Company Overview - Alumina Limited is an Australia-based mining company. Alumina Limited's sole business undertaking is in the global bauxite, alumina and aluminum industry, which it conducts primarily through bauxite mining and alumina refining. All of those business activities are conducted through its 40% investments in Alcoa World Alumina and Chemicals (AWAC). AWAC has an international network of alumina refineries in the United States, Brazil, Suriname, Jamaica, Spain and Australia. AWAC owns or partly owns, bauxite mines operating in five countries that meet the production needs of the AWAC refineries. AWAC produces chemical grade alumina from three refineries: Kwinana (Australia), Point Comfort (USA) and San Ciprian (Spain). AWAC's shipping operations use owned and chartered vessels to transport dry and liquid bulk cargoes, including bauxite, alumina, caustic soda, fuel oil, petroleum, coke and limestone.

Analysis - The shares of Alumina Limited (ASX: AWC) has been wiped out around 24.3% over the last six months on the back of the company’s poor performance owed to the falling aluminum prices and lower demand from China. The group’s net profit after tax reported a loss of $98.3 million for the full year 2014, against $0.5 million in 2013. The decrease was mainly due to the significant items which included loss on sale of Jamalco (after tax) of $106.5 million and point Henry restructuring charges of $90.8 million. As a result, the earnings per share also posted $(3.5) cents as compared to $0.02 cents during last year. Gearing also decreased to 3.4%, as compared to 4.6% during 2013.

AWAC Joint Venture (Source - Company Reports)

AWAC Joint Venture (Source - Company Reports)

On the other hand, investors need to note the group managed to deliver a net profit after tax excluding significant items of $91.1 million from $29.6 million in 2013, which is a 61.5% increase despite headwinds in the aluminum target market industry. AWAC EBITDA excluding significant items rose 141.2% to $869.0 million from $727.8 million in 2013, driven by lower costs of production and transition to spot based pricing for smelter grade aluminum shipments. AWAC was able to achieve an underlying improvement of $208 million. The strong US dollar, lower shipments and the firm’s initiatives on productivity cost control has led to the decrease in costs. Despite the falling aluminum prices, the group managed to slightly increase its average price per tonne by 0.6% to $310 from $308. AWAC also witnessed a 0.6% increase in its production to 15,902 kt from 15,809 kt driven by the rise in production from Australia, Brazil and US. However, AWAC production is expected to be only 15.2 mt during 2015 due to the sale of Jamalco on December 2014. This forecast does not include the production from Ma’adenJoint venture, wherein AWAC share is estimated to be 251kt.

.png)

AWAC operating performance improvement and production by region (Source: Company Reports)

Solid performance by Alcoa, driven by AWC

Quite recently, Alcoa reported a strong second quarter of fiscal year 2015 performance, with net income (excluding special items) witnessing an year over year increase of 16% to $250 million or $0.19 per share. Alcoa’s revenue rose 1% to $5.9 billion, as compared to $5.8 billion in the corresponding quarter of 2014, on the back of organic growth from aerospace, automotive and alumina business. The major alumina component (most relevant to Alumina Limited) posted a strong business during the quarter and also delivered the strongest first half results in eight years. The Alumina after tax operating income surged to $215 million during the quarter, from just $38 million in the second quarter of 2014. However, the Alumina after tax operating income decreased, as compared to the previous quarter’s $221 million, due to lower pricing as per Aluminum price index and London metal exchange. Meanwhile, the rise in production and higher volumes had offseted this impact to some extent. The adjusted EBITDA per metric ton also surged $59 metric ton to $98 metric ton as compared to the corresponding quarter last year, but reduced $4 metric ton from the previous quarter.

China alumina Production Growth & Forecast (source - Company Reports)

China alumina Production Growth & Forecast (source - Company Reports)

Alcoa also made the first two prepayments under the Alumina segment on its earlier announced twelve year gas agreement for alumina refineries in Western Australia which would be started in 2020. Alcoa paid $300 million during the second quarter and will pay $200 million during next year’s January.

On the other hand, Alcoa continues to close and restrain upstream facilities as a part of its continuing review of 2.8 million metric tons of aluminum capacity (to exit high cost operations). Alcoa cut 443,000 metric tons of alumina refining capacity at Suralco. Alcoa also intends to sell Suralco operations to a Suriname government entity. But, Alcoa joint venture with Ma’aden (which is of Alumina Limited interest) in Saudi Arabia is on track to be completed while efforts to increase the refinery’s production is on track to produce 1.1 million metric tons by 2015. Moreover, the smelter is also on track to attain nameplate production of 740,000 metric tons of primary aluminum during this year.

Recovering Industry

After facing such huge pressure, AWAC estimates an improvedalumina price this year and has taken several initiatives to improve its operating efficiency to maintain its competitive position. The group’s focus towards lower cost capacity with higher production, shift to API pricing basis and San Ciprian gas conversion is expected improve its performance in the coming years.

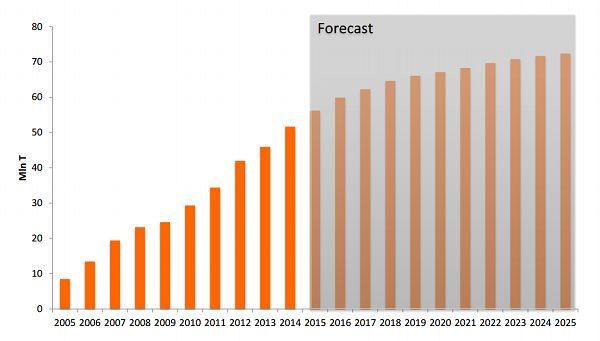

Forecast China Bauxite Imports (Source - Company Reports)

Forecast China Bauxite Imports (Source - Company Reports)

Moreover, after seeing a slump of aluminum demand from over the past few years, the alumina market is estimated to witness a compounded annual growth return of 6.1% during 2019 to 2014 period, which would drive the alumina and bauxite demand. China is estimated to deliver a compounded annual growth return of 6.3%, while the global compounded annual growth return excluding China is forecasted to be 5.8% during the same period. Therefore, over 88 millions of tonnes of bauxite per annum is further needed by 2019.

Recovering demand from China

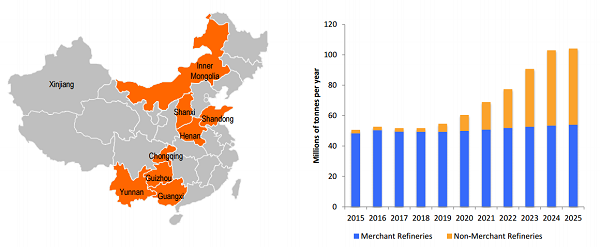

The growing prices of aluminum in China this year due to strong demand and lower supply, offers some support to the companies operating in this industry like AWC. The Chinese producers have ramped up the spot price of aluminum this year by not executing trades in the Shanghai Futures Exchange. Moreover, high oil prices and expanding capacities at west of China are also expected to support the aluminum prices this year. The Shandong region continue to be the leading bauxite-consuming province till 2025. Meanwhile, the Inner Mongolia (rail) and Chongqing (barge) are expected to be the new provinces to import bauxite during 2015 to 2025. Henan and Shanxi refineries might also import high quality bauxite tonnes, as the domestic bauxite grades are able to give quality. The aluminum refineries are expected to reap profits during the fourth quarter of this year on the back of these improved average alumina prices.

.png) China and Global market balance estimates (Source: Company Reports)

AWC repositioned itself to deliver growth

China and Global market balance estimates (Source: Company Reports)

AWC repositioned itself to deliver growth

AWC, being the major alumina producer is making all efforts to deliver growth in coming years. The group is already successful in delivering higher production at lowest quartile of cost. Therefore, AWC has exited from its high cost operations by shutting its point Henry smelter and sold Jamalco. Meanhile, Alumina (with interest of 25.1%) added low cost operations in Saudi Arabia through its Ma’aden joint venture, with a capacity of over 4 million tonnes per annum of bauxite mine and 1.8 million tonnes per annum for alumina refinery. Moreover, to decrease the company’s impact on aluminum prices, AWC intends to de-link alumina pricing by 75% in 2015 and 84% in 2016.

.PNG) Asset portfolio restructure (Source: Company Reports)

Asset portfolio restructure (Source: Company Reports)

Alumina Limited stock has corrected over 10.4% in this month alone but has surged over 2.8% in the last five days, on the back of better than expected Alcoa results and strong performance delivered by Alcoa. Moreover, the recovery in demand from China and improving aluminum prices will offer further support to the stock. We believe that AWC is on track to become among the lowest cash cost refineries in the world, while maintaining its higher production.

Alumina Daily Chart (Source - Thomson Reuters)

Alumina Daily Chart (Source - Thomson Reuters)

Investors need to note that the company’s further improvement in operational efficiency along with rise in production can drive the stock to the higher levels in the coming months. Therefore we give a “BUY” recommendation to the stock at the current price of $1.485.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...