Kalkine has a fully transformed New Avatar.

Company Overview: Ausdrill Limited is an exploration and production drilling company. The Company focuses on providing a range of services to mining clients. It operates in four segments: Drilling Services Australia, Contract Mining Services Africa, Equipment Services & Supplies, and All Other. The Drilling Services Australia segment is engaged in the provision of drilling services and drilling equipment, including drilling and blasting, in-pit grade control, exploration drilling and wet water well drilling in Australia. The Contract Mining Services Africa segment is engaged in the provision of mining services, including drilling and blasting, in-pit grade control, exploration drilling and earthmoving in Africa. The Equipment Services & Supplies segment is engaged in the provision of mining supplies, products and services, including equipment hire, equipment parts and sales across the world. The All Other segment includes the provision of energy drilling and equipment hire, and material analysis.

.png)

ASL Details

ASL’s Revenue Doubled To $2 Billion Presently from August 2018: Ausdrill Limited (ASX: ASL) is a small-cap diversified mining services company with the market capitalisation of ~$1.23 Bn as of 7 August 2019. It has been involved in successfully delivering services across every stage of the mining lifecycle, with a focus on production. The company has recently presented its business prospects at Diggers and Dealers mining forum, where it highlighted that in August 2019, its revenue doubled to approximately $2 billion as compared to around $1 billion in August 2018. Its number of employees increased from 6K+ to 8K+ presently. Its presence has increased from 10 countries in August 2018 to 13 in August 2019, and its number of projects increased from 36 in August 2018 to 55 in August 2019. Its order book increased from around $2.3 billion in August 2018 to $6.7 billion presently.

.png)

Transformational Growth (Source: Company Reports)

In Australia, the company’s service offerings include drill and blast, grade control, water well drilling, exploration drilling, mineral analytics, equipment sales and hire, and parts sales. Its Australian regional footprint includes operations based in Western Australia, Queensland, South Australia, New South Wales, and Northern Territory. In Africa, the group offers load and haul and crusher feed services that the Group provides in Australia. The Group provides specialist underground mining services, including high speed decline development and production, through its 50-50 JV with Barminco Limited, African Underground Mining Services. Its Australian operations are diversified across a portfolio of clients and jurisdictions including Ghana, Mali, Burkina Faso, Senegal, Cote d’loire, Tanzania, South Africa, and Zambia.

The company’s decent financial performance where its revenue almost doubled in a year, and its growing pipeline which can be supported by the fact that its order book increased by 191% from August 2018, is expected to help it in delivering a sustainable return to its shareholders in the coming times.

.png)

ASL’s Global Presence (Source: Company Reports)

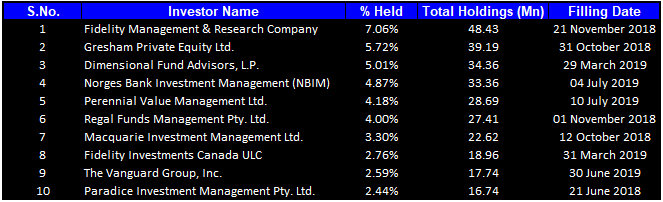

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 41.93% of the total shareholding. Fidelity Management & Research Company and Gresham Private Equity Ltd. hold maximum interest in the company at 7.06% and 5.72%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

West African Resources Appoints ASL’s subsidiary for Open-Pit Mining Contract: ASL updated the market that Gold developer West African Resources Limited has appointed Ausdrill Ltd’s wholly-owned subsidiary, namely African Mining Services (“AMS”), as preferred tenderer for the open-pit mining contract for the Sanbrado Gold Project. AMS has a strong track record in the region with over 9 years of operating experience in Burkina Faso and 30 years’ experience in West Africa. Both AMS and West African Resources are in the process of finalising the contract terms, which will include the provision of an optional deferred payment arrangement for up to US$10m at a commercial interest rate, with works expected to commence in early CY2020.

Being selected as a preferred contractor at the Sanbrado Gold Project is a significant achievement for AMS. It will boost its morale in its endeavour to enhance its surface operations in Africa and target substantial growth opportunities across a range of commodities in select African countries.

On July 19, 2019, ASL informed the market about the approximately A$800 million, five-year underground mining services contract at the Zone 5 Mine in Botswana recently awarded to Ausdrill’s subsidiary, Barminco, from Khoemacau Copper Mines. This is one of the largest contracts awarded to Barminco and a major opportunity for Ausdrill under its international growth strategy. Khoemacau’s Zone 5 operation is a new, large, and long-life mine development project located in the highly-prospective Kalahari copper belt in Botswana. Under the contract, Barminco will perform mine development, establishment of underground mine infrastructure, diamond drilling and mine production at an initial rate of 3.6 million tonnes per annum of copper ore with multiple expansion opportunities.

The funding package has successfully closed, and the company is looking forward to delivering on this significant project, with preparations underway to commence mining services at the Zone 5 mine in December 2019.

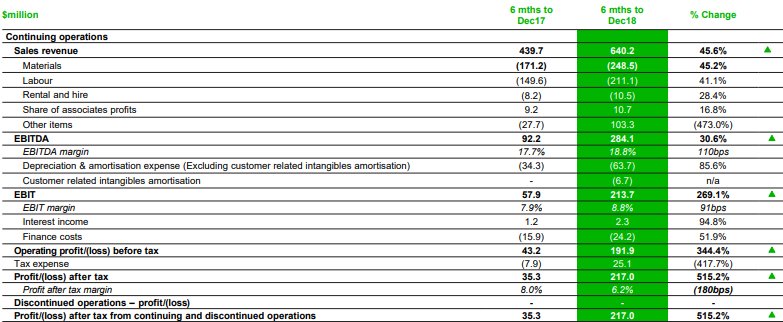

H1FY19 Key Highlights: The revenue from operations for the half-year period was reported at $640.2 million, which is a 45.6% increase as compared to the previous corresponding period. The underlying results include two months of contribution from Barminco and its additional 50% share in African Underground Mining Services (AUMS) that was acquired in October 31, 2018. On a proforma basis, and to enable comparison, the group had made the Barminco acquisition at the start of the financial year the underlying proforma NPAT would have been $55.2 million.

The Group’s statutory NPAT for the period was $217.0 million, which is a 515.2% increase as compared to the previous corresponding period. This increase in the statutory results are due to a significant uplift from one-off, non-cash items relating to the accounting treatment of the acquisition, which included $198.4 million accounting gain from the revaluation of Ausdrill’s 50 % share of AUMS that the Company owned prior to the acquisition of Barminco, and a $30.7 million taxation benefit that was largely related to the Barminco transaction. Meanwhile, Ausdrill also recorded a $31.2 million impairment to the value of its Energy Drilling Australia assets, which have been in care and maintenance since FY16. In addition, there were some smaller one-off costs, including transaction and redundancy costs.

At the end of the period, ASL’s cash reserves stood at $198.9 million and undrawn debt facilities of $176.5 million. Its credit ratings were upgraded in November 2018 by both Moody’s Investor Services and Standard and Poor’s to Ba2 and BB, respectively, following the completion of the Barminco acquisition.

Due to improvement in performance, the Board of Directors declared a fully franked interim dividend of 3.5 cents per share for the half year period ended on December 31, 2018.

H1FY19 Income Statement (Source: Company Reports)

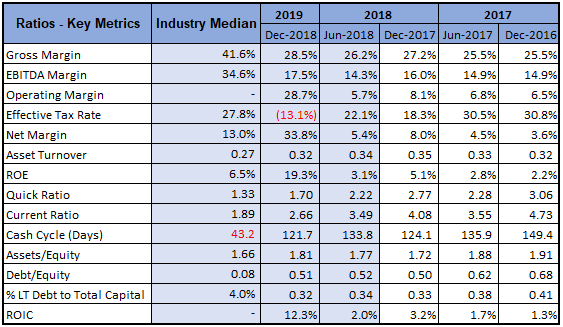

A Quick Look at Key Metrics: Its net margin for H1FY19 stood at 33.8%, better than the industry median of 13.0%, which indicates the company is efficiently converting top-line to the bottom-line. Its gross margin and EBITDA margin improved from 27.2% and 16.0% in H1FY18 to 28.5% and 17.5%, respectively, in H1FY19, which implies decent fundamentals of the company. Its ROE for H1FY19 stood at 19.3%, better than the industry median of 6.5%, which implies that the company generated a better return for its shareholders than its peer group. Its current ratio for H1FY19 stood at 2.66x, better than the industry median of 1.89x, which implies the company is in a better position to address its short-term obligations than its peer group.

Key Metrics (Source: Thomson Reuters)

Key Risks: ASL’s business is vulnerable to few risks such as level of new mining services contracts and contract renewables; currency fluctuations; labour costs and availability; risks associated with doing business in Africa (eg. Health Risk (Ebola Virus Outbreak in 2014), political instability, war or civil disturbances, etc.); regulatory compliances and change in laws, uninsured risks such as blowouts in the mining operations, cratering, explosions, fires, loss of hole, damages or loss of equipment and damage or loss from inclement weather or natural disasters, etc.

What to expect: The underground mining is presenting significant organic growth opportunities across Australia and Africa. Company’s strong orderbook coupled with organic growth opportunities makes a strong case for continued growth in underground. The Surface mining is presenting significant organic growth opportunities across a range of commodities in Africa. The company is expected to focus on enhancing its earnings and cash conversion from existing operations.

The demand for equipment rental, parts and services continue to grow, which will help the company’s investments group to continue to grow on the back of the mining re-investment cycle. Provided strong pipeline and growth, the second half of FY19 will provide base line for FY20, which will also benefit from the full year synergies of approximately $11 Mn. The company is on track to achieve its earnings guidance of underlying net profit after tax of $98 million for FY19.

.png)

ASL’s Strategic Pillars (Source: Company Reports)

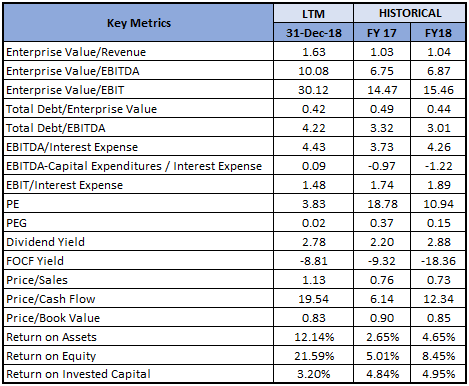

Key Valuation Metrics (Source: Thomson Reuters)

Method 1- Price to Earnings Multiple Approach (NTM):

(8).png)

Price to Earnings Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

Method 2- EV/EBITDA Multiple Approach (NTM):

(2).png)

EV/EBITDA Multiple Approach (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: Ausdrill’s share generated decent YTD return of 59.29%, and 26.76% return in the span of just 3 months. ASL’s strong financial position ensures that the company is well-positioned to fund newly awarded projects and capitalise on growth and investment opportunities. With the decent volume growth visibility, healthy balance sheet, respectable operating margins, and return ratios, we have valued the stock using two Relative valuation methods, P/E and EV/EBITDA multiple and have arrived at the target price upside of high single-digit to low double-digit growth (in %). Hence, in view of aforesaid parameters and current trading levels, we recommend a “Buy” rating on the stock at the current market price of $1.820 per share, up 1.111% on August 7, 2019.

(1).png)

ASL Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...