’s common equity tier 1 capital ratio stood at 11.5% which reflects a rise of 45 bps. Its cash RoE increased 13 bps and stood at 12.0% while the cash earnings per share witnessed a rise of 5% to 124.8 cents. The interim dividend amounted to 80 cents per share (fully franked), thus, equating to $2.27 billion to be shelled out to the shareholders.

Moving forward, the bank is expected to be aided by its strong balance sheet and by its focus towards costs. The bank had wrapped up its $3 billion buy-back which resulted in a 3.7% reduction in its shares and this helped in driving a robust increase in its earnings per share. The management stated that work commenced in 2016 focused towards simplification of the business as well as to strengthen the balance sheet had supported it to tackle strong headwinds in Australian retail banking. At CMP of $27.650, the stock of the bank is trading at P/E multiple 11.79x of FY20E EPS and P/BV multiple of 1.23x of FY20E Book Value of Equity per Share (BVPS). Hence, considering the high dividend, long-term growth potential, and cost management approach in the business model amidst certain challenges, we have valued the stock using 5-year average P/BV multiple to FY20E consensus Book Value Per Share (BVPS) of ~$22.4; and 5-year average P/E multiple to FY20E consensus EPS of ~$2.34 and have arrived at the target price upside of single digit growth (in %). Key risks related to rating: regulatory risk, subdued growth in the housing market, stiff competition, retail banking in Australia, etc.

.png)

Key Financial Metrics (Source: Company Reports, Thomson Reuters)

Decent Footing from Margins’ Standpoint: Australia and New Zealand Banking Group Limited’s efficiency ratio has witnessed improvement from the past few years as it declined from 60.1% in 1HFY16 to 50.8% in 1HFY19 which reflects that the bank’s usage of assets to post income has been quite well. Also, the bank plans to work towards its costs which might help in improving its bottom line position. The bank is maintaining its net interest margin at respectable levels which further strengthens the confidence in its fundamentals.

.png)

Key Metrics (Source: Thomson Reuters)

Top 10 Shareholders: Following table gives the broad picture of the top 10 shareholders in Australia and New Zealand Banking Group Limited:

.png)

Top 10 Shareholders (Source: Company Reports)

Understanding ANZ’s Australia Division’s Performance: In Australia division, the lending volumes witnessed a fall from lower system credit growth, asset competition and more conservative home loan origination risk settings in 1HFY19. This got partly offset by the growth witnessed in the Business & Private Bank. In half-year ended March 2019, the division’s net interest income stood at $4,091 million which reflects a fall from $4,325 million generated in the half-year to March 2018. The division’s net interest margin stood at 2.61% in 1H FY 2019 which reflects a marginal fall from the half-year ended March 2018 net interest margin of 2.78%. It was mainly impacted by increased funding costs, home loan mix changes & higher discounting, the regulatory impact on the credit card pricing, and increased customer remediation. This got partially offset by increased deposit margins and home loans re-pricing.

Australia Division’s Cash Profit (Source: Company Reports)

ANZ’s Institutional Division Witnessed a Rise in Lending Volumes: ANZ’s institutional division’s lending volumes witnessed a rise across loans & specialised finance and transaction banking. Also, the customer deposits encountered a rise in markets and transaction banking. The division’s net interest margin (ex-Markets) witnessed a rise because of increased deposit margins, partially offset by fall in the lending margins. The institutional division’s other operating income witnessed a rise because of increased markets income from franchise sales and trading which got partially offset by the lower balance sheet income.

Institutional Division (Source: Company Reports)

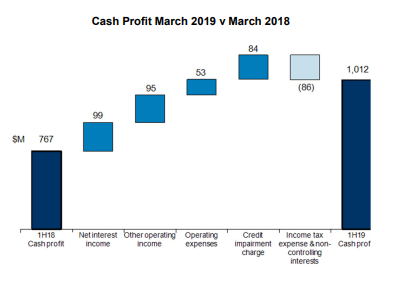

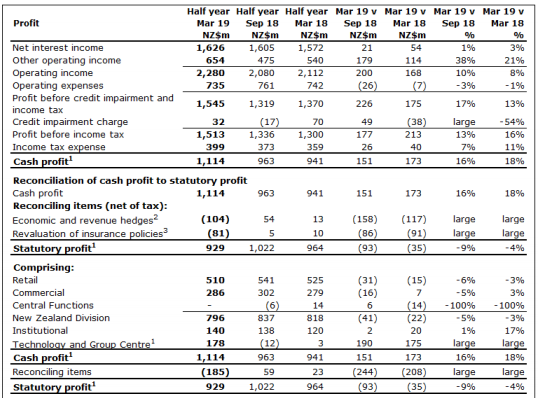

One-off transactions Supported ANZ’s NZ Cash NPAT: ANZ Bank New Zealand posted a statutory net profit after taxation (or NPAT) amounting to NZ$929 million in six months to March 31, 2019 which reflects a decrease of 4% on corresponding half in 2018 financial year. Its cash NPAT amounted to NZ$1,114 million, reflecting a rise of 18% because of one-off transactions which includes unloading of life insurance company OnePath Life (NZ) Limited as well as 25% share in Paymark Limited. Its expenses witnessed a fall of 1% because of the divestment impact of OnePath Life (NZ) Limited.

Key financial information of ANZ New Zealand (Source: Company Reports)

The low levels of credit losses reflect the improvements with respect to credit quality and benign credit environment and ANZ Bank New Zealand’s customer deposits witnessed a rise of 7% and gross lending encountered a 4% rise.

Update about Foreign Currency Dividend Payments: Australia and New Zealand Banking Group Limited would be shelling out proposed 2019 interim dividend in 3 different currencies i.e. Australian Dollars, Pounds Sterling and New Zealand Dollars. If the shareholder does not provide banking instructions in another designated currency to ANZ’s Share Registrar by no later than 5:00pm (Australian Eastern Standard Time) on May 15, 2019, ANZ’s proposed 2019 interim dividend which is payable to participating ANZ ordinary shareholders with a registered address in UK (including the Channel Islands and the Isle of Man) or New Zealand would be converted to their local currency at an exchange rate calculated on May 17, 2019 and would be payable in that currency only and the cash entitlements with respect to the proposed 2019 interim dividend would be payable to all other participating shareholders in AUD.

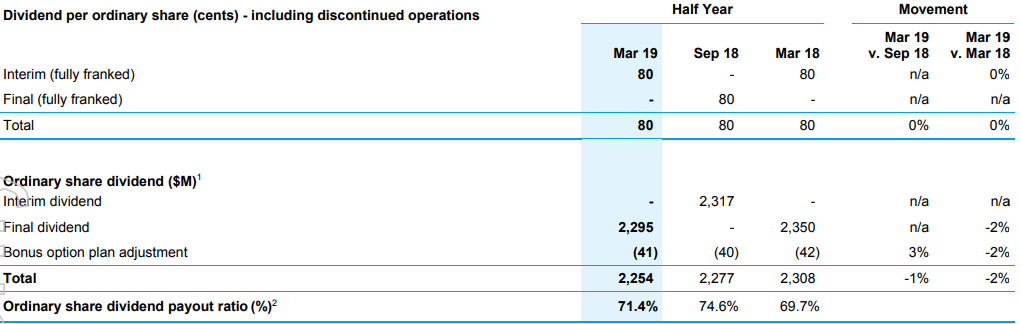

Decent Annual Dividend Yield Might Attract Attention: ANZ had proposed an interim dividend amounting to 80 cents per share which would be paid on each eligible fully paid ANZ ordinary share on July 1, 2019. The proposed 2019 interim dividend would be fully franked with regards to the Australian tax purposes. The bank has dividend reinvestment plan (or DRP) as well as a bonus option plan (or BOP) which would be operating in respect of proposed 2019 interim dividend.

Dividends (Source: Company Reports)

As reflected in the above picture, the bank’s ordinary share dividend payout ratio stood at 71.4% in half-year to March 2019 reflecting a rise as compared to half-year to March 2018 which might attract the attention of market players. The annual dividend yield of the bank is about 5.9% on a five-year average basis (FY14-18). Currently, the annual dividend yield of the bank happens to be at 5.8% which is higher than the banking industry average of 5.4%, representing more income for its shareholders than many peers. It has also wrapped up $3 billion on-market share buy-back. The net organic capital generation of +84 bps for 1H FY 2019 happens to be stronger than historical averages of +13 bps.

Key Valuation Metrics (Source: Company Reports)

What To Expect From ANZ: The top management of Australia and New Zealand Banking Group Limited stated that the performance in 1H FY19 was strong but there are headwinds which are facing the sector and the bank is taking appropriate action. As per them, the retail banking in Australia is expected to remain under pressure for foreseeable future and there would be subdued credit growth, intense competition as well as increased compliance costs which would be impacting earnings. The institutional banking is performing well, and this business is well-positioned to provide positive earnings diversification which would help in partially offsetting the headwinds in other parts of the group.

Historical P/E Band (Source: Company Reports)

The management added that New Zealand has been performing well but it is starting to share similar characteristics with the Australian market because of stiff competition as well as a slowing Auckland housing market. The major concern with respect to New Zealand is the impact of proposed capital changes on the broader economy. The Reserve Bank of New Zealand has been consulting on proposal for increases in Risk Weighted Assets (RWA) and minimum capital ratios. The overall impact on ANZ depends on numerous factors which include outcome of the consultation period, and regulatory changes that are underway by APRA.

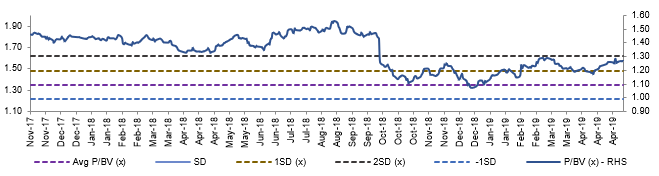

Historical P/BV Band (Source: Company Reports)

Stock Recommendation: The stock of ANZ provided decent returns from the past few months as, in the span of previous 3 months, its return came in at 2.60% while in the span of previous one month, the return stood at 6.94%. Also, the bank possesses decent annual dividend yield of 5.8% which could be another factor that might help in gaining traction among the market players. Moreover, the bank would be working on costs which could positively impact its bottom-line position and can further help in strengthening its overall position. As mentioned in its results presentation, the bank had looked upon 16 initiatives which cover retail customers, farmers, remuneration, accountability, culture & governance, remediation, dispute resolution and financial advice. Hence, considering strong results in 1H FY19, decent fundamentals and its focus on cost management, we have valued the stock using 5-year average P/BV multiple to FY20E consensus Book Value Per Share (BVPS) of ~$22.4; and 5-year average P/E multiple to FY20E consensus EPS of ~$2.34 and have arrived at the target price upside of single digit growth (in %). Given the backdrop of aforesaid parameters and current trading level, we give a “Buy” recommendation on the stock at the current market price of $27.650 (up 0.217% on 9 May 2019).

ANZ Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...