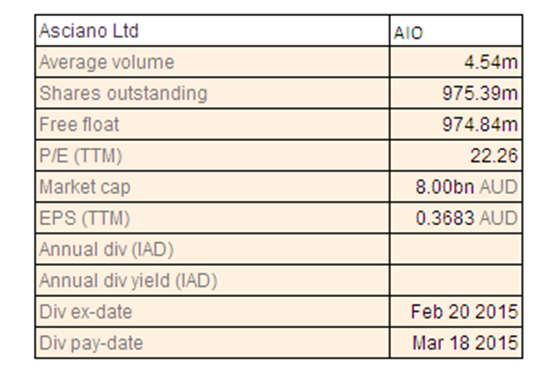

AIO Details

Improved bottom line despite top line pressure: Asciano Ltd (ASX: AIO) revenues fell by 3.9% year on year (yoy) to $3.8 billion in 2015 fiscal year, impacted by the tough market conditions in Australia. However, AIO was able to deliver an increase of 9.7% yoy in underlying EBIT to $790.2 million driven by solid coal rail haulage, wherein the Pacific National business rose 5.8% in net tonne kilometers while container lifts in Patrick container terminals business also performed well. However, Intermodal, Bulk & Auto and Logistics generated softer volumes. Nonetheless, Asciano’s underlying Net Profit after Tax surged by 18.6% yoy to $414.7 million. The group achieved an additional of $143.7 million in savings during the period driven by its business improvement program (BIP) efforts. Asciano aimed to achieve over $150 million cost take-out through its BIP. However, the BIP generated over $143.7 million in benefits during the FY15 fiscal year resulting in a total of $258.7 million over the last four years. Asciano estimates to exceed its target of $300 million by up to 10% by 2016 financial year.

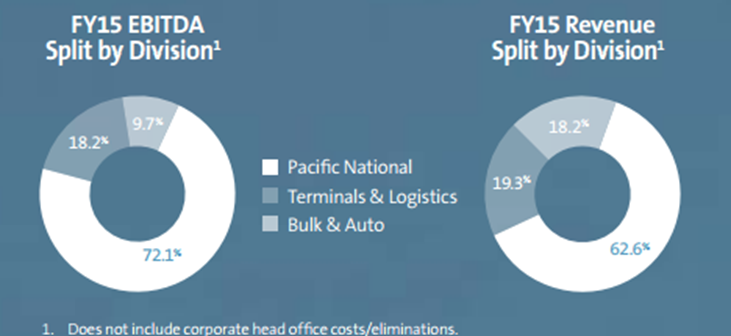

Divisional highlights (Source: Company Reports)

ACCC concerns over Brookfield Infrastructure’s Bid: Brookfield Infrastructure Partners Limited recently made an offer to acquire 100% of the issued capital of Asciano for an implied value of $9.15 per Asciano share, leading to an enterprise value of around $12 billion. Moreover, the group estimates to pay a total franked special dividend of up to $0.90 per share to shareholders as part of the agreement, in case the transaction proceeds as well as the approval of the Australian Taxation Office is received. Management also recommended its shareholders to accept this offer. On the other hand, Australian Competition and Consumer Commission (ACCC) raised concerns over the proposed acquisition of Asciano by Brookfield Infrastructure. According to ACCC, the vertical integration of the two companies would decrease the competition for the supply of above rail haulage services in WA and Queensland. Asciano reported that it would consider the influence of the ACCC’s process on the transaction. However, receiving ACCC approval for the bid might be a challenge to the group.

Qube Holdings’ interest in Patrick business: Qube Holdings acquired an aggregate interest of 19.99% of the shares in Asciano Limited with the help of its two co-investors, Global Infrastructure Partners and Canadian Pension Plan Investment Board. Qube has funded a 6.3% interest in Asciano by way of a total return swap with UBS. Meanwhile, Qube made this transaction to help decide the ownership of Australian terminal assets of Asciano’s first class. Combination of Qube with Patrick Containers Terminals business and many small number of assets in the bulk, automotive and general stevedoring businesses owned by Asciano (Patrick Businesses) would deliver the potential to generate a solid value. Qube is interested in the Patrick Businesses of Asciano, as the same would open more opportunities which would in turn boost Qube’s shareholder value. Qube also intends to enhance Patrick terminal business by managing and developing the Patrick container terminals businesses, generating cost efficiencies at the Patrick terminals as well as implementing and improving terminal automation and terminal operating systems. However, Qube is not supporting the present Brookfield’s scheme proposal.

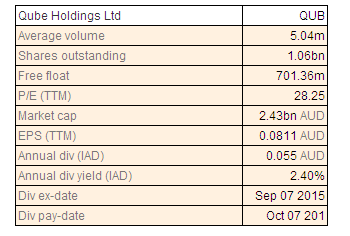

QUB Dividend Details

Asciano’s Balance sheet position: The group enhanced its balance sheet during 2015 fiscal year with its leverage (net debt to EBITDA ) decreasing to 2.7 times, which is on track with its estimated range of 2.5 times to 3 times. Asciano’s interest cover also enhanced to 5.5 times from 5.3 times in prior corresponding period (pcp) as well as much above as compared to its estimation of a minimum of 3.5 times. Asciano also enhanced its ROCE to 11.4% during the period against 10.7% in prior corresponding period. ROE rose to 10.9% from 9.5% in pcp. Asciano issued $350 million of 10-year unsecured fixed rate medium term notes, during May 2015 and diverted the funds to repay its debt maturing in September 2015. Meanwhile, the group incurred a capital expenditure of $566.9 million in the fiscal year of 2015, which is lower than the bottom end of the estimate range of $600-700 million and much lower than total spend of $753.7 million in FY14. Asciano upgraded to strategic operational sites during the period which includes its Sydney and Melbourne rail freight terminals, a new pre-delivery inspection facility at Webb Dock as well as the acquisition and commissioning of a floating marine facility in Dampier, Western Australia. Asciano expects its FY16 capital expenditure to be in the range of $390-440 million, which is on track with its earlier estimates.

.png)

Capital expenditure outlook (Source: Company Reports)

Conclusion: AIO’s board is in support of the Brookfield offer in the absence of any superior proposal while QUB has taken a large stake in AIO and is non-supportive of the offer. AIO now plans to evaluate the implications of QUB’s emergence as its biggest shareholder. At the same time, QUB under its consortium is considering about approaching AIO with an alternative offer and undertaking an equity raising with regards to an alternative proposal. On the other hand, Brookfield is set to report its 3Q results along with which it is expected to throw some light on the saga. Meanwhile, AIO informed that ACCC’s final decision is expected on 17 December 2015. The issues of course focus on the vertical integration of AIO’s rail operations and Brookfield’s ownership of Dalrymple Bay Coal Terminal in QLD and Brookfield Rail. All in all, QUB has created a blocking stake which seem to have enough potential to kill the Brookfield offer. Hence, it will be good to wait and watch the outcome which may or may not bring all the parties to term. As of now, AIO stock is trading close to its 52-week high price and at a high P/E ratio of 31x.

AIO Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...