Kalkine has a fully transformed New Avatar.

Company Overview: Amcor plc is a packaging company. The Company’s segments include Flexibles and Rigid Plastics. The Company offers a range of packaging related products and services, including packaging for beverages, food, healthcare, and personal and home care, tobacco and industrial applications. The Flexibles consists of operations that manufacture flexible and film packaging in the food and beverage, medical and pharmaceutical, fresh produce, snack food, personal care and other industries. The Rigid Plastics segment consists of operations that manufacture rigid plastic containers for a range of predominantly beverage and food products, including carbonated soft drinks, water, juices, sports drinks, milk-based beverages, spirits and beer, sauces, dressings, spreads and personal care item and plastic caps for a variety of applications.

.png)

AMC Details

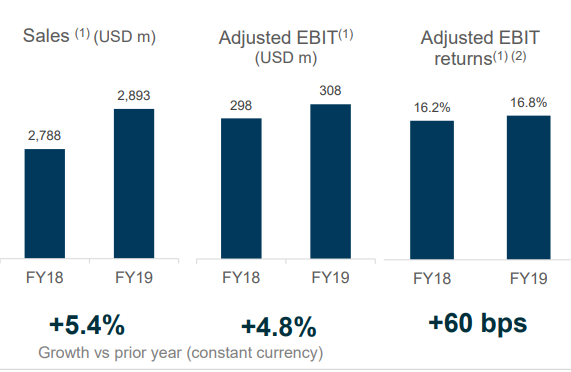

Decent Performance in FY19: Amcor PLC (NYSE: AMCR, ASX: AMC), formerly known as Amcor Limited, is a large-chip packaging company with the market capitalisation of ~$24.05 Bn as of 16 September 2019. It is engaged in the business of developing and producing rigid and flexible packaging for the food, beverage, home- and personal-care and other fast-moving consumer end markets. The company operates in two business segments, namely Flexibles Segment and Rigid Packaging segment, which contributed revenue around 70% and 30%, respectively in FY19 of total revenue. Recently, the company released a decent set of numbers for FY19 wherein its revenue witnessed a rise of 5.5% to $9.5 Bn while, during the same period, EBIT and net income amounted to $1,075 Mn and $730 Mn, respectively, exhibiting a respectable growth of 5.7% and 9.0% on a YoY basis. On June 11, 2019, the company wrapped up the acquisition of Bemis Company, Inc., which is a global manufacturer of flexible packaging products. As per the terms of the agreement, Bemis shareholders got 5.1 Amcor shares for each share of the Bemis stock while the Amcor shareholders got 1 Amcor CHESS Depositary Instrument (or CDI) for each share of the Amcor Limited stock issued and outstanding. The CEO of Amcor reflected favourable viewpoints with respect to the FY19 results by stating that 2019 was the transformative year, which was marked by successful completion of Bemis acquisition along with listing on the New York Stock Exchange under the symbol “AMCR”. The company remains confident in its ability to deliver $180 million of the pre-tax cost synergies by 2022 fiscal year-end. As per the release, legacy Amcor business has performed well during FY19, delivering results which were in line with the anticipations and building the momentum in the several areas like safety, sales, and working capital. The company’s financial profile is robust and would be enhanced as it delivers the financial benefits from Bemis acquisition and continued organic growth throughout the business. As of June 30, 2019, the company employed approximately 50,000 people worldwide.

Considering the company’s robust balance sheet and capacity to generate the higher levels of free cash flow as financial benefits from Bemis acquisition are delivered, AMC is positioned to redeploy proceeds from the divestments and, at the same time, it can maintain the ability to invest towards the organic growth and acquisitions as well as maintaining robust investment-grade credit metrics. The company’s capacity to drive the shareholder returns is evident in initiatives which include increasing the dividend, returning $500 million to the shareholders via share buy-back and investing at least $50 million towards the strategic projects in order to accelerate sustainability agenda.

.png)

Full Year Adjusted Financial Results (Source: Company Reports)

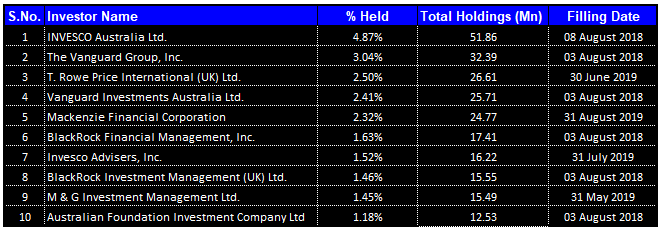

Top 10 Shareholders: The following table provides an idea of the top 10 shareholders in Amcor PLC:

Top 10 Shareholders (Source: Thomson Reuters)

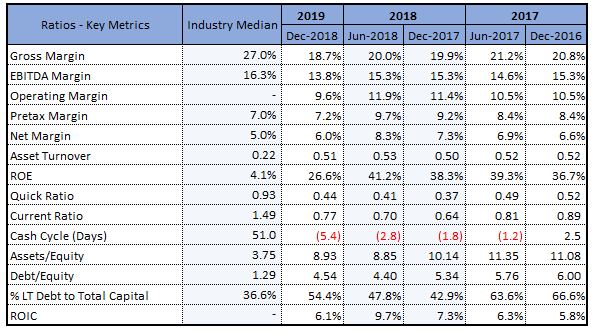

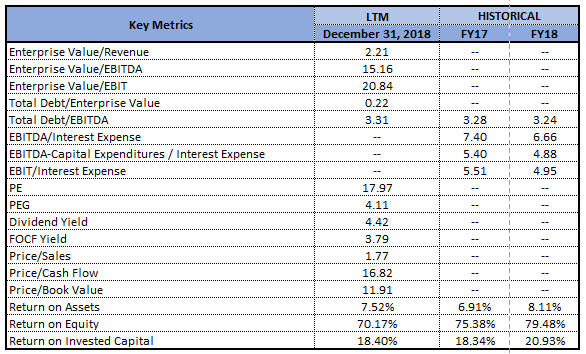

Decent Position in Key Margins: The company’s net margin stood at 6% in 1H FY19, which is higher than the industry median of 5% and, thus, it reflects that AMC is possessing better capabilities to convert its top-line into the bottom-line. Additionally, during the same period, the company’s operating margin stood at 9.6%. The company’s RoE (or return on equity) stood at 26.6% in 1H FY19, which is comfortably higher than the industry median of 4.1% and, therefore, it looks like that AMC has been delivering decent returns to its shareholders. The company’s current ratio stood at 0.77x in 1H FY19, which is higher from 1H FY18 figure of 0.64x and, thus, it can be said that AMC is in a better position to meet its short-term obligations. Additionally, decent liquidity levels reflect that AMC could make deployments towards its key business activities which could support long-term growth.

Key Metrics (Source: Thomson Reuters)

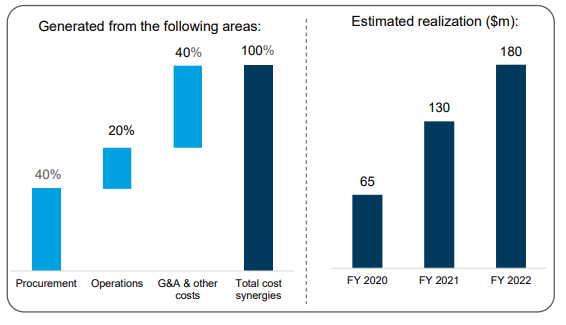

How Bemis Acquisition Could Help AMC Moving Forward: On June 11, 2019, Amcor PLC wrapped up the acquisition of 100% of outstanding shares of the Bemis Company, Inc involving a purchase price amounting to $5.2 billion in an all-stock transaction. With respect to the Bemis transaction, the company has assumed $1.4 billion of debt. The company initiated restructuring activities in Q4 FY19, and the aim was to integrate and optimize the combined organization. As was previously announced, the company has a target to realize around $180 million of the pre-tax synergies driven by the procurement, supply chain as well as general and administrative savings by the fiscal year 2022 end. The strategic rationale of the Bemis acquisition provides a stronger value proposition for the customers, employees as well as the environment. The strategic combination establishes Amcor PLC as a global leader in the consumer packaging with the comprehensive global footprint, scale in every region along with the industry-leading R&D capabilities.

Bemis Acquisition: Cost synergies (Source: Company Reports)

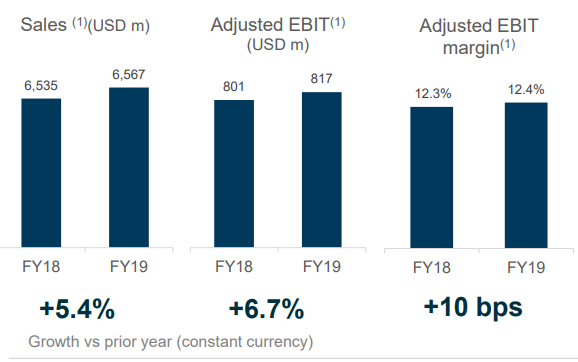

How Flexibles Segment Performed in FY19: The Flexibles segment of Amcor witnessed an increase of 5.4% in the net sales in the constant currency terms, out of which 3.3% reflects the additional sales from legacy Bemis business since June 11, 2019. The segment’s adjusted EBIT amounted to $817.2 million which was 6.7% higher than the last year in the constant currency terms, out of which 3.2% reflects the additional adjusted EBIT from legacy Bemis business since June 11, 2019.

Flexibles Segment (Source: Company Reports)

The organic growth in the segment mainly reflects the combination of the higher sales and robust operating cost performance, final benefits from the legacy Amcor restructuring initiatives of around $9 million as well as a benefit of around $5 million from normal time lag in recovering the higher raw material costs.

Net Sales Rose 5.4% in Rigid Packaging Segment: Amcor PLC’s rigid packaging segment witnessed a rise of 5.4% in FY19 in the constant currency terms which includes 3.7% favourable impact from pass through of the higher raw material costs. The following picture provides a brief overview of rigid packaging segment’s performance:

Rigid Packaging Segment (Source: Company Reports)

The segment’s adjusted EBIT stood at $308.2 million, which was 4.8% higher than the last year in the constant currency terms, reflecting higher volumes, favourable product mix and benefits from the restructuring initiatives of around $8 million.

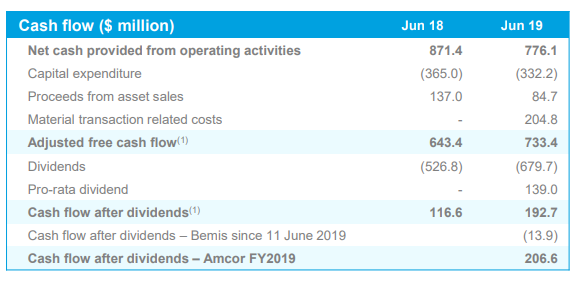

Understanding Position of Cash Flow and Balance Sheet: The company’s adjusted free cash flow (before dividends) amounted to $733.4 million and was $90 million higher than the prior year mainly because of the lower capital expenditure and robust working capital performance. Additionally, the company has a robust balance sheet with the capacity for growth which could help it in gaining traction among the market players moving forward. The Board of Directors declared a quarterly dividend of 12 US cents per share or A$ 0.17725 per share (unfranked) which will be payable on 8 October 2019 to the shareholders. The following picture shows an increase in the company’s adjusted free cash flow:

Cash Flow (Source: Company Reports)

On-Market Share Buy-back: The Board of Directors of Amcor PLC approved the $500 million on-market buy-back of the ordinary shares and CDIs. Additionally, the company has committed to deploy at least $50 million towards the strategic projects to further advance sustainability agenda and accelerate the progress towards 2025 goals.

What to Expect from Amcor PLC: As per the AMC investor presentation September 2019, the company’s base business has been performing well, and the momentum is heading into 2020. The company is uniquely positioned for the long term, and there is visibility with regards to the near term earnings growth. AMC is expecting 2020 to be a transition year as it integrates newly acquired Bemis business. Considering complexities related to simultaneous acquisition, divestment of the certain healthcare plants required by the regulators as well as balance sheet refinancing which are a direct result of transaction, AMC has elected to give additional guidance metrics for 2020 fiscal year.

For the 2020 fiscal year, AMC is expecting adjusted constant currency EPS growth of around 5- 10% as compared to the adjusted combined EPS of 58.2 US cents per share in the 2019 fiscal year. Assuming the 2019 average exchange rates, it reflects the constant currency EPS range of between 61.0- 64.0 US cents per share. The cash flow post dividends in the range of $200 to $300 million are expected, which is after the deduction of around $100 million of the cash integration costs.

For the 2020 fiscal year, additional guidance metrics include the general corporate expenses of between $160 to $170 million in the constant currency terms and the net interest costs of between $230 to $250 million in the constant currency terms. However, the adjusted effective tax rate is expected to be in the range of 21-23%.

Key Valuation Metrics (Source: Thomson Reuters)

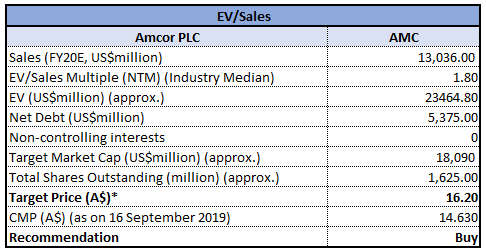

Valuation Methodology: EV/Sales MultipleApproach

EV/Sales Multiple Approach(Source: Thomson Reuters), *1 US Dollar = 1.4553 Australian Dollars as of 9/16/2019

(Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months)

Stock Recommendation: The stock of Amcor PLC has delivered a return of 11.45% on a YTD basis while, in the time span of past one year, it rose 6.10%. The company’s net sales have witnessed a CAGR growth of 1.94% between the span of FY17- FY19. AMC’s cash and cash equivalents have witnessed an increase in FY19 as compared to FY15 and, thus, it can be said that the company is possessing cash generation capabilities which could help it achieving desirable cash levels moving forward. As was announced earlier, the company was required to divest the flexible packaging plants in Europe and the US to secure the anti-trust approval for Bemis acquisition. It was mentioned that combined after-tax proceeds from sale of the assets were around $550 million. Based on the foregoing, we have valued the stock using a relative valuation method, i.e., EV/Sales multiple and have arrived at a target price of the stock lower double-digit growth (in percentage term). Hence, we give a “Buy” recommendation on the stock at the current price of A$14.630 per share (down 1.082% on 16 September 2019).

.png)

AMC Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...