Company Overview - Ardent Leisure Group is an Australia-based company, which invests in and operates leisure and entertainment businesses in Australia, New Zealand and the United States. The Company operates through six segments: Family entertainment centers, which include around 20 main event sites in Texas, Arizona, Georgia, Illinois and Oklahoma, the United States; Bowling centers, which include around 49 bowling centers and four amusement arcades in Australia and New Zealand; Marinas, which includes seven d'Albora Marina properties located in New South Wales and Victoria; Theme parks, which include Dreamworld and WhiteWater World in Coomera, Queensland and the SkyPoint observation deck and climb in Surfers Paradise, Queensland; Health clubs, which include around 76 centers in Queensland, New South Wales, Victoria, South Australia and Western Australia, two independent Hypoxi studios in New South Wales, and one independent Hypoxi studio in Ballantyne, North Carolina, and Other.

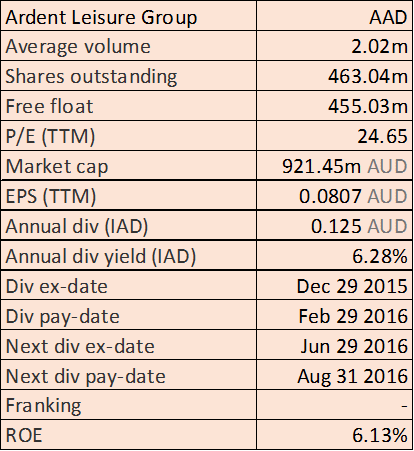

AAD Details

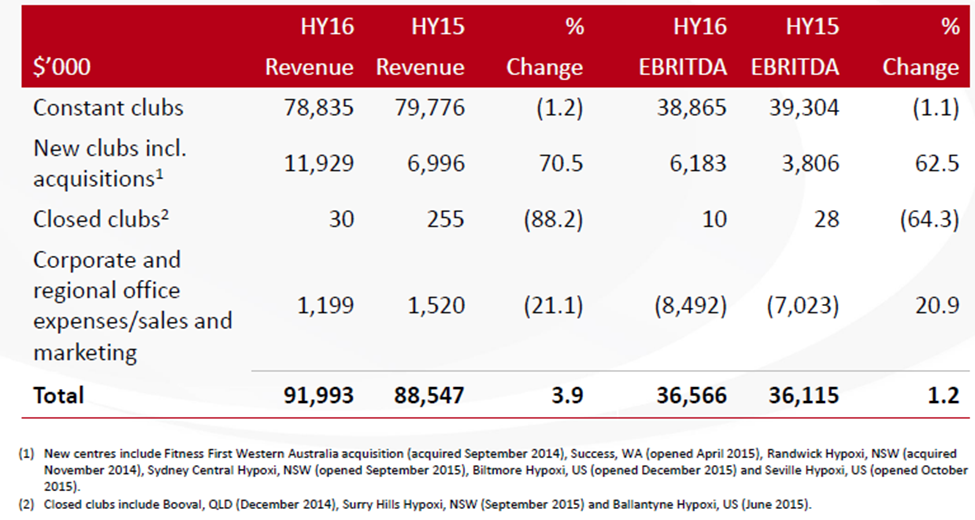

d’Albora Marinas portfolio sale process: Ardent Leisure Group (ASX: AAD) has earlier stated certain objectives to generate maximum value to its shareholders, which included the sale of d’Albora Marinas. On the other hand, recently the group reported that they need to make some capital enhancements before they proceed with the sale process of the d’Albora Marinas. This update from the group has led to the stock correction of over 9.95% in the last four weeks (as of June 24, 2016). d’Albora Marinas has seven high profile marinas, with three in Sydney Harbour, two adjacent to the Melbourne CBD coupled with more two at the popular leisure destinations of Nelson Bay and Akuna Bay, north of Sydney. With this sale, Ardent intends to further strengthen their focus on its core Main Event Family Entertainment Centres in the USA. On the other side, the group’s Marinas division business has not been performing well with revenue and EBITDA falling by 2.3% yoy and 8.6% yoy, respectively, during the first half of 2016. This impact is due to several factors like Berth and fuel revenueimpact during redevelopment of the Spit (NSW) marina; building construction impact on Victoria Harbour (VIC) berthing occupancies and costs associated with a new center at Nelsons Bay (NSW). But, overall berthing occupancy was maintained at 82% during the first half of year 2016.Management expects a better business for next year as these factors’ impact would decrease.

Marinas portfolio (Source: Company Reports)

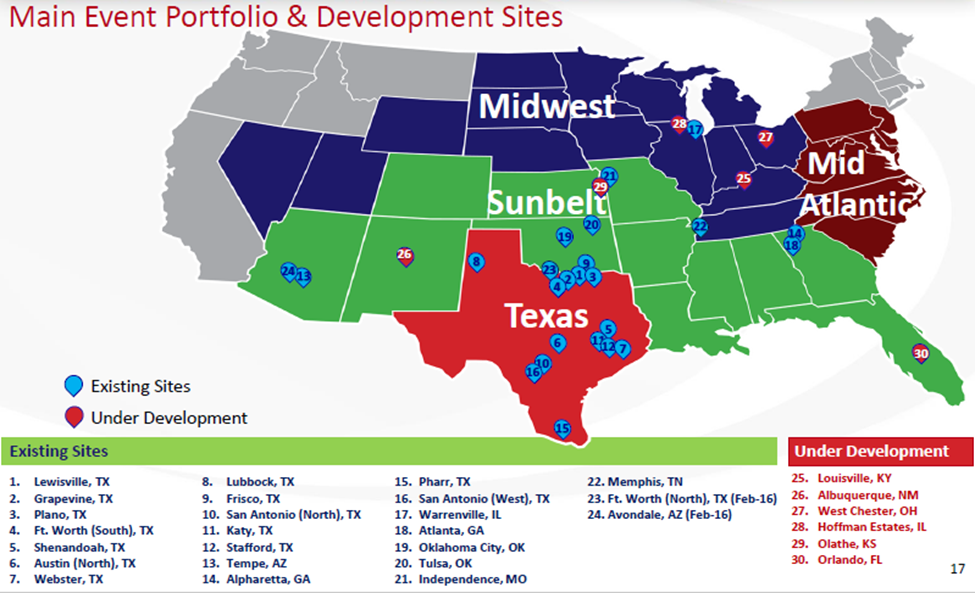

Solid performance of its core, Main Event business: The group’s main event business accounts a major part, which comprises 29% of its first half of 2016 EBITDA. Main event revenues surged over 48.2% on a yoy basis to $105 million. Meanwhile, the group’s centers, generated an average annual EBITDA return on investment of over 35% opened from 2007. Ardent is aggressively expanding its Main Event portfolio business and delivered two centers- Independence, MO and Memphis, TN by end of the first half of 2016. The group is planning to open five new centers by second half of FY16 having an overall of 27 centers by end of FY16, which is a 35% rise against fiscal year of 2015. Ardent intends to open at least eight sites by FY17, wherein three are under construction sites at Olathe (KS), Hoffman Estates (IL) and Orlando (FL). Consequently, the group estimates 30% rise as compared to fiscal year of 2016. Meanwhile, Ardent’s Main Event division got over US$33 million via two sale and leaseback transactions in the first half of 2016.

Main event portfolio (Source: Company Reports)

Efforts to improve Health Clubs business: The group’s health clubs business revenue rose only 3.9% on a yoy basis to $92 million but the division’s EBITDA fell over 8.1% yoy to $13.3 million in the first half of 2016. Accordingly, management reported that they are undertaking solid initiatives to enhance its Health Clubs business and accordingly progressing its 24/7 conversion program, expanding equipment, and leading digital initiatives. As a result, the group’s EBITDA for the second quarter of 2016 improved by 20.9% on a yoy basis to $6.8 million which is a major trend reversal as compared to the first quarter of 2016. This rise was also boosted by the group’s solid membership growth of over 8,300 members (for the entire first halfof 2016).Premium memberships accounted over 45% of all sales while the group forecasts an EBITDA rise of over 10% in the segment during the second half of 2016. The group has converted 37 clubsto 24.7 operationsduring the first halfof 2016 which generated over 25.8%rise in sales and 15.7% cutin attritionduring the first halfof 2016. Ardent estimated more than 45 converted clubs by June 2016. The group estimates its second half of EBITDA earnings to be in the range of $15m to $16m for the division, which is a rise of over 10% against pcp. With the growing Australian fitness industry, whichexpanded to 14.8% in 2015 against 11.7% in 2011, the group’s Goodlife is well positioned to leverage the upcoming industry growth.

Health Clubs performance in first half of 2016 (Source: Company Reports)

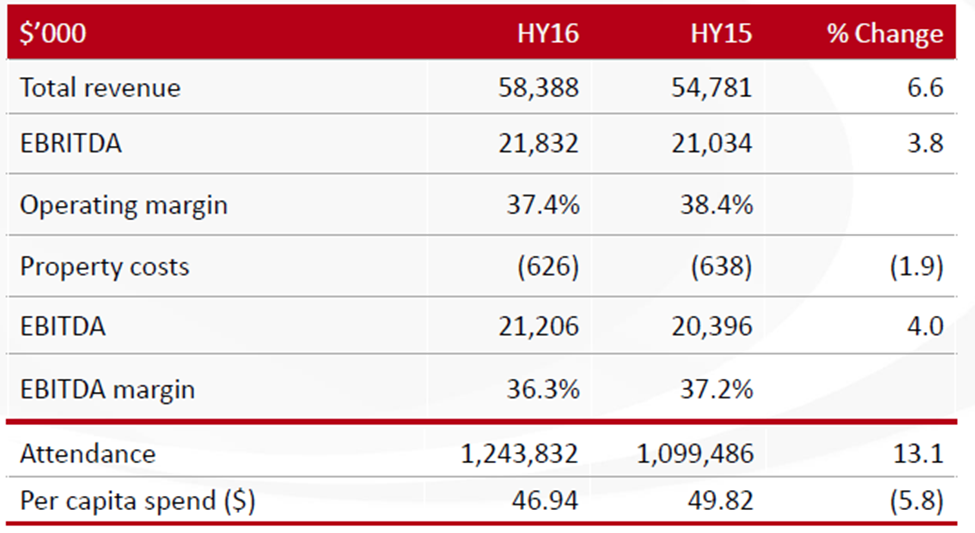

Focusing on Dreamworld Brand: The group’s theme parks division generated a revenue rise of 6.6% on a yoy basis to $58.388 million on the back of solid demand from China while EBITDA rose by 4.0% to $21.2 million in first half of 2016. Ardent is making solid efforts to offer a unique experience and gain competitive edge by developing distinct attractions. Management reported that they are heavily focusing on “Dreamworld” brand to enhance ticket revenue and in?park spend. As a part of its recent strategic objectives, the group intends to develop more unique attractions at Dreamworld to appeal the mass market entertainment experiences, and leverage the rising tourism opportunity in the Gold Coast, especially from Asia and during the 2018 Commonwealth Games. Moreover, in the coming years the group expects its US assets to surpass its Australian businesses and is accordingly taking steps to rebalance its portfolio. The SkyPointbusiness is doing well driven partly by the international market. The group is renovating its Dreamworld, Tiger Island.

Theme park performance in first half of 2016 (Source: Company Reports)

Bowling highlights: The overall revenuefor bowling division rose by 11.6%on a yoy basis to $67.4 million in the first half of 2016 while EBITDA surged by 20.5% on a yoy basis to $11.0 million. Constant centers revenue rose3.1%on a yoy basis driven by amusement gamesinvestment coupled with ongoing innovation in food and beverage.The group expanded two new venues to itsportfolio -Kingpin Darwin, NT and Playtime Penrith, NSW.Ardent has always been focusing on enhancing its customer booking experience. Management reported that their AMF and Kingpin venues would continue to drive revenues via better Food and Beverage menus, enhanced amusement games and better entertainment offerings. But, the group is shifting from its traditional AMF branded bowling centers into multi?attraction family entertainment venues on par with its new facility in Darwin. Accordingly, for the coming three years the Group intends to exit earlier, less returning sites and focus only on growth via selective development from its present assets like Kingpin at Crown Casino, coupled with the acquisition of new sites for high returning amusement games arcades. The groups Kingpin center would resume from fourth quarter of FY16 after refurbishment.

Bowling performance in first half of 2016 (Source: Company Reports)

Strong dividend yield: The shares of AAD have been volatile this year and fell over 13.1% during this year to date (as of June 24, 2016) while showing rise of about 2% on June 27, 2016. On the other hand, the group is focusing on its core Main Event business and intends to expand the national roll-out in the US to 35 centers by 30 June 2017. The group estimates a low single digit revenue growth from constant centers on a long term basis for Main Event business. With the transformation initiatives of its health clubs business, the group would generate further membership growth even for the second half. For its Bowling business, management intends to further develop and acquire stand-alone amusement facilities, while quitting its underperforming legacy centers. Despite the delay in pursuing d’Albora Marinas portfolio sale, this sale would strengthen AAD’s capital position. We believe investors need to leverage the correction in the stock as an entry opportunity. Moreover, AAD has a solid dividend yield. We give a “Buy” recommendation on the stock at the current price of $2.00

AAD Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...