Company Overview - Aurizon Holdings Ltd. (Aurizon) is an Australia-based rail freight operator. The Company acts as a heavy haul freight railway operator; rail transporter of coal from mine to port for export markets; engages in bulk general and containerized freight businesses, and rail services activities. Its segments include Network, Commercial & Marketing, Operations and Other. The Network segment provides access to, operation and management of the Central Queensland Coal Rail Network. It also provides overhaul and maintenance of rail network assets. The Commercial & Marketing segment is engaged in commercial negotiation of sales contracts and customer relationship management. The Operations segment is engaged in the national delivery of coal, iron ore, bulk and intermodal haulage services. It also includes yard operations, fleet maintenance, operations, engineering and technology, engineering program delivery and safety, health and environment. It also maintains rolling stock fleet assets.

AZJ Dividend Details

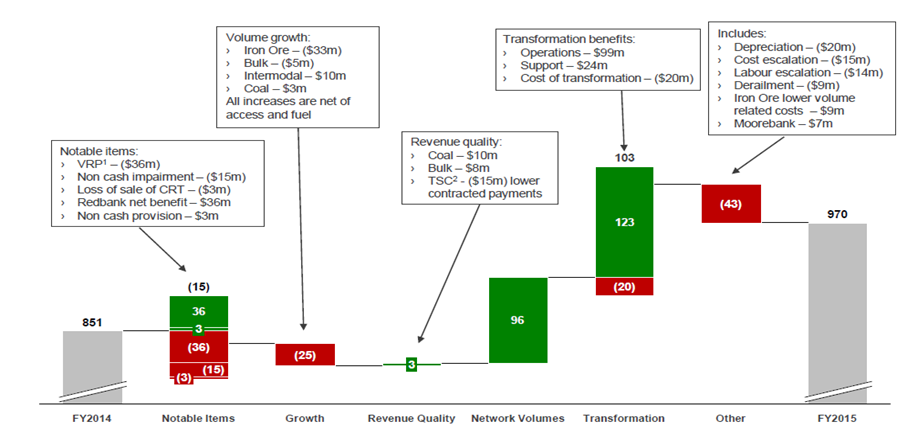

Transformation program contributed to performance:

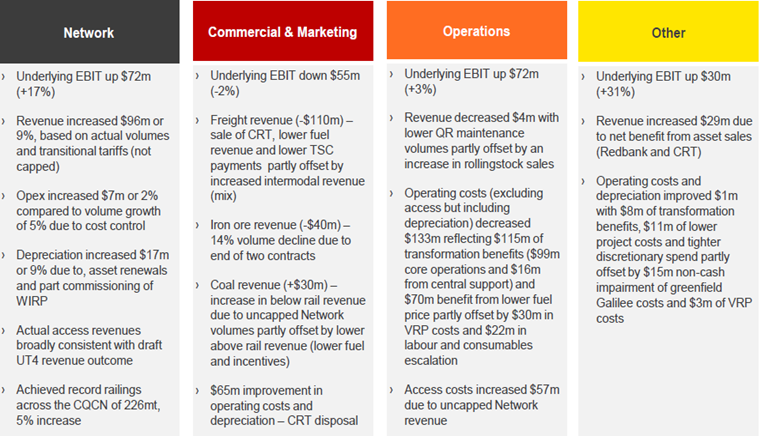

Aurizon Holdings Ltd (ASX: AZJ) reported a slight revenue decrease by 1% year on year (yoy) to $3.78 billion during fiscal year of 2015 but delivered a 14% yoy increase in underlying EBIT to $970 million while statutory NPAT surged by 139% yoy to $604 million. The group’s transformation program coupled with productivity enhancements efforts contributed to the bottom line performance. The group generated over $123 million benefits via its transformation program during the period. Aurizon Holdings also improved its return in invested capital (ROIC) by 0.9 percentage points to 9.7% during FY15. The group reported a 45% year over year increase of dividends to 24 cents per share in FY15. AZJ delivered 226 million tonnes of coal across its Central Queensland Coal Network while generated 211 million tonnes of coal in its New South Wales and Queensland operations. The group’s iron ore business was on track with the forecasts of 26 million tonnes in FY15 while its general freight business hauled at 46 million tonnes. Recently, the company also announced for some senior management changes with the sudden departure of Mike Franczak, Executive Vice President, Operations.

FY15 performance across AZJ divisions (Source: Company Reports)

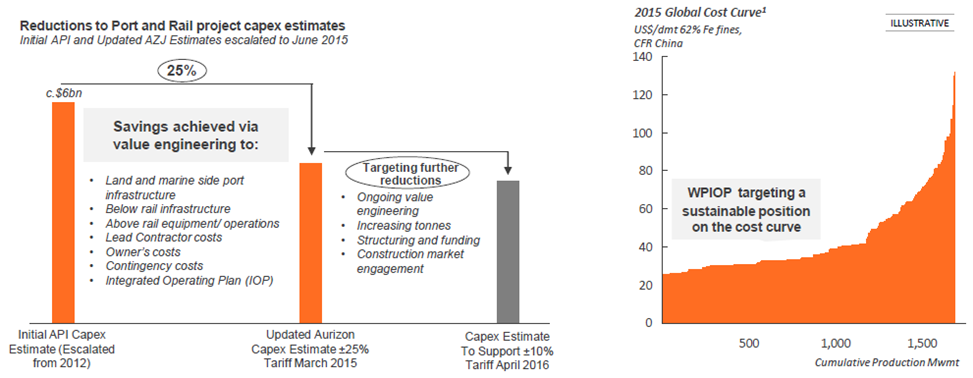

Developing growth opportunities: Aurizon Holdings Ltd is continuously seeking growth opportunities and diversifying its business to offset tough commodity market pressure. As a result, AZJ started the ramp-up of its long-term Whitehaven Coal contract in New South Wales, including the Maules Creek mine since March 2015. Ongoing expansion of its NSW coal business generated 6% volume increase in FY2015, while AZJ continues to further invest in NSW coal capacity and efficiency. Aurizon Holdings started $180 million Hexham Train Support Facility which is near the Port of Newcastle, which would offer trains with fuel, water and other required supplies leading to a better operations efficiency with decrease in maintenance costs. AZJ finished the Stage 1 development of the Wiggins Island Rail Project at Central Queensland which would deliver a further 27 million tonnes per annum of coal to the new Wiggins Island Coal Export Terminal in Gladstone. The group along with its JV partner Qube Holdings got a Federal Government approval in June for developing Moorebank intermodal freight facility, located at south west of Sydney. Moorebank is expected to be among the major integrated warehouse rail terminal area in Australia post the development, and would connect to Port Botany, the busiest ports in Australia. Aurizon Holdings is also constantly reviewing proposal for the development of its multi-user rail and port infrastructure at Pilbara in Western Australia to unlock iron ore deposits. The group is conducting technical and commercial feasibility studies via its partners that include Baosteel Resources, POSCO and AMCI.

Development initiatives driving underlying EBIT performance (Source: Company Reports)

Strong Outlook: Aurizon Holdings is aiming to further enhance its productivity, customer service as well as costs efficiency in the range of $310 to 380 million for the next three years (by FY18) through its transformation program. As a result, Aurizon Holdings expects to reach a 70% of Operating Ratio by the 2018 financial year while intends to maintain a dividend payout ratio in the range of 70% to 100% of Net Profit after Tax. Meanwhile, the group reiterated its coal haulage outlook in the range of 210 to 220 million tonnes for 2016 fiscal year indicating its ongoing solid production of customers. AHJ expects its iron ore haulage at around 24 million tonnes and freight volumes at around 45 million tonnes for fiscal year of 2016. The group incurred a capex of $1.1 billion for fiscal year of 2015 as it delivered a high performance track maintenance equipment which has the ability to improve its network’s volumes coupled with a decrease in closure hours. AZJ expects to spend over $1.45 billion for fiscal year of 2016 and fiscal year of 2017, while forecasts its long term non-growth capital expenditure of over $500 million to $600 million per annum. Aurizon Holdings is targeting average return on invested capital to be over 10.5% for fiscal year of 2016 to FY 2018. Meanwhile, the company extended its ongoing market buy-back program to 107 million shares (which is 5% of its issued share capital as of November 2014) for further twelve months. The group bought back over 38.1 million shares till date under the program (as of December AGM report) which accounts over 36% of the overall buy-back capacity at an average price of $4.82. The group is continuing its buy-back of the remaining 68.9 million shares in the coming twelve months.

West Pilbara Iron Ore project’s potential cost position and sustainability (Source: Company Reports)

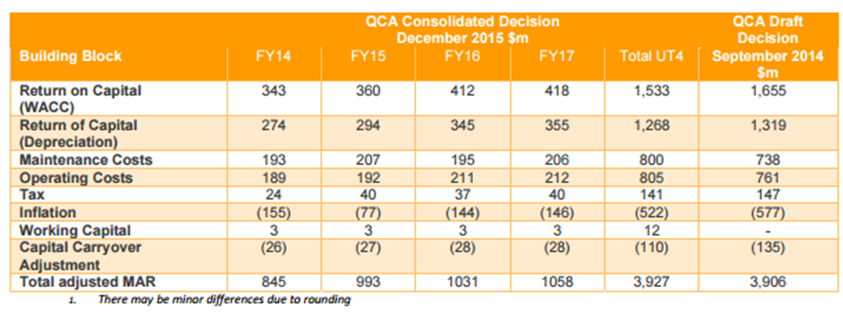

Delays on QCA finalization: Aurizon Holdings reported that the company is facing extended delays from Queensland Competition Authority (QCA) in the finalization of the 2014 Draft Access Undertaking (DAU). The group submitted its original UT4 DAU to the QCA on April 2013, while QCA recently reported a consolidated draft decision after which there would be an additional 10 weeks of consultation in advance to the new estimated final decision at April 2016. Based on the recent QCA report, Aurizon Holdings network tariffs and revenue for FY16 are related to the QCA draft decision regarding the Maximum Allowable Revenue. According to the Consolidated Draft Decision, the overall maximum revenue would be $3.927 billion during the period of the Undertaking, as compared to the QCA’s previous Draft Decision of $3.906 billion. The Consolidated Draft Decision also includes a weighted average cost of capital of 7.17%, which is in line with its earlier Draft Decision. Aurizon Holdings maintained its intention to resolve and implement UT4 by the end of FY16.

QCA consolidated decision (Source: Company Reports)

Stock Performance:

The shares of Aurizon Holdings fell over 8.74% (as of December 18, 2015) in the last four weeks impacted by the recent advice from Queensland Competition Authority (QCA) that AZJ and its customers would witness more delays in the finalization of the 2014 Draft Access Undertaking (DAU), disappointing the management as its network tariffs and revenue for fiscal year of 2016 are based on the QCA draft decision on Maximum Allowable Revenue (as of September 2014). On the other hand, AZJ is focusing on long term growth and was able to deliver decent FY15 performance despite volatile commodity market. The group recently made an agreement with NSW Ports to operate its Enfield Intermodal Logistics Centre (ILC) in Western Sydney and lease the land at the site. This agreement would further boost its intermodal business while AZJ already added over 175 new wagons into its national intermodal operations. The group started a new freight management technology to boost its customer service as well as enhance its business, and is well positioned to leverage the booming Australia’s domestic freight task opportunity which is forecasted to be triple by 2050 from its present size. Meanwhile, we believe that the recent correction offers an attractive entry opportunity for long term investors seeking for value stocks. AZJ generated 85.28% (as of December 18, 2015) returns since its IPO and rallied over 9.6% (as of December 18, 2015) in the last fifty two weeks. Aurizon Holdings is trading with a P/E of 17.3x while having an annual dividend yield of 4.9%. The transformation strategy, capital management initiatives and a probable upside with regards to the QCA draft final decision still appear to be catalysts for a longer-term momentum. We thus believe that AZJ stock has the potential for growth in long term and based on the foregoing, we give a “BUY” recommendation on the stock at the current price of $4.85

AZJ Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...