Kalkine has a fully transformed New Avatar.

Company Overview: Amcor plc is a packaging company. The Company’s segments include Flexibles and Rigid Plastics. The Company offers a range of packaging related products and services, including packaging for beverages, food, healthcare, and personal and home care, tobacco and industrial applications. The Flexibles consists of operations that manufacture flexible and film packaging in the food and beverage, medical and pharmaceutical, fresh produce, snack food, personal care and other industries. The Rigid Plastics consists of operations that manufacture rigid plastic containers for a range of predominantly beverage and food products, including carbonated soft drinks, water, juices, sports drinks, milk-based beverages, spirits and beer, sauces, dressings, spreads and personal care item and plastic caps for a variety of applications.

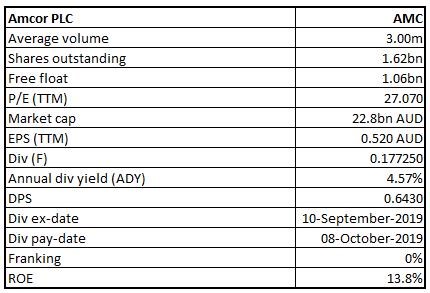

AMC Details

Decent Performance in FY19: Amcor PLC (ASX: AMC) is a large-cap packaging company with the market capitilisation of circa $22.8 Bn as of 21 October 2019. It develops and produces rigid and flexible packaging for various food, beverage, pharmaceutical, medical-device, home- and personal- care, and other fast-moving consumer end markets. The company released its annual report for FY19 wherein it stated that both of its reporting segments, i.e., Rigid Packaging and Flexibles posted good results, due to a combination of higher sales and strong rigor on the operating costs. On June 11, 2019, the company wrapped up the acquisition of Bemis Company Inc. Resultantly, AMC is now a global leader when it comes to consumer packaging, and it has even greater attraction for the talent, global reach, scale as well as technical capabilities. We presume that synergistic acquisition with Bemis will support top-line growth of the company. Further, AMC’s listing on the New York Stock Exchange and inclusion in S&P 500 increased the optionality and liquidity for shareholders and provide access to a larger pool of potential investors and capital.

The company is well-placed for further growth at the back of robust financials, unique combination of talented people, differentiated capabilities, scale, and strong footprint across the globe. It serves customers, which are in stable and defensive categories such as healthcare and food, which are resilient to economic volatility. Apart from having an unmatched global footprint, the company’s operations and supply chains are mainly local, which reduces reliance on complex international trade. The above-stated characteristics drive robust and consistent cash flows, which create value to the shareholders in 3 ways, i.e., dividends, organic earnings growth and acquisitions and/or buy-backs.

There are expectations that robust financial profile, global reach, and decent liquidity might act as tailwinds for long-term growth. With respect to Bemis acquisition, the greater scale, attractive end markets, and best-in-class capabilities might help the overall long-term performance of the company.

.png)

Full Year Adjusted Financial Results (Source: Company Reports)

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Amcor PLC:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Key Metrics: Net margin stood at 4.6% in FY19 while its gross margin came in at 19%. In FY19, the company’s RoE stood at 13.8%. When it comes to the liquidity levels, the company seems to be having decent footing as its current ratio stood at 1.15x in FY19, which reflects an increase from FY18 figure of 0.72x. Therefore, it can be said the company’s liquidity position to meet its short-term obligations has improved. Additionally, it can be said that AMC would be able to make deployments towards the strategic business activities, which might act as long-term growth catalysts. The company’s Debt/Equity ratio stood at 1.09x in FY19, which is substantially down from the prior year figure of 7.74x, and it can be said that its balance sheet is less leveraged in FY19 as compared to the prior year and is more stabilised. The lower debt on the balance sheet generally reflects stability, and the company can focus on its growth prospects.

.png)

Key Metrics (Source: Thomson Reuters)

AMC Possesses Capacity to Drive Shareholders’ Returns: The company added that 2019 was a transformative year for the company, which was marked by the completion of Bemis acquisition and listing on the New York Stock Exchange. It was further stated that the integration of Bemis is underway, and the company remains confident in its ability to deliver $180 million of pre-tax cost synergies by 2022 fiscal year-end. The company’s capacity to drive the shareholder returns is evident as it has announced initiatives, which include increasing the dividend, returning $500 million to the shareholders with the help of share buy-back and deploying at least $50 million towards the strategic projects in order to accelerate sustainability agenda.

.png)

Shareholder Value Creation (Source: Company Reports)

Completion of Acquisition of Bemis: AMC has earlier announced the completion of the acquisition of Bemis Company Inc., effective June 11, 2019. The combined company would now be operating as Amcor plc, trading on the New York Stock Exchange. The key personnel of AMC stated that acquisition of Bemis brings additional scale, capabilities and footprint, which would be strengthening the company’s industry-leading value proposition. Additionally, it would be generating significant value for the shareholders.

How Flexibles Segment Performed in FY19: The company’s Flexibles segment posted net sales amounting to USD 6,566.7 million, which implies a rise of 5.4% in constant currency terms, out of which 3.3% reflects the additional sales from legacy Bemis business since June 11, 2019. The following picture provides an overview of the key numbers of Flexibles segment:

.png)

Flexibles Segment (Source: Company Reports)

The organic growth mainly implies a combination of increased sales and robust operating cost performance, final benefits from legacy Amcor restructuring initiatives of around $9 Mn and the benefit of around $5 Mn from normal time lag in recovering the increased raw material costs.

Rise Witnessed in Rigid Packaging Segment’s Net Sales: The Rigid Packaging segment witnessed net sales amounting to US$ 2,892.7 million in FY19, which implies a rise of 5.4% in constant currency terms that consists of 3.7% of favorable impact from pass through of increased raw material costs. The segment’s adjusted EBIT amounted to US $308.2 million, which was 4.8% higher than the previous year in the constant currency terms implying increased volumes, favorable product mix and benefits from restructuring initiatives of around $8 million. The following picture provides a broader overview of the performance of Rigid Packaging segment:

.png)

Rigid Packaging (Source: Company Reports)

Robust Balance Sheet Position Strengthens Confidence in Future Performance: The company posted net sales amounting to USD 9,458.2 million in FY19, which implies a rise of 5.5% in constant currency terms, while its adjusted net income amounted to $729.5 million, reflecting a rise of 9%. The company stated that its net cash inflows provided by the operating activities fell $95.3 million, or 10.9%, and stood at $776.1 million for the fiscal year 2019, from the fiscal year 2018 figure of $871.4 million. The fall was mainly because of the Bemis transaction-related costs partially offset by the improvement with respect to working capital. The company has a robust balance sheet, and it is having a capacity for growth. The following picture shows that there has been an increase in the adjusted free cash flow in FY19, and the figure stood at $733.4 million while in FY18 it was $643.4 million:

.png)

Cash Flow (Source: Company Reports)

What to Expect from AMC Moving Forward: The company’s business strategy revolves around 3 components, i.e., focused portfolio, differentiated capabilities and aspiration to be THE leading global packaging company. The company’s portfolio of businesses has been sharing some crucial characteristics like focus towards primary packaging for the fast-moving consumer goods, good industry structure, attractive relative growth, and multiple paths to win from the leadership position, scale, and other competitive advantages. The company has provided guidance for 2020 fiscal year, and there are expectations that its adjusted EPS (cps) in the constant currency terms might be in the range of 61.0 - 64.0 cents and pre-tax synergy benefits are expected to be ~$65 million. The following seems important in this regard:

.png)

Guidance for 2020 Fiscal Year (Source: Company Reports)

The company’s cash flow after the dividends (after cash integration costs) is expected to be in the range of $200 - $300 million, and cash integration costs are expected to be around $100 million. The long-term potential of the company happens to be substantial. It was stated that $50 million strategic investments revolve around further accelerating the progress against sustainability goals with the help of additional R&D infrastructure, manufacturing equipment, partnerships and open innovation. The company’s general corporate expenses in the constant currency terms are expected to be between $160 - $170 million, while the net interest costs are anticipated to be in the ambit of $230 – $250 million.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

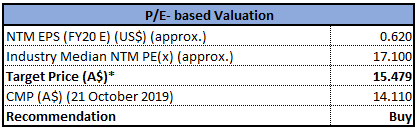

Valuation Methodology: Price to Earnings Based Valuation

PE- based Valuation (Source: Thomson Reuters), *1 USD equals 1.46 AUD as on October 21, 2019

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of AMC has witnessed a fall of 8.52% in the span of the previous six months, while in the time span of the past three months, the stock has fallen 10.95%. Currently, the stock is trading slightly below the average of 52-week high and low levels of $16.74 and $12.665, respectively, with PE multiple of 27.07x and an annual dividend yield of 4.57%. Additionally, the company’s robust cash generation capabilities and balance sheet position might support the overall company moving forward. The company stated that its base business has been performing well and the momentum is heading into 2020, and there is visibility to the near-term earnings growth. Given the backdrop of aforesaid facts and business prospects, we have valued the stock, using a relative valuation method, i.e., price to earnings multiples, and arrived at a target price of high single-digit growth (in % term). Hence, we give a “Buy” rating on the stock at the current market price of $14.11 (up 0.284% on 21 October 2019).

AMC Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...