Company Overview: Aurizon Holdings Limited (ASX: AZJ) is Australia’s leading rail freight operator which provides integrated freight and logistics solutions across an extensive national rail and road network, traversing Australia. The company also transports coal from mines in Queensland and New South Wales to end customers and ports. Its network team is focused on creating a rail network that is reliable and available for its customers to support Queensland’s strong coal industry. The company’s vision is to be the first choice for bulk commodity transport solutions and its purpose is to grow regional Australia by delivering bulk commodities to the world..png)

AZJ Details

.PNG)

Continued Focus on Operational Efficiency: Aurizon Holdings Limited (ASX: AZJ) is Australia’s leading rail freight operator which specializes in the services of rail design, engineering and construction and offers large-scale supply chain solutions to various types of customers. The company has three major avenues: Network, Coal and Bulk. Lately, the company’s Coal business secured key contract extensions, delivering on its strategy of de-risking and extending the contract book. AZJ’s Bulk business is currently progressing ahead of expectations with strong performance driven by new contracts and operational efficiencies. The Network business continues to deliver significant regulatory reforms and several benefits for the entire coal supply chain. Further, the company continues to focus on operational efficiency to continuously improve its operational performance, asset efficiency and cost competitiveness. Last year, the company delivered on several key strategic priorities which have placed it well to deliver long-term value for shareholders.

Lately, the company has removed much of the regulatory uncertainty that impacted its business for the past couple of years, allowing it to focus more on its core business, drive further transformation and provide safe and efficient service to its customers. Looking forward, the company’s Bulk business is well placed to benefit from the continued long-term growth in demand for Australia’s high-quality resources including inputs such as silver, lithium, cobalt and nickel, that are underpinning the rapid global growth in battery power, solar, electric cars, telecommunications and wind turbines. .png)

Historical Performance (Source: Company Reports)

FY19 Results Highlights: In FY19, Aurizon Holdings Limited delivered on its commitment of returning surplus capital to shareholders. During the year, the company announced a $300 million on-market share buy-back which later got extended by $100 million to $400 million. The company paid total dividends of 23.8 cents per share in FY19, representing 100% of Underlying Net Profit After Tax. The company’s Underlying Earnings Before Interest and Tax for FY19 stood at $829 million. The Non-Network businesses delivered a $450.1 million contribution to EBIT, exceeding the guidance range for FY19. Further, Aurizon Network business delivered a $400 million contribution to EBIT.

In FY19, the company witnessed record tonnages across the Central Queensland Coal Network (CQCN) of 232.7 million tonnes. In addition, it saw new customers and improved business operations in Coal and Bulk. In Coal business, the company secured key contract extensions over the year, which has the effect of extending the expiry profile of the portfolio, with 72% of its contracts having a duration of seven years or more..png)

FY19 Results Snapshot (Source: Company Reports)

Improved Performance in H1FY20: In the first half of FY20, the company recorded Underlying EBIT of $456 million, up 12% on pcp. The company’s underlying NPAT stood at $269 million in H1FY20, up 19% on pcp. The improved results were mainly due to higher EBIT performance in the Network business and strong performance by the Bulk business driven by new contracts and operational efficiencies.

During the period, the Return on Invested Capital (ROIC) improved by 0.5ppt to 10.5% and free cash flow from continuing operations increased by 26% to $465 million due to the proceeds from sale of the Rail Grinding business. In the Coal business, a total of 106.3 million tonnes of coal was railed in Queensland and New South Wales in H1FY20.

In the Network business, around 116.6 million tonnes was railed across the Central Queensland Coal Network in H1FY20. During the period, Bulk’s underlying EBIT improved from $14 million to $44 million, mainly due to the securing of new contracts, expanded services and additional volumes with existing customers, and cost reductions..png)

H1FY20 Results Summary (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 18.56% of the total shareholding. BlackRock Institutional Trust Company, N.A. and Vanguard Investments Australia Ltd. hold the maximum interests in the company at 3.67% and 3.04%, respectively.

.png)

Top 10 Shareholders (Source: Refinitiv, Thomson Reuters)

Decent Track Record of Paying Dividend: Over the last four years, the company has been paying 100% of its Underlying Net Profit After Tax as dividends. For FY19, the company paid a total dividend of 23.8 cents per share, 70% franked, representing 100% payout of underlying NPAT from continuing operations. For H1FY20, the company declared an interim dividend of 13.7 cents per share (70% franked), up 20% on pcp, representing 100% of Underlying NPAT..png)

Dividend History (Source: Company Reports)

COVID-19 Update: On 16 April 2020, the company released a March quarter update, wherein, it confirmed that it has experienced no material impact to Coal or Bulk above rail volumes in the quarter from COVID-19. In response to Covid-19, the company has implemented various preventative measures including new workplace protocols for business critical and operational teams and working from home where possible for the remainder of the staff.

March Quarter Update: In the March 2020 Quarter, the company saw 2% increase in total above rail volumes, if compared to pcp. This was mainly due to increased volumes in Bulk, with Coal volumes remaining flat. In the Coal business, the company saw higher CQCN volumes during the quarter, however it was offset by lower NSW/SEQ volumes. In the Bulk business, the company’s volumes in March quarter were 12% higher compared to the pcp, driven by stronger volumes for Iron Ore and Bulk East with Bulk West volumes flat..png)

March 2020 Quarter Volumes Snapshot (Source: Company Reports)

A Quick Look at Key Ratios: For H1FY20, the company’s EBITDA margin stood at 54.7%, up 7.8% on pcp. For the same period, the company reported a net margin of 22.4%, up 6.8%, demonstrating improving profitability. The company currently has an Asset to Equity ratio of 2.11x and Debt to Equity ratio of 0.74x..png)

Key Metrics (Source: Refinitiv, Thomson Reuters)

Aurizon to sell the Acacia Ridge Terminal: Recently, the Full Federal Court dismissed an appeal by the Australian Competition and Consumer Commission (ACCC) and cleared the way for Aurizon to sell the Acacia Ridge Terminal to Pacific National. The sale now only requires approval by the Foreign Investment Review Board. With the completion of this transaction, the company will complete its three-stage exit from its loss-making Intermodal business.

What to expect: Looking forward, the company expects its Bulk business to benefit from continued long-term growth in demand for Australia’s high-quality resources. Following the strong results in H1FY20, the company has reaffirmed its EBIT guidance of $880 million - $930 million for FY2020.

The company continues to focus on operational efficiency to continuously improve its operational performance, asset efficiency and cost competitiveness. The company expects its Above Rail Coal volumes to be in the range of 210mt to 220mt in FY20, assuming no major weather impact or change to operating conditions occurring during 2HFY20.

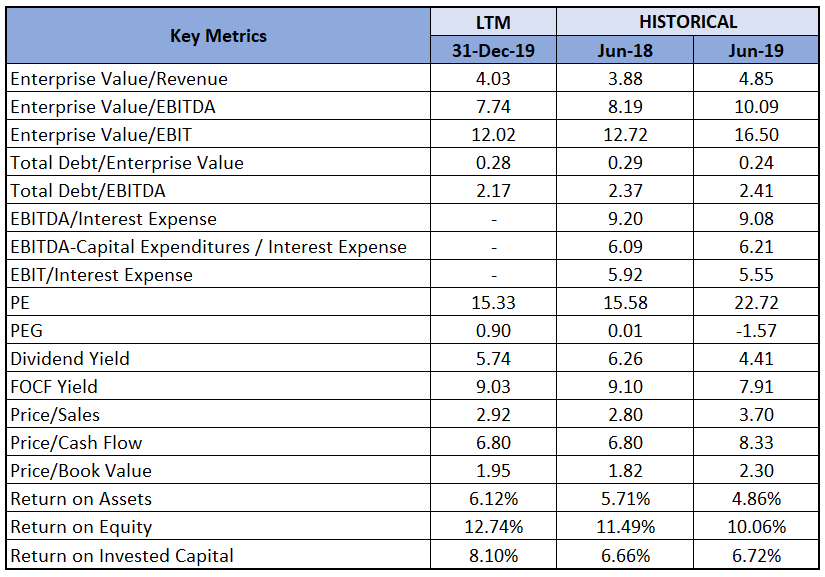

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

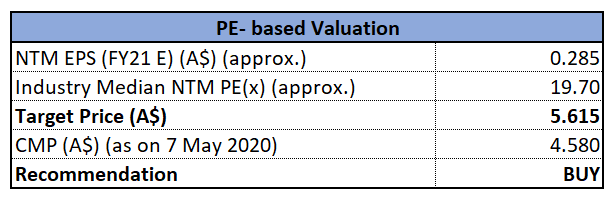

Valuation Methodology: P/E Multiple Based Relative Valuation Approach (Illustrative)

P/E Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: In the past six months, the stock of AZJ has declined by 20.45% on ASX and is currently trading lower than the average of its 52-weeks low and high price of $3.380 and $6.110, respectively, offering a decent opportunity for accumulation. We have valued the stock using Price to earnings multiple based illustrative relative valuation method and arrived at a target price of lower double-digit upside (in % terms). Considering the company’s resilient performance amid COVID-19 pandemic, its decent performance in H1FY20, strong track record of paying dividends and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $4.580, up by 0.659% on 7 May 2020.

.png)

AZJ Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...