Company Overview - Ainsworth Game Technology Limited is an Australia-based manufacturer and supplier of gaming machines, software and other related equipment. The Company’s product portfolio includes Game Plus, which includes a range of standalone and linked games; Premium Plus, which includes game themed and specialty games with custom touch; and A560 of cabinets. Game Plus include Play 50/100 Lines, 50/100 Lines Rewards, Bingo King, Double shot, High Denom, High Denom Rewards, Hummin’ Mystery, Hyper Bucks, Jackpot General and Jackpot Zone. The Company manufactures global gaming products including, entertaining stand-alone progressives and linked games through its sales offices and distributors in Australia, New Zealand, Asia, Europe, Latin America and the United States.

Analysis - This report brings our attention to Ainsworth Game Technology (AGI), which is an Australian Electronic Gaming Machine (EGM) manufacturer that sells products into North and South America, Asia and Australia. During the AGM, the Company reported robust result for FY14 with an 18% rise in earnings on the previous year. The total dividend payments for the year of 10 cents per ordinary share were declared. AGI further stated that the dividends indicated 52% of after tax profits which has been in consensus with AGI’s obligation to return profits to shareholders. AGI also expects to generate franking credits in FY15.

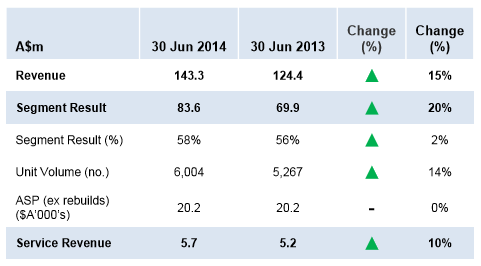

Segment Result_Australia (Source – Company Reports)

The trading update for 1H15 and FY15 entailed 1H15 profit to be below 1H14, however, in line with 2H14. The Company expects the FY15 profit to be ahead of FY14 based on anticipated strong 2H15. Specifically, the update which was provided in November 2014 indicated that there will be revenue gains in FY15 but more heavily weighted to 2H15. The US customer buying patterns is expected to be the leading factor for a better 2H15.

Gaming Products (Source – Company Reports)

It is projected that 2H15 profitability would be ahead of 2H14. The 1H15 domestic sales is expected to be about 30% lower on pcp. This appears to be based on product approvals in NSW and Queensland. Further, untenable growth otherwise seen in Victoria would also be factored-in. More particularly, Australia’s situation is steered by stifled demand around the new A560SL box which is yet to deliver a sales spike and the lack of innovation in new content. However, it is expected that international markets such as North and Latin America will do better and lead to enhanced contributions in 1H15 and FY15.

NSW office of Liquor and Gaming indicated improving slot installations for AGI in 2Q15 compared to 1Q15, which is as per the Company’s comments during the AGM. Specifically, the data highlighted 2Q15 unit volume decline of 22.3% which looks better than the 41.2% decline of 1Q15. The share of installations has seen an improvement with each month with the following statistics - Oct 14.4%, Nov 17.4% and Dec 22.7%, over what was seen in Aug and Sep as 12.7% and 12.9% respectively. There was a 30.9% decline in overall installations in 1H15 as opposed to 1H14 in consensus with AGI’s guidance of 30% decline in revenue in 1H15.

Data from a number of Sydney based clubs illustrates solid on-floor game performance with a further scope for AGI to take floor share. Particularly, SL and X cabinet are expected for release in QLD in February 2015 and additional games have also been provided under the umbrella of the SL cabinet in NSW. Then recent release of multi-game function in NSW is found to be performing well. Thus, there is a good chance that the 2H domestic performance witnesses a spike. The Company has also added up gaming ops units from 422 in FY12 to 1,105 in FY14 given various regulatory approvals helping in enhancing the share in gaming ops market. Over the coming three years, growth into the recurring revenue segment may reach an installed base of 2-3k recurring revenue units.

Historical Financial Performance (Source – Company Reports)

Further, the ship-share data from North America indicated that AGI is moving up to increase its market share given the new game brands which have been found to be performing at greater than 2x house average. 75bps of share gains in North America during FY15 and FY16 in view of opening of new jurisdictions, and annual growth of ~33% through FY16 is expected. Currently, 24% of annual revenue and gross profit for the Company are represented by North America. It is expected that this contribution may jump up to ~40% of group earnings by FY17.

The aspects to be closely watched include the ship share percent in Australia and North America, replacement cycle in Australia and North America, trends in gaming expenditure, regulatory changes and exchange rate fluctuations.

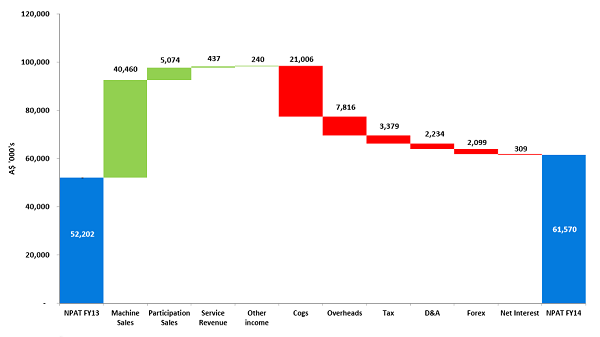

Financial Performance Summary (Source – Company Reports)

We see value in the stock given the continual performance based on the manufacturing quality products and potential to stabilize share in Australia, prospects from the North American market, and a balance sheet with a net cash position at FY14 of A$71m. The earnings also otherwise continue to grow given the fact that the performance of the machines regularly beat expectations.

The Company is well positioned to enhance shareholder value. AGI’s focus on organic growth would also be beneficial in view of the new A$30m Las Vegas facility which is scheduled for a March 2016 opening. This is likely to provide AGI the opportunity to expand into new product lines including steppers. At a gaming exhibition held in Las Vegas, the Company illustrated its exciting range of products, which included two new licensed themed products for the participation market (including Sound of Music™) which are expected to be available in the second half of FY15. Further, a ~4.6% dividend yield in place and North American acquisition values being elevated would help generate a share buyback opportunity.

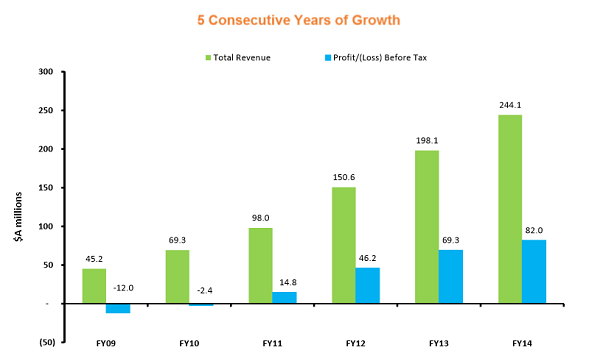

FY14 total sales revenue of $244.1m also represented an increase of 23% on pcp with domestic revenue $143.3m (up 15% on pcp) and international revenue of $100.8m (up 37% on pcp) being reported. Then, the Company had received 31 new licence approvals last year; and as at August 2014, a total of 163 unique jurisdictional licences were at hand with AGI. Given the entire scenario, AGI also intends to invest in product initiatives with Research and Development activities representing 11% of revenue.

AGI Chart (Source - Thomson Reuters)

The partnering with Playtech Limited for the online, mobile, TV and land-based gaming industry through an online content licensing agreement has been benefitting. Through this, AGI planned to feature its most popular game titles across all Playtech platforms in regulated UK and European online sites for desktop, mobile and tablet devices. System integration has been reported to be on track to incorporate the Ainsworth Gameconnect™ RGS, with the expected release for the first 10 games in the second half of 2015. The joint venture with 616 Digital LLC enabled the fast tracking of AGI’s ability to come-up with the launch of the Players Paradise casino. A second social casino is expected to be launched during 2015 to provide unique mobile and tablet game offerings.

Based on the foregoing, we put a BUY recommendation for the stock at the current price of $2.85.

Please wait processing your request...

Please wait processing your request...