Company Overview: Audinate Group Limited is an Australia-based provider of professional audio networking technologies globally. The Company is engaged in developing both software and hardware to facilitate the delivery and management of audio over information technology (IT) networks, which improves audio quality, equipment interoperability and system flexibility. Its Dante solution is an uncompressed, multi-channel digital media networking technology, with near-zero latency and synchronization. Its products include Dante Analog Output Module, Dante Broadway, Dante Brooklyn II, Dante Brooklyn II PDK, Dante Controller, Dante Domain Manager, Dante HC, Dante PCIe-R Soundcard, Dante Ultimo, Dante Ultimo Product Development Kit (PDK), Dante Via, Dante Virtual Soundcard and Dante-MY16-AUD2. The Dante Analog Output Module is a Dante audio to analog audio adapter module, supporting one RJ45 Dante input, and one or two balanced analog outputs.

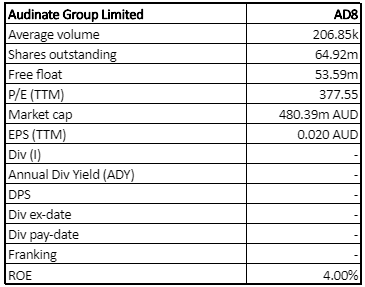

AD8 Details

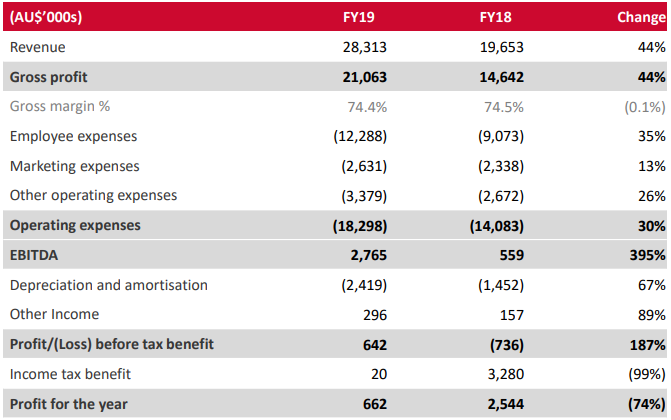

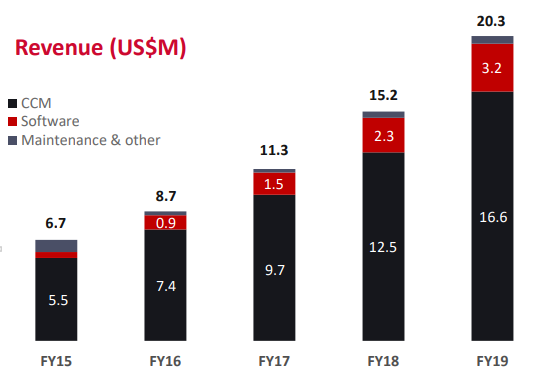

Decent Top-line growth in FY19: Audinate Group Limited (ASX: AD8) is engaged in the development and sale of digital Audio-Visual networking solutions. The company’s technology platform, Dante, distributes uncompressed digital audio signals over computer networks. Looking at the performance over the period covering FY16 to FY19, the company witnessed a CAGR growth of 33.5% in top-line with FY16 revenue amounting to A$11.9 million and FY19 revenue amounting to A$28.3 million. Revenue CAGR in terms of US dollars, for the period covering FY15 to FY19, is 27.6%. During the year ended 30 June 2019, the company generated revenue amounting to US$20.3 million, up 33.6% on FY18 revenue of US$15.3 million. In Australian dollars, revenue went up by 44.1%, from A$19.7 million in FY18 to A$28.3 million in FY19. The strong growth in revenue is attributable to further penetration of Dante-enable products in key market segments, that led to a material increase of 395% in EBITDA during the year. EBITDA for the period was reported at A$2.8 million, as compared to 2018 EBITDA of A$0.6 million. Operating cash flow for the period was reported at A$3.6 million, up 249% on 2018 cash flow of A$1.0 million. NPAT for the period amounted to ~A$0.7 million, representing an improvement of ~$0.6 million on the prior year after adjustment of one-off tax benefit received in FY18. During the year, the company saw an increase of 30% in operating expenses to A$18.3 million. The expenses primarily pertained to investment in people that included 19 new roles related to sales and engineering, costs associated with the company’s new Sydney office and the second year of long-term incentive expenses.

Financial Summary (Source: Company Reports)

Over the period covering FY15 to FY19, the company reported continued growth in revenue, which stood at US$20.3 million in FY19 as compared with revenue in FY15 at US$6.7 million. The increase in revenue during the current year is attributable to a 29% increase in shipments of Dante chips, cards, modules and software.

Going forward, with record of achievement and growing revenue in the last few years along with the competitive landscape in terms of networked audio products, continued expansion and investment in R&D, consistent product upgradation, etc., the growth trajectory is expected to be continued in FY20.

Revenue Growth (Source: Company Reports)

Significant Expansion of Product Offering: As mentioned above, revenue growth in FY19 was supported by the increased scale of operations with respect to Dante-enabled products. As at 30 June 2019, the company had 2,134 Dante enable products available for sale, representing a 30% increase on 1,639 products in the previous year. The number of Original Equipment Manufacturers shipping Dante enable products increased by 22% to 270 as at 30 June 2019. Two launches in FY18 that include the Dante Domain Manger and a range of Dante AVIO adapters, exceeded the company’s expectations for FY19.

In June 2019, the company also released Dante AV Module and introduced Dante AV Product Design Suite, making its debut into the video market. In July 2019, the company secured a first design win and the Dante AV Product Design Suite is expected to be shipped to OEMs by the end of CY19. In the month of June, the company also launched two new software products, including Dante Application Library™ and Dante Embedded Platform™.

Impact of One-off Tax Benefit: During the year, the company recorded profit after tax amounting to ~$0.7 million as compared to $2.5 million in FY18. Profit for the previous year was inclusive of a one-off tax impact worth $2.4 million.

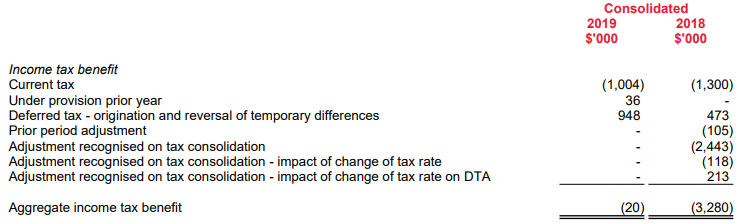

In FY18, the company and its wholly-owned Australian subsidiaries formed an income tax consolidated group under the tax consolidation regime, that results in a deferred tax asset being recognised.

Deferred Tax Asset Explained: Deferred tax asset forms part of a company’s financial statements at the year-end and affects the income-tax payment for that particular year as well as the years ahead. In FY18, Audinate Group Limited and its wholly-owned Australian subsidiaries formed an income tax consolidated group under the tax consolidation regime, which resulted in a deferred tax asset being recognised. Aggregate income tax benefit for FY18 was reported at $3.28 million. The break-up of the tax benefit can be seen in the image below.

Income Tax Benefit (Source: Company Reports)

Recent Updates:

(a) Change of Address: The company recently released an announcement regarding the change of registered office and principal place of business to Level 7, 64 Kippax Street, Surry Hills NSW 2010.

(b) Shareholding Update: As per another update, it was notified that AustralianSuper Pty Ltd ceased to be a substantial shareholder of the company since 11 July 2019.

(c) Share Purchase Plan: In July 2019, the company announced the completion of its Share Purchase Plan, which was oversubscribed with applications exceeding A$37 million. Earlier, the company has also reported an oversubscribed placement worth A$20 million to new and existing institutional investors. The funds received through the placement and the Share Purchase Plan will support global sales penetration, expansion of product initiatives and provide additional flexibility to the company’s balance sheet.

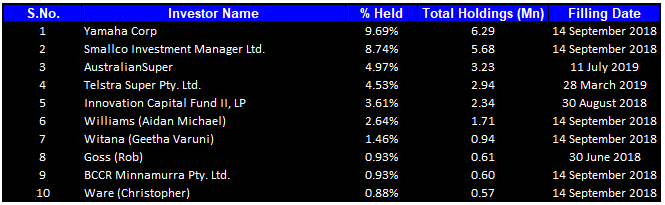

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 38.38% of the total shareholding. Yamaha Corp holds the maximum interest in the company at 9.69%, followed by Smallco Investment Manager Ltd holding 8.74% of the outstanding shares.

Top Ten Shareholders (Source: Thomson Reuters)

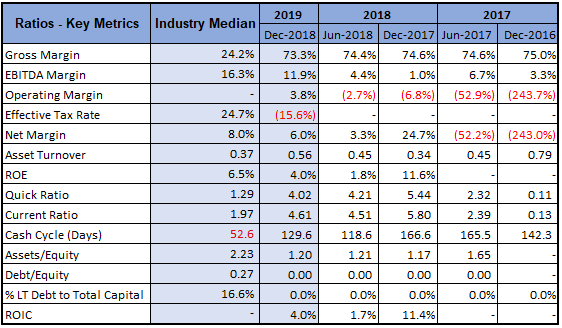

Key Metrics: In 1HFY19, the company had an EBITDA margin of 11.9% as compared to 1HFY18 margin of 1.0%. The company’s gross margin during the period stood at 73.3%, which is much higher than the industry median of 24.2%. Current ratio for the period stood at 4.61x in comparison to the industry median of 1.97x.

Key Metrics (Source: Thomson Reuters)

Key Risks: Based on its activities, the company is exposed to a variety of financial risks, including market risk, credit risk and liquidity risk. (a) Market Risk – This includes the impact of foreign exchange movement, (b) Credit Risk – This refers to the risk associated with a counterparty defaulting in fulfilling its contractual obligations resulting in financial loss to the company, and (c) Liquidity Risk is associated with the company’s ability to pay debts as and when they become payable.

Outlook: The company’s historical US dollar revenue growth has been in the range of 26% to 31%.The company expects to continue the trajectory with a focus to grow the shareholder’s value in the long run. In terms of revenue split, the company expects to revert to historic H2 bias in FY20 while focusing on revenue growth through design wins for its newly launched products. In FY20, the company will commence investing to double the engineering and R&D functions over the next two years. The company will focus on developing next-generation Dante audio and video software implementations.

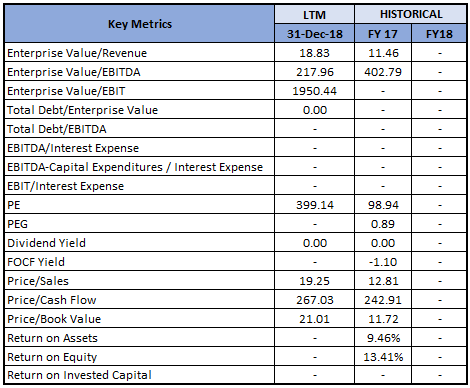

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: EV/EBITDA Multiple Approach (NTM):

(4).png)

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock of the company generated returns of -0.67% over a period of 1 month. In FY19, the company witnessed strong growth in revenue backed by the expansion of its Dante product offerings that included the introduction of new products and applications. FY19 revenue for Dante Domain Manager & adapters exceeded the company’s expectations. The increase in revenue drove EBITDA, during the year to remarkable levels in comparison to the previous year. The company further aims to drive design wins in FY20 to generate the revenue pipeline for FY21 and beyond. During the year, the company expanded its sales and support teams with the opening of sales offices in Germany, Japan & China along with the addition of additional sales resources in the USA and EMEA. The period also saw continued investment in research & development. The company used the growth in gross margin to fund new product initiatives making innovation a core to its business. With the above developments in place, the company expects to maintain its historical revenue growth trajectory and deliver shareholder’s value in the long run. Furthermore, AD8 is continuously working on the acceleration of product development and has the foundations in place to support the software transition of the Audio-Video industry in the medium term. In the coming financial year, the company is expected to bring further advancements through increased investment in R&D functions and a well-placed business infrastructure platform. It is focused on expanding its addressable market with addition of video & software products. With the above scenario in place, the company seems well-positioned to drive innovation throughout the AV industry and support its long-term growth objectives. Considering the decent performance in FY19, rapid global expansion and the ongoing plans for product developments, the company is well-placed to drive shareholder returns in the near future. Based on the above factors, we have valued the stock using EV/EBITDA based relative valuation method and have arrived at the target price of around high single-digit upside (in percenteage term). Lately, we have covered the stock at a price of $7.470 with an advice to watch in the absence of catalyst and awaited FY19 results. With the decent set of numbers for FY19, justifying the valuations, thus, we give a “Buy” recommendation on the stock at the current market price of $6.970 as on 23 August 2019 (down 5.811% on 23 August 2019).

.png)

AD8 Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...