Company Overview - Australia and New Zealand Banking Group Limited (ANZ) provides a range of banking and financial products and services to retail, small business, corporate and institutional clients. The Company conducts its operations in Australia, New Zealand and the Asia Pacific region. The Company has 1,220 branches and other points of representation excluding Automatic Teller Machines (ATMs). The Company operates on a divisional structure with Australia, International and Institutional Banking (IIB), New Zealand and Global Wealth. ANZ’s business consists of raising funds through customer deposits and the wholesale debt markets and lending those funds to customers. ANZ also operates in other countries, including the United Kingdom and the United States.

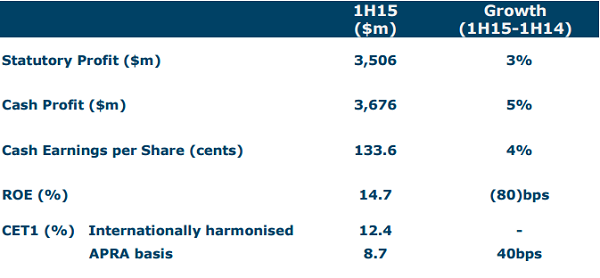

Analysis - Australia & New Zealand Banking Group Limited (ANZ) reported an impressive financial performance for the 2015 half year. Statutory profit after tax grew by 3% to $ 3.5 billion while cash profit was up by 5% to $ 3.7 billion. The fully franked interim dividend was $ .86 per share and the EPS was 133.6 cents per share both of which showed a growth of 4% and profit before provisions also grew by 4%. Customer deposits showed growth of 12% while net loans and advances were up by 10%. Provisions were 3% down at $ 510 million and return on equity stood at 14.7%. Common equity tier 1 ratio was 8.7% on the basis of Basel 3 Australian Prudential Regulation Authority which would be 12.4% on the basis of an international comparison.

Financial Performance (Source - Company Reports)

Financial Performance (Source - Company Reports)

CEO Mike Smith said that this was a solid and well balanced performance reflecting the progress made in adjusting to the more challenging macro environment. Domestic markets in Australia and New Zealand have again reported good growth and returns and the group continues to invest heavily to promote future profits especially in Australia. The focus continues to be on critical segments such as Home Lending and Commercial Banking especially in the underweight areas such as New South Wales. In New Zealand, the simplification and brand merger has consolidated the group's position as the leading bank in the country and the results from Global Wealth are good because of industry-leading innovation. International and Institutional Banking has performed despite the expansionary monetary policy and lower commodity prices.

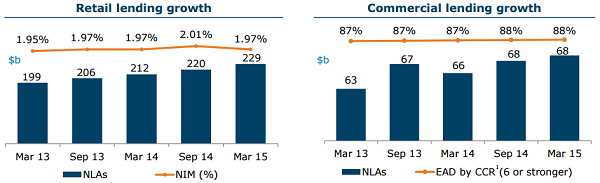

Lending Growth (Source - Company Reports)

Lending Growth (Source - Company Reports)

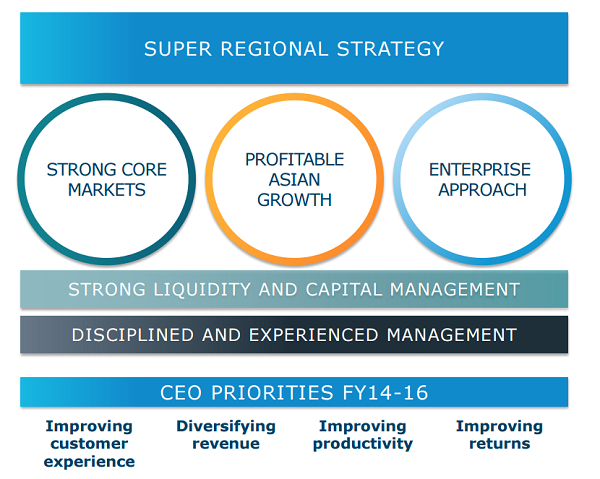

The outlook for the foreseeable future is that the group will continue to operate in a lower growth environment with occasional spells of volatility and shocks. The outlook for credit quality continues to be favourable because of low interest rates, the low oil prices and a strengthening USD. Growth in China is slowing but the country is handling the process well. The group believes that it will benefit from its Super Regional Strategy in the longer term and there will be opportunities to continue to improve financial performance in the shorter term. The 4% increase in the interim dividend will see around 73% being delivered to Australian retail and institutional investors and the payout for FY 2015 is likely to be at the higher end of 65% to 70% of cash profits.

Super Regional Strategy (Source - Company Reports)

Divisional performance

Australia

Super Regional Strategy (Source - Company Reports)

Divisional performance

Australia

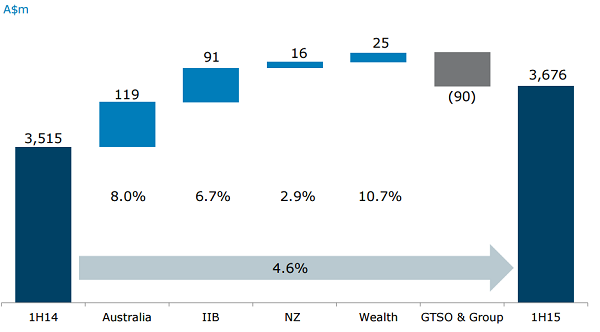

The Australian division delivered profit growth of 8% driven by a 6% growth in both income and profit before provisions. Investment opportunities in the country continue to be compelling because of both growth prospects and returns. As a result, investment in the half-year was increased focusing on the digital platform, growth in New South Wales and specialist platforms in corporate and commercial business such as Health and Emerging Corporates. Corporate and commercial loan volumes grew by 4% and retail loan volumes by 8% while deposits grew by 6% and 3% respectively. The strength in the historical Small-Business Banking sector continues with loans growing by 15% and deposits at $ 31 billion being more than double the level of loans.

Divisional Cash Profit (Source - Company Reports)

International and institutional banking

Divisional Cash Profit (Source - Company Reports)

International and institutional banking

The division profits grew by 7% because of Global Market customers and the cash management business. The geographical standout was Asia-Pacific, Europe and Americas where profit was up by 18%. Customer franchises continue to be strong rally in Asia where revenues have grown by 13% because of lower capital requirements and products with higher returns. The Trade business managed to maintain volumes though income was hit by lower commodity prices. Loan quality continued to be high with 79% being investment grade.

Cash Profit & Growth (Source - Company Reports)

New Zealand (all numbers in NZD)

Cash Profit & Growth (Source - Company Reports)

New Zealand (all numbers in NZD)

The business has generated more momentum with income growing by 6% and better quality cost control resulting in an 8% growth in PBP. Economic activity has been driven by increased consumer and business confidence and the profit growth of 1% showed a lower level of writeback of provisions. Customer numbers are growing because of the ever stronger brand, improve digital services and better quality service delivery. The commercial and agribusiness is flourishing with lending up by 6%.

Other businesses

Profits grew by 11% on the back of the performance from the insurance business while Private and Wealth Management Services showed strong market performance and improved volumes. The business now has 2.4 million customers with more than $68 billion in investments and retirement savings. Global technology, services and operations saw continuing investment in common platforms and IT infrastructure modernisation and the improvements in efficiency is evidenced by the fact that operating costs decline by 3% despite a 7% increase in transaction volumes. Credit quality continues to improve with a 3% decline in provisioning costs and the total loss rate saw a moderate decline from 21 basis points to 19 basis points at which level it is expected to stabilise for the second half of the year.

Revenue Drivers (Source - Company Reports)

Revenue Drivers (Source - Company Reports)

Investor Day New Zealand update

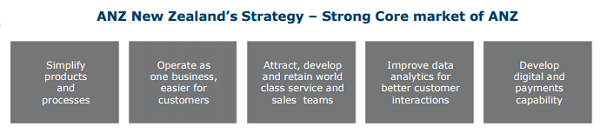

86% of the population earns less than NZD 70,000 annually with only 6% earning more than NZD 100,000. The population is expected to touch 5 million by the year 2030 with the help of migration. The GDP contribution by industry leads with Finance and Business at 27% followed by Services and Others at 22%. Around 88 % of the banking market is divided between the big four with the market share of ANZ at 31% on top followed by the others. ANZ has followed the strategy of simplifying processes and products, operate as a single business making it easier for customers, attracting and developing international quality talent, improving analysis for superior customer interaction and beefing up digital and payment capabilities. The creation of scale and leveraging it has resulted in creating what is arguably the biggest and the best bank in the country.

ANZ New Zealand Strategy (Source - Company Reports)

ANZ New Zealand Strategy (Source - Company Reports)

The macro view on Australian banks

Australian banks, or at least two of them, have relatively new CEOs and the latest Westpac Bank’s new chief Brian Hartzer has just released numbers that were about 15% below the expectations of the market. Share prices are falling since the peak in March 2015 though the run of bank stocks has been impressive over the last couple of years. Loan growth has been lagging and Australian banking regulators have been vocal about property growth leading to the possibility of further capital raising. In addition, macro economic data has not been encouraging and capital expenditure in the quarter for March has fallen far more steeply than had been expected. The outlook for the year to June 2016 is likely to be worse.

ANZ Daily Chart (Source - Thomson Reuters)

ANZ Daily Chart (Source - Thomson Reuters)

Despite all this gloomy prognostication, ANZ is well placed to cope because of all its initiatives and its impressive track record. It is also a market leader in its countries of operation and looks set to continue its growth. We put a BUY recommendation on the stock at the current price of $31.85.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...