Company Overview: Aurizon Holdings Limited (ASX: AZJ) happens to be an integrated heavy haul freight railway operator and rail transporter of coal from mine to port for the export markets. Moreover, it has portfolio of other bulk, general and containerised freight businesses and large-scale rail services activities. The company carries out its operations via reportable segments namely, 1) Network, 2) Coal, 3) Bulk, and 4) Other. The company has been transporting over 250 million tonnes of Australian commodities, connecting miners, primary producers as well as industry the domestic and international markets. The company works for the sole purpose of growing regional Australia by delivering bulk commodities to the world..png)

AZJ Details

.png)

Decent Results in 1H FY 2020: Aurizon Holdings Limited (ASX: AZJ) is Australia’s leading rail freight operator and is categorised in top 50 ASX company. As on March 26, 2020, the market capitalisation of Aurizon Holdings Limited stood at ~A$8.31 billion. The company recently declared its results for the half-year ended December 2019 wherein it posted underlying earnings before interest and tax (or EBIT) amounting to $456 million in its continuing operations reflecting an increase of 12% on pcp basis. The growth was witnessed mainly because of higher EBIT performance in network business delivered by increased revenue from UT5 Undertaking and robust performance by bulk business due to new contracts and operational efficiencies. The company’s underlying net profit after tax (or NPAT) amounted to $269 million, reflecting an increase of 19% from 1H FY 2019. Its statutory NPAT rose by 51% to $343 million as compared to 1H FY 2019, reflecting profit on sale of Aurizon’s Rail Grinding business. Notably, return on invested capital (or ROIC) witnessed an improvement by 0.5 ppt to 10.5% as compared to 1H FY 2019. The company’s free cash flow from continuing operations went up by 26% to $465 million as a result of proceeds of sale from rail grinding business.

The company’s total current liabilities (excluding borrowings) declined by $101.2 million mainly because of $94.9 million reductions in trade and other payables primarily due to settlement of $81.3 million over collection of access revenue in FY 2019, $38.0 million reductions in the employee benefits provisions, partly compensated by $27.0 million increase in the other liabilities including $9.8 million because of adopting of AASB16. Its total borrowings rose $2.2 million including, $82 million proceeds from the issuance of Australian Dollar Medium Term Note partly offset by $45 million net repayment of the bank debt facilities and $36 million revaluation (favourable) of the Euro Medium Term Notes. The company’s other non-current liabilities rose by $132.8 million mainly due to $49.8 million increase in the net deferred tax liabilities and $78.4 million increase in other liabilities mainly due to the adoption of AASB 16. The company’s Board of Directors managed to declare an interim dividend amounting to 13.7 cents per share (70% franked), which is 100% of the underlying NPAT and a rise of 20% on a YoY basis. The increase in interim dividend might attract the attention of the market participants moving forward. Keeping in view that the company is paying dividends consistently with ~4.93% dividend yield on five-year average basis and focus on building fund management business,

Given the backdrop of decent long-term outlook, business strategy towards improving operational efficiency, and maintaining 100% dividend payout ratio over the last five years, we have applied two relative valuation methods, i.e., EV/Sales multiple and Price/Cashflow multiple and arrived at a target price of lower double-digit upside (in % terms). .png)

Key Financial Highlights (A$ Mn) (Source: Company Reports, Thomson Reuters)

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Aurizon Holdings Limited:.png)

Top 10 Shareholders (Source: Thomson Reuters)

Improvement in Key Margins: The company net margin of 22.4% in 1H FY 2020 which implies an increase from 1H FY 2019 figure of 15.6% and, therefore, it can be said that AZJ is possessing decent capabilities to convert its top-line into the bottom-line. Its gross margin stood at 75.5%, an improvement from 74.3%. AZJ’s RoE stood at 7.4% in 1H FY 2020, reflecting an increase from 1H FY 2019 figure of 4.8%, thus, it looks like the company has been delivering decent returns to its shareholders..png)

Key Metrics (Source: Thomson Reuters)

The percentage of long-term debt to total capital stood at 33.8% in 1H FY 2020 as compared to 1H FY 2019 figure of 40.5% and, therefore, it can be said that AZJ has reduced its exposure towards long-term debt. Generally, lower exposure towards long-term debt reflects that the company can focus towards its growth prospects and it can make deployments which could help it in achieving overall growth.

Appointment of Group Executive Network: Aurizon Holdings Limited has recently made an announcement that Pam Bains has been appointed to the position of Group Executive Network. Her appointment as Group Executive Network follows resignation of Michael Riches in the month of December 2019. The company’s Managing Director & CEO named Andrew Harding stated that Pam was ideally positioned to deliver the next phase of transformation for Network business as it implements UT5 Undertaking.

Information on Share buy-back: On August 12, 2019, AZJ has made an announcement about its intention to undertake on-market share buy-back of up to $300 million during FY 2020. Later on, this was increased on February 10, 2020 by $100 million to $400 million, which confirms the company’s commitment to returning surplus capital to the shareholders. As of 24 March 2020, the group has bought back a total of 7,35,37,989 shares via on-market trade for the total consideration of A$ 39,05,05,230.4.

Overview of AZJ’s Funding: An improvement in the legal and capital structure was implemented in 1H FY 2020 which results in the more efficient balance sheet as well as funding structure. AZJ happens to be committed towards diversifying the debt investor base and increasing the average debt tenor. In July 2019, Aurizon Network Pty Ltd (which is the wholly owned subsidiary of the group) reduced the capacity of syndicated bank debt facility expiring in the month of July 2021 from $490 million to $380 million. On September 25, 2019, Aurizon Network Pty Ltd issued the long term $82.0 million fixed rate Medium Term Note, which expires on March 22, 2030.

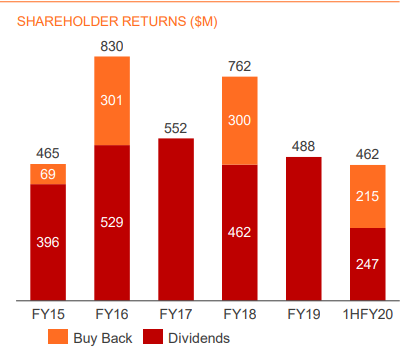

Interim Dividend Increased 20% YoY in 1H FY 2020: The company has declared an interim dividend amounting to 13.7 cents per share (or cps) (70% franked), which implies 100% of the underlying NPAT and a rise of 20% as compared to prior corresponding period (or pcp). The annual dividend yield of AZJ is about 4.93% on a five-year average basis (FY15-19) and current dividend yield trades at 6.24%. The following image provides a broader overview of the shareholders returns:

Shareholder Returns (Source: Company Reports)

The company has managed to maintain 100% payout ratio since 2H FY 2015 which could attract the attention of the investors seeking dividend payments.

What to Expect from AZJ Moving Forward: The company is maintaining its FY 2020 underlying EBIT guidance in the range of $880 million - $930 million, and operational efficiency improvements is expected to be the primary driver of performance. The guidance has been given based on certain assumptions like there would be no material impacts because of adverse weather or coronavirus situation. Also, with respect to Network, uplift in WACC from 5.9% to 6.3% in mid CY 2020 has been assumed.

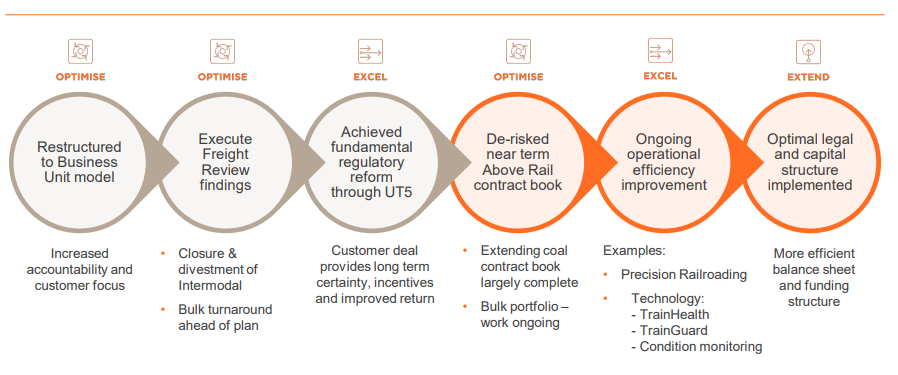

Aurizon’s Strategy (Source: Company Reports)

The company’s strategy enables delivery of the shareholder value and, since optimal legal and capital structure has been implemented, more efficient balance sheet and funding structure might help the overall company moving forward..png)

Key Valuation Metrics (Source: Company Reports)

Valuation Methodologies:

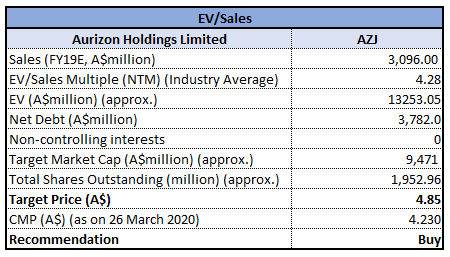

Method 1: EV/Sales Based Relative Valuation

EV/Sales Based Valuation (Source: Thomson Reuters)

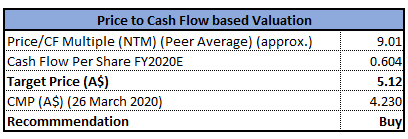

Method 2: Price to Cashflow Based Relative Valuation

Price to Cashflow Based Relative Valuation (Source: Thomson Reuters)

Stock Recommendation: In FY 2019, AZJ decided to pay out 100% of the underlying net profit after tax in the form of dividends, which is consistent with its practice for last 4 years. The Board of Directors declared final dividend amounting to 12.4 cents per share (or cps) (70% franked). This took the total dividends for FY 2019 to 23.8 cents per share (70% franked). In the annual report for FY 2019, the company stated that it remains committed towards improving efficiency as well as safety of the operations in order to deliver benefits for customers and shareholders. Also, technology plays a crucial role in this and the company has been investing towards the initiatives that would be improving locomotive reliability, program diagnosis, driving techniques along with operational safety.

We have applied two relative valuation methods, i.e., EV/Sales multiple and Price/Cashflow multiples and arrived at a target price of lower double-digit (in % terms). On the backdrop of above factors, increase in interim dividend of 20%, reduction in the exposure towards long-term debt as a percentage of total capital, maintenance of FY 2020 guidance, improvement in legal and capital structure, and expected upside, we give a “Buy” rating on the stock at the current price of A$4.230 per share, down by 1.856% on March 26, 2020.

.png)

AZJ Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...