Company Overview – Alumina Limited is a forwarding office for Alcoa World Alumina and chemicals (AWAC) distributions. Its profit is a 40% equity share of AWAC profit, less head office and interest expenses. Its cash flow is AWAC distributions. Alumina was born of the demerger of WMC Limited’s aluminium assets in 2003. First class AWAC investments include substantial global bauxite reserves and alumina refining operations. The high degree of installed capacity, constructed when costs were a fraction of the current affords AWAC ample brown fields expansion opportunities.

Analysis – Alumina Ltd’s or AWC’s earnings drive solely from its 40% equity stake in Alcoa World Alumina and Chemicals, or AWAC. AWAC reported a weaker than expected tripling in underlying 2013 earnings to USD 188 million. We exclude USD 435 million in exceptional costs including Alba legal settlements, Anglesea maintenance and impairments from the underlying figure. Higher than anticipated operating costs was the reason for a weaker performance. AWAC unit operating costs were marginally lower than for 2012. The weaker than anticipated 2013 result and announced closure of the Point Henry aluminium smelter in Geelong are largely offset by a reduction in our long term Australian Dollar/US dollar exchange rate forecast to 0.90 from parity. Point Henry will close in August and accounts for 190,000 tonnes or just over half, AWAC’s annual equity smelting capacity. The smelters are a small component off AWAC’s business overall and Point Henry’s closure is only mildly negative for AWC. AWAC refineries have now migrated to a comfortable mid-lowest-cost quartile position; extraordinary given it is the globe’s largest alumina producer at 12.5% market share.

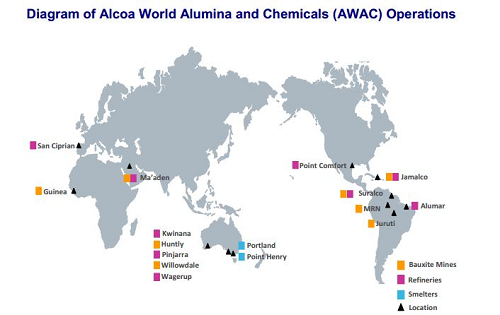

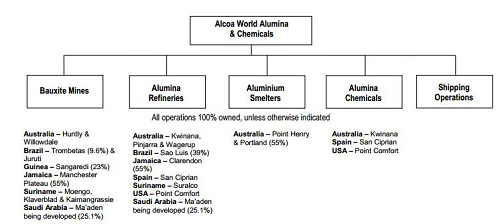

AWAC Operations (Source – Company Reports)

AWAC Operations (Source – Company Reports)

AWAC recorded a reported profit of US$0.5m negatively impacted by US$16m due to the Alba legal matter. A higher level of visibility on legal costs will now be afforded following the conclusion of the Alba Civil settlement and investigations in January 2014 (ongoing since 2008). The closure of Point Henry will also negatively affect AWAC’s accounts by US$240m in 2014. The company is pump primed for when external conditions actually turn positive. Despite AWC’s obvious advantages including a low cost position relative to peers, aluminium is not geographically scarce and the company’s focus on Alumina makes it susceptible to concentrated and volatile market pricing. AWC remains deeply undervalued because of investor capitulation in the face of Chinese overinvestment in Aluminium.

AWAC Operations (Source – Company Reports)

AWAC Operations (Source – Company Reports)

Importantly AWAC reported positive USD 558 million net operating cash flow in 2013 versus only USD 36 million in the previous corresponding period. Free cash flow improved to positive USD 235 million versus negative USD 350 million. Most was paid out to the two shareholders, including USD 108 million to AWC. AWC paid down another USD 62 million in debt, reducing net debt to just USD 135 million, gearing a paltry 5%. AWAC is ungeared. Total AWAC restructuring related charges associated with the smelter’s closure are USD 250 million after tax. Of this USD 120 million is cash with the initial USD 50 million occurring in 2014 and the USD 70 million balance in later years. AWC’s 40% share of the cash component equates to just AUD0.04 per share.

AWC Daily Chart (Source – Thomson Reuters)

AWC Daily Chart (Source – Thomson Reuters)

It is sobering to think AWC’s improvement has come at a time of still extremely challenging market conditions. As well this is before Ma’aden to be one of AWAC’s lowest cost refineries, comes on line in fourth quarter this year. Volumes continue on trend to market pricing, with 65% of AWAC sales to be at spot in 2014 versus 54% in 2013 and 80% targeted by 2016. Meanwhile bauxite prices continue to rise in China, many regions more than doubling during the past five years. And spot alumina prices are back above USD 330 per tonne following a lull leading into the New Year. This is a favourable tailwind for a company with an ungeared balance sheet, limited expenditure commitments and improving cash flow. Year on Year, underlying AWAC EBITDA margin increased to 12% versus 8%, reflecting a 40% increase in alumina product margin to US$45/t. AWAC’s capex of US$ 323m was 17% lower against CY12 on both reduced growth investment and lower sustaining expenditure. A similar trend is guided for the current period as construction of infrastructure at the Jaruti mine in Brazil winds down with US$265m total capex indicated for CY14. AWAC free cash flows of US$310.3m was a significant improvement on FY12. Following a considerable funding restructure in 1H13, Alumina established an undrawn, four year US$300m facility late I the fourth quarter. The business closed FY13 with US$132m net debt versus US$664m or 20% gearing in the prior year.

The improvement to AWAC product margins of US$14/t to US$45/t, reflected a 6% decline in average cash costs per tonne of production year on year. While AWAC group production was relatively flat, cost of goods sold for the year declined, but was unfortunately almost entirely offset by a sharp increase in restructuring and other costs including the Alba legal matter. Further cost reduction initiatives are expected to be implemented over FY14, which in tandem with a guided reduction in capex of 18% and continued weakness in AUD, supports our expectation to EBITDA and cash flow over the coming years. The 100% AWAC owned Point Henry Aluminium smelter assigned for closure in the September quarter represented one of two smelting assets operated in the AWAC portfolio. The company has guided total cash closure costs of US$120m, with US$50m expected to be spent in 2014. Hence the closure cost guidance has had a negligible impact on our Net Present Value of AWAC and Alumina. We believe AWC can achieve stronger unit revenue due to changing contract conditions also we expect stronger alumina volumes due to smelter demand increasing. We are putting a buy on AWC at the current price of $1.18.

Disclaimer

Kalkine provides general advice on securities. Kalkine does not provide advice that takes into account your, or anybody else’s investment objectives, financial situation or needs. We strongly suggest that you should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. Employees and/or associates of Kalkine Pty Ltd may hold one or more of the stocks reviewed on this website. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...