Kalkine has a fully transformed New Avatar.

Company Overview: Ansell Limited (ASX: ANN) is engaged in manufacturing protective industrial and medical gloves. The company has transformed itself from Australian rubber latex products manufacturer to a highly improved safety solutions provider, globally. Ansell’s expertise, innovative products, trusted brands and advanced technologies help to build customer confidence by providing solutions for new needs. The company manufactures more than 10 billion gloves every year, providing security services to >25 industries.

.png)

ANN Details

.JPG)

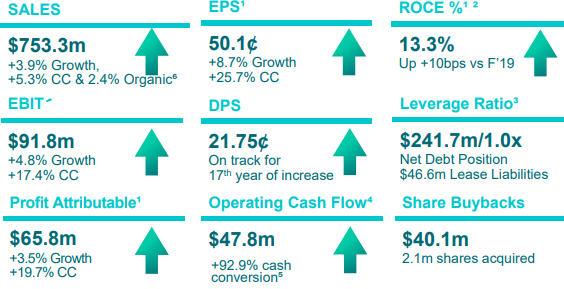

ANN Rides on Continuous Momentum in HGBU and IGBU Segment: Ansell Limited (ASX: ANN) is a top supplier of improved health and safety protection solutions that boost human well-being. Ansell’s products and services encourage confidence in people and aid businesses and workers to operate better. As on 25 March 2020, the market capitalization of the company stood at ~A$3.04 billion. ANN in its 1HFY20 results for the period ended 31 December 2019, reported revenues of US$753.3 million, up 3.9% year over year on a reported basis and 5.3% on a constant currency basis. The increase was aided by 2.4% organic revenue growth on account of continued Healthcare GBU (HGBU) momentum of 3.4% and improved Industrial GBU (IGBU) performance of 1.3% on year over year basis. Statutory EBIT increased a whopping 51.2% year over year and came in at US$91.8 million. The improvement in EBIT margins was on the back of benefits from Gross Profit After Distribution Expenses (GPADE), primarily aided by the transformation program, sales mix and lower raw material costs, which more than offset FX impacts and Selling General & Administrative costs.

The company remains in a healthy and a steady position and is anticipating organic growth in the coming years. For FY20 & beyond, the company remains on track for margin expansion aided by commercial and operational efficacy. Further, the company is expecting a positive impact from the Transformation program and remains focused on opportunities for further optimisation to enhance customer service. The company continues to invest in ERP, supply chain & digital technology. Further, it expects a continuation in delivering robust cash conversion and leverage on growth opportunities in key segments in order to drive productivity through automation.

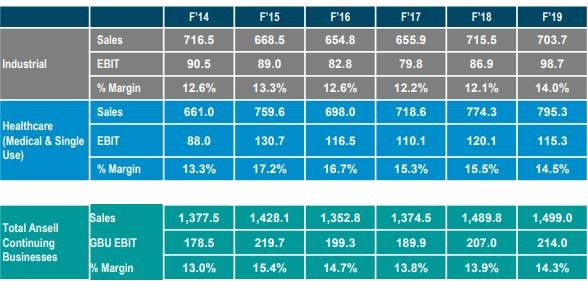

ANN witnessed a compound annual growth rate of 1.7% in revenue in the time span of FY14-FY19. The company has adopted four key strategies to make its business strong and healthy. This includes focusing on innovation, emerging market development, leveraging industry-leading and trusted brands, and lastly via partnerships with leading distributors. Further, the company also made significant investments in digital marketing to leverage artificial intelligence (AI) based solutions. As per the reports for FY19, more than 20% of Ansell’s total sales are now sourced through a variety of digital channels.

Cash flow from operations grew at a CAGR of ~9.06% over the time span of FY15-FY19. The company further aims to generate significant cash from operations and maintain a healthy balance sheet. The company remains on track to deliver significant value to its shareholders through the continuous payment of dividends, share buy backs and investment in new and latest know-how. ANN declared an interim dividend of US 21.75 cents per share in 1HFY20.

Segment History- Continuing Businesses (Source: Company Reports)

1HFY20 Performance: During the period, revenue stood at US$753.3 million, increasing 3.9% year over year. Organic revenue for the period increased ~2.4% year over year. Growth amplified on the heels of HGBU momentum (up 3.4%) and improved IGBU performance (up 1.3%). Robust surgical performance and solid performance from Life Science aided growth in HGBU. IGBU increased as EMEA showed signs of improvements, with continuous momentum in APAC region, which more than offset the decrease in Americas. EBIT stood at US$91.8 million, up 51.2% year over year. In 1HFY20, profit stood at US$65.8 million, up 3.5% year over year and 19.7% increase on a constant currency basis. Earnings per share for the period came in at US 50.1 cents per share, as compared to US 28.6 cents per share in pcp. EPS was positively impacted by higher sales and GPADE margins combined with lower tax & share buyback, thereby maintaining a healthy balance sheet for further growth. Selling, general & administration expenses increased 10% year over year to US$165.4 million, which includes ~US$7 million impacts from Ringers & Digitcare and timing of biennial events.

1HFY20 Results (Source: Company Reports)

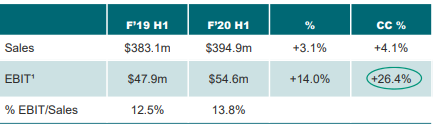

Segmental Performance in 1HFY20: During the period, total revenues with respect to Healthcare GBU came in at US$394.9 million, as compared to US$383.1 million reported in 1HFY19. Segmental EBIT went up 26.4% on constant currency basis and came in at US$54.6 million. Healthcare GBU witnessed growth in revenues and EBIT, primarily on the back of increase in emerging markets such as China, India and OLAC strong performers. HGBU margins primarily benefited from the product mix, lower raw material costs, enhanced manufacturing plant performance and pricing initiatives. Negative FX movement impacted EBIT margins by 110 basis points. Coming to Industrial GBU, revenues and EBIT stood at US$358.4 million and US$44.4 million, respectively. The figures increased by 6.5% and 11% year over year, respectively, on a constant currency basis.

HGBU (Source: Company Reports)

.png)

IGBU (Source: Company Reports)

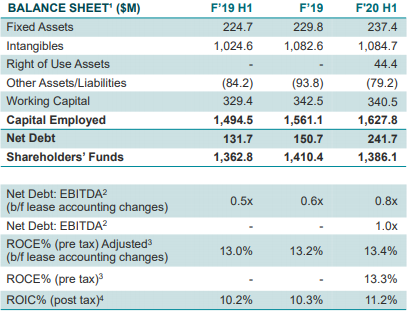

Balance Sheet & Cash Flow Detail: At the end of 31 December 2019, the company’s net debt stood at US$241.7 million, as compared to US$131.7 million at the end of 1HFY19. The increase in net debt was on the back of a change in the new lease accounting standard. Cash at bank and short-term deposits at the end of the period stood at US$384.5 million, as compared to US$414.9 million at the end of 1HFY19. Capital employed at the end of 1HFY20 stood at US$1,627.8 million, as compared to US$1,494.5 million at the end of 1HFY19. Operating cash flow for 1HFY20 stood at US$47.8 million, with robust cash conversion of 92.9%. ROCE in 1HFY20 stood at 13.3%, up 10 bps.

Balance Sheet (Source: Company Reports)

Coronavirus Update: The company has taken necessary measures to keep China safe and protected in the period of uncertainty due to COVID-19 outbreak. In doing so, ANN has been engaged in delivering Personal Protective Equipment (PPE) to keep people safe. It has also been working carefully with the Chinese authorities to manufacture and distribute protective clothing as per the requirements. In doing so, the company is fast tracking its regulatory and import process in order to accelerate supply. Employees of ANN in China have maintained the production of PPE to cope with the crisis.

Recent News:

(a) On 25 March 2020, the company announced an on-market buy-back of a total of 1.94 million shares. The value of shares bought back is around $53.93 million.

(b) On 23 March 2020, the company stated that Vanguard Group, a substantial holder of the company, has increased its voting power from 5.002% to 6.007%.

(c) On 9 March 2020, the company announced a partnership with Modjoul, a data-driven IoT platform and analytics company to build hand protection solutions focusing on motion-ergonomics.

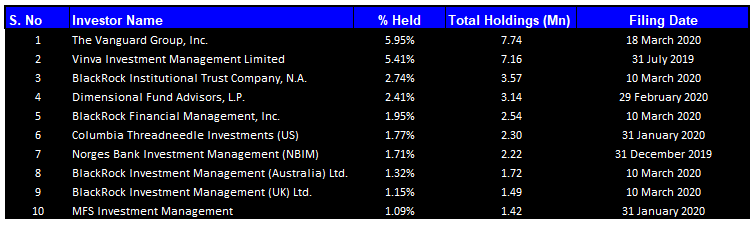

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 25.49% of the total shareholding. The Vanguard Group, Inc. is the entity holding maximum shares in the company at 5.95%. Vinva Investment Management Limited is the second-largest shareholder, with a holding of 5.41%.

Top Ten Shareholders (Source: Thomson Reuters)

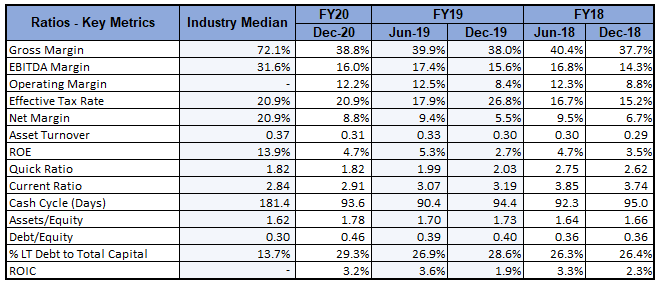

Key Metrics: In 1HFY20, the company had a gross margin of 38.8%, which is higher than 1HFY19 margin of 38% and 1HFY18 margin of 37.7%, representing decent fundamentals. EBITDA margin stood at 16%, higher than 1HFY19 margin of 15.6% and 1HFY18 figure of 14.3%.

Key Metrics (Source: Thomson Reuters)

Outlook: Going forward, the company is expecting to generate organic growth of approximately 3% to 5% per annum. EPS growth is expected to be in the range of 5% to 10% per annum. Further, the company expects ROCE to improve to 14%-15% by FY20. The company is expecting to have minimal effect on its net financial performance from the Coronavirus outbreak. The company expects to stabilise in FY20 against the impact of uncertainties around global economies and trade. Owing to a strong pipeline and strategic initiatives taken by the company, it maintained its FY20 EPS outlook to be in the ambit of US 112¢ to 122¢. The EPS guidance includes a positive impact of EBIT growth from various business initiatives including transformation program, pricing, lower raw material costs & mix. Further, the company remains on track to continue with its buyback program. It also strives to stay focused on executing a differentiated business proposition, which in turn will improve shareholder value.

Growing through organic revenues remains an important part of the company’s growth prospects. Further, increased investments in healthcare technologies, artificial intelligence and digitalization, are likely to support the company’s growth trajectory. This is expected to lead in cost productivity, thus supporting both the top line and margins. The company continues to witness growth opportunities in few regions with the IGBU business set to benefit from new product sales initiatives, emerging market growth and ongoing benefits from the Transformation Program.

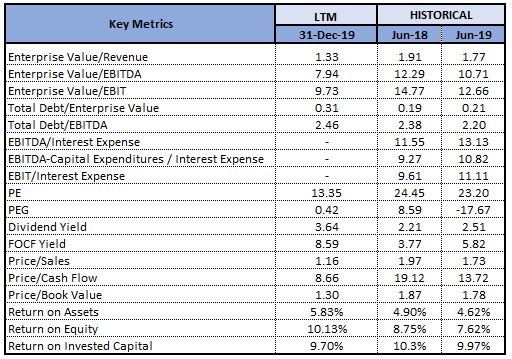

Key Valuation Metrics (Source: Thomson Reuters)

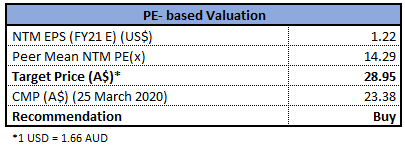

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation

Price to Earnings Multiple Based Relative Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company generated a negative return of ~16.8% in the past six months. In 1HFY20, the company delivered a decent result, driven by positive contributions from the HGBU and IGBU segments. The company expects to thrive further on the back of population trends, increasing patient expectations and geographical expansion. Considering the above factors, we have valued the stock using Price to Earnings based relative valuation method and have arrived at a target price with an upside of lower double-digit (in % terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $23.38, down 0.806% on 18 March 2020.

.png)

ANN Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...