Kalkine has a fully transformed New Avatar.

I. Sector Landscape and Outlook

The predecessor to diamond, Coal, the carbon rich mineral fuels the power and Steel industry globally. While the thermal coal’s (accounted for ~78% of the global coal trades in 2019) outlook remains grim, it is comforting to know that only ~50% of the coal exports from Australia came from thermal coal. So, almost the remaining 50% of the demand for Australian coal came for metallurgical or coking coal.

As per the International Energy Agency, dependence on resources such as coal has grown to the extent that coal accounts to almost 38% of the world’s power generation. In 2018 alone, over 1,576 Mega tonnes of coal equivalent were used only for power generation purposes and it is expected to grow to 1,714 Mega tonnes of coal equivalent by 2024. Of the two coal variants, the prospect of Thermal coal is widely discussed and does face its fair share of challenges. However, Asian countries such as India, China and parts of Southeast Asia are expected to continue the usage of thermal coal for power generation for a long time to come. Despite its challenges, the thermal coal is here for long and would continue to light the world with growth from the developing world. We believe that thermal coal is vital for the coal industry, but the major growth lies in the metallurgical coal segment. In this report’s purview, we have discussed the market dynamics of the metallurgical coal.

Fig 1: Australia’s standing in Metallurgical Coal

Source: Australian Energy & Resources Quarterly March Edition

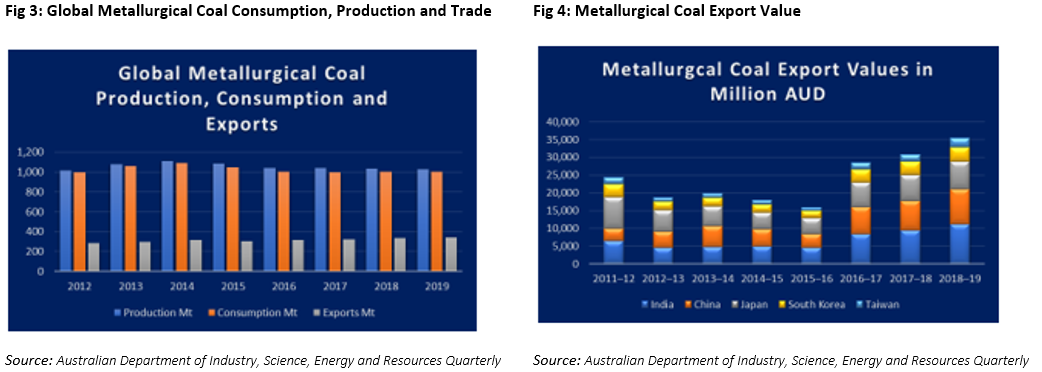

Metallurgical coal export contributed $44 billion to the Australian coal industry’s earnings through 2018-19 against $26 Billion for thermal coal, even though the exports volumes of thermal coal were significantly larger. One of the major drivers to this is the fact that the metallurgical coal commands a premium price over thermal coal and furthermore, Australia produces a larger fraction of higher quality coal product.Let us understand the dynamics of the steel industry to better gauge the demand for metallurgical coal.

Steel Market Braids Iron ore and Metallurgical Coal

Steel is a great collaborator of minerals such as coal and iron ore, playing a major role in the development of the economy. Steel has been the cornerstone of the global economy and would equally be fundamental for the world’s progress in the next decades. Unlike, “THE COMMODITY” crude oil in relation to which the alternatives are trending and are rising, steel has been and will find its application for a long time to come. Around 0.6 tonnes (600 kg) of coke is consumed in producing 1 tonne (1000 kg) of steel, and on an average 770 kilograms of coal is consumed to produce over 600 kilograms of coke, which means that around 770 kg of coking coal is used to produce 1 tonne of steel through this production route.

The per capita consumption of steel is widely regarded as the indicator of socio-economic development and living standard of a nation. As per the World Steel Association, the average per capita global steel consumption has increased by ~50% to 224.5 kilograms in 2018 since the year 2000 and is anticipated to grow by another 50% by the year 2050. In other words, both iron ore and metallurgical coal together form the backbone of a nation’s economy and outlines the path for the future. Thanks to the advancement in the furnace technology, an average of 20 Gigajoules of energy is required to produce a tonne of crude steel which is ~60% lower than the levels six decades ago. With the global production of steel being at 1,845 million tonnes in 2019, the global energy consumption stood around 36.9 billion Gigajoules.

Fig 2: Monthly Steel Production.png)

Source: World Steel Organisation

Now that we have an idea about the usage and demand driver of Metallurgical coal, let us ponder on the pricing, demand and supply dynamics in the market.

Pricing Outlook: Supply Disruptions Continue to Strengthen Prices

Following the decline in the prices through 2019, The premium Hard Coking Coal prices are anticipated to stabilise in the range of US$150-165 a tonne, recovering from the lows of US$135 a tonne in November 2019. The expectation of a rise on Coking coal prices is based on:

- Anticipated global economic recovery

- Slower supply from the US, which is plagued by the profitability issues due to high product and freight costs.

- Countries including Canada and Mongolia faced weather, mining and logistics issue earlier this year further supporting the prices.

What Drives the Demand for Metallurgical coal?

As per the Australian Department of Industry, Science, Energy & Resource, the global demand in 2019 stood at 340 Mt and is anticipated to hit 342 Mt in 2020. Owing to the slowing global economic growth and the weak steel production in China, the metallurgical coal imports flattened during the year. While demand from Japan, South Korea and Taiwan is anticipated to hold ground, a strong demand on the back of a major infrastructure push from India cannot be ignored. With some of the European economies such as the UK, Spain and France now relaxing the lockdown in a phased manner, most of the steel plants which were either suspended or were operating at minimal capacities would now ramp up to contribute to rebuilding and recovery of the economies post the normalisation.

China Story of Revival: With China plagued by COVID 19 since the beginning of 2020, the dragon country still managed to register a growth in the steel production during the first quarter of 2020 producing over 233 Million tonnes of crude steel, registering a growth of 1.5% on yoy basis. With the reopening of china, the steel production is experiencing a strong rebound with both the domestic crude steel production and demand rising, leading to a sharp surge in the iron ore and coking coal prices.

The steel rebar transactions have already recovered to the normal levels. Mining industry majors such as Rio Tinto and BHP have been vocal on a strong recovery from China and expect a higher throughput in 2020, contingent upon China managing its battle against successive waves of COVID-19. A strong push towards infrastructure development is also expected in China, boosting the steel demand and in turn the metallurgical coal demand strongly in 2020 and 2021. BHP, which exports almost half of Australia’s metallurgical coal anticipates a recovery in the sector and is expected to ramp up production during the year. The coal major expects to expand the metallurgical production in the range of 41-45 Mt in FY2020 against 30 MT in FY2019.

The rising domestic metallurgical coal production within China is expected to match the demand. With China planning to shut down the operations of smaller coal mines with capacities lower than 300,000 tonnes by 2021 due to safety concerns, the supply from the domestic mines might take a hit.

Indian Side of the Story: India, the second largest steel producer, is under a nationwide lockdown since the end of March. With the country now under the fourth phase of lockdown which allows the citizen to now go out for employment and allowing the majority of the economic activities open for business, the 1.3 billion strong nation is adapting itself to the new normal. The Indian Government has also announced a massive US$267 billion stimulus package, equivalent to 10% of the nation’s GDP, a splurge in the infrastructure development is expected.

With the Indian unemployment rate standing at around 27.1% at the end of April, the Government is under pressure to address this issue. In the wake of this, the government is expected to announce various initiatives to reboot the economy, which in turn lead to commodities such as steel to see an increase in demand.

In such a case, the steel productions would skyrocket within the country and will require much higher volumes of metallurgical coal, particularly from Australia. A sudden demand from India cannot be ruled out and may take the metallurgical coal prices by storm.

Supply Disruption to Support Coking Coal Pricing

The Supply is expected to remain disrupted due to the weather conditions and the coronavirus outbreak. In early 2020, weather conditions led to a disruption in Canadian supply, with Canada being the third largest exporter of coking coal, which added to the strengthening of prices. Ever since the coronavirus infections spread globally, many of the countries including Mongolia, the largest exporter of Coking coal to China, closed down its borders which in turn led to disruption of coking coal supply to China.

US – A Swing Producer with High Freight and Production Costs: The current coking coal prices also possess issues to the United States, the world’s second largest coal exporter after Australia, on the back of profitability concerns. The high cash cost of the US based mines does not allow sustenance of export activities at lower coking coal prices. The US would have to remain as a swing producer due to high cash cost and also higher freight costs to the demand centres in China, India and other Asian countries. A decline in export from the US would not surprise the market.

Mongolia, China’s largest Supplier Seals Borders Amidst COVID Outbreak: Mongolia, the Chinese neighbour, meets almost 50% of Chinese coking coal imports, but the sealing of borders with China due to coronavirus outbreak disrupted the exports strongly. The Mongolia highway ports at Xiberkulun and Gashun Suhaitu held a disinfection drive leading to a reduction in supply as only 400 vehicles a day were allowed. This led to a depletion of the Chinese inventories during the first quarter. South Gobi Resources, a Mongolian Coking coal producer, suspended its export operations in February and plans to suspend its mining operations until May.

Australia Shows Robust Performance, Nears Coronavirus Freedom

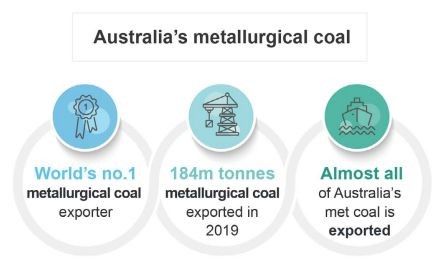

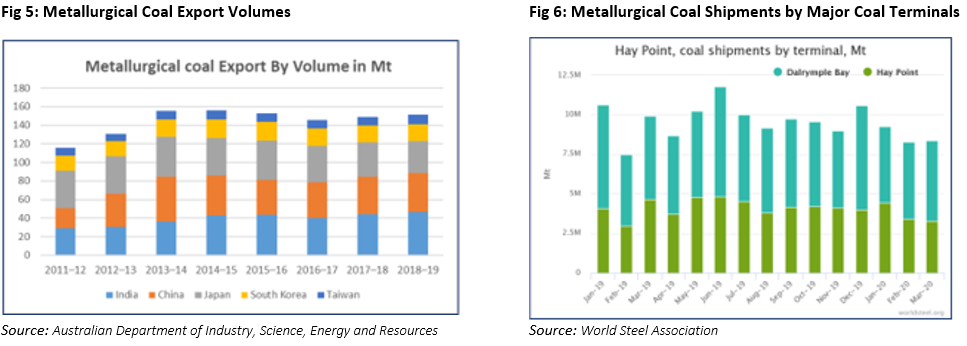

Australia holds the lion’s share in the coking coal industry accounting to almost 55% of the exports globally. The value of Australia’s metallurgical coal exports reached a record high for a second consecutive year in 2018–19.

The Australian exports amounted to 184 Mt, translating to a value of $44 billion driven by high prices and rising export volumes. The Australian Department of Industry, Science, Energy & Resource anticipates the export volumes to grow to 192 Mt in 2020. The country holds a strong portfolio of metallurgical coal projects to further ramp up the production in the future. Interestingly, the Australian metallurgical coal operations and supply chain proved to be resilient during the Coronavirus pandemic.

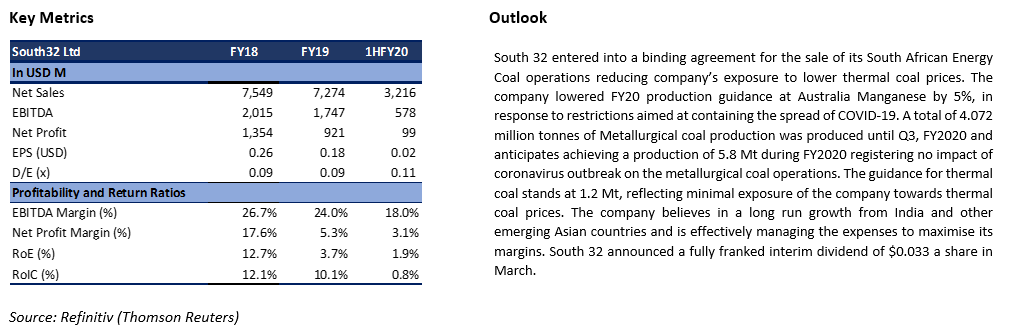

The nation’s two major coal terminals at the Hay Point and Dalrymple Bay, which together account to more than 50% of the metallurgical exports, recorded nearly stable export volumes indicating the robustness of the Australian coking coal industry. With Australia now having around 535 active coronavirus cases (as per the Australian Department of Health as on 20 May 2020), the country is expected to face no major disruptions at any of their mining sites.

Risks to be borne in mind: The recovery from the pandemic is fuelling the demand surge for steel and in turn, metallurgical coal. Markets such as China, India and other Southeast Asian economies may emerge as the driving force for the metallurgical coal with vast infrastructure development. However, the economic conditions of these nations may either strengthen or weaken the metallurgical coal market. Though climate concerns raise some level of uncertainty over the future of thermal coal, the switch, if happens, can take a long time. Also, with rising environmental consciousness, many thermal projects may find difficulty in securing funds. Growth in demand for the coal is expected in the near term, but the question remains, how and when will the global economy get back on the track. Nonetheless, with moderate expectations from the thermal coal segment, metallurgical coal is anticipated to take the coal sector forward in the upcoming time.

II. Investment Theme and Stocks under Discussion (S32, NHC, WHC and SMR)

After gauging through the coal market dynamics, let’s take a detailed look at the companies operating in this sector, in terms of their performance and outlook. We have assessed the coal companies’ stocks based on Discounted Cash Flow (DCF) method.

1. ASX: S32 (SOUTH32 LIMITED)

(Recommendation: Buy, Potential Upside: Low Double Digit, Mcap: AUD 9.64 Billion)

South 32 is a diversified mining giant with operations spread across the globe. The company owns and operates the Illawarra Metallurgical Coal operations which produces premium hard coking coal.

Valuation

Our illustrative valuation model suggests that stock has a potential upside of ~15% on 20 May 2020 closing price..png)

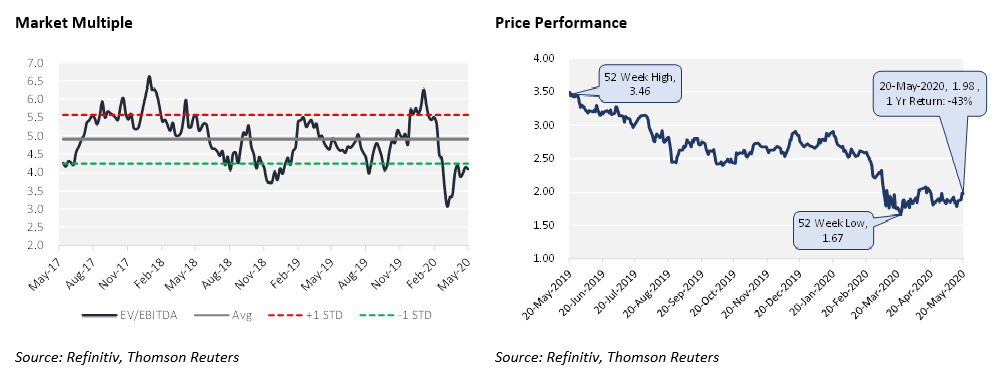

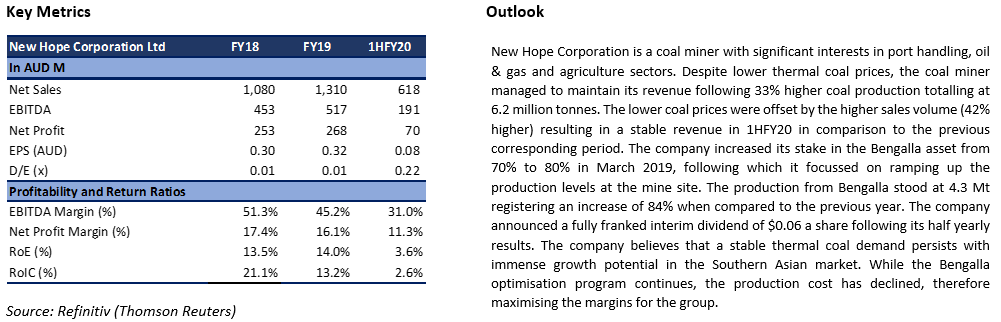

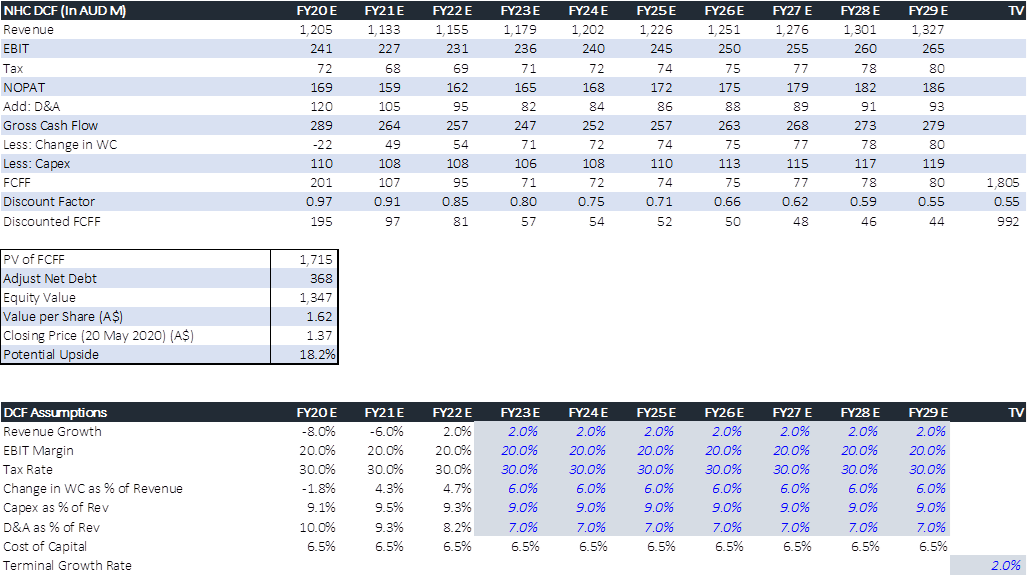

2. ASX: NHC (NEW HOPE CORPORATION LIMITED)

(Recommendation: Buy, Potential Upside: Low Double Digit, Mcap: AUD 1.14 Billion)

New Hope is a coal miner based out of South East Queensland. The Company's principal activities include coal mining, oil and gas, marketing and logistics, and investments.

Valuation

Our illustrative valuation model suggests that stock has a potential upside of ~18% on 20 May 2020 closing price.

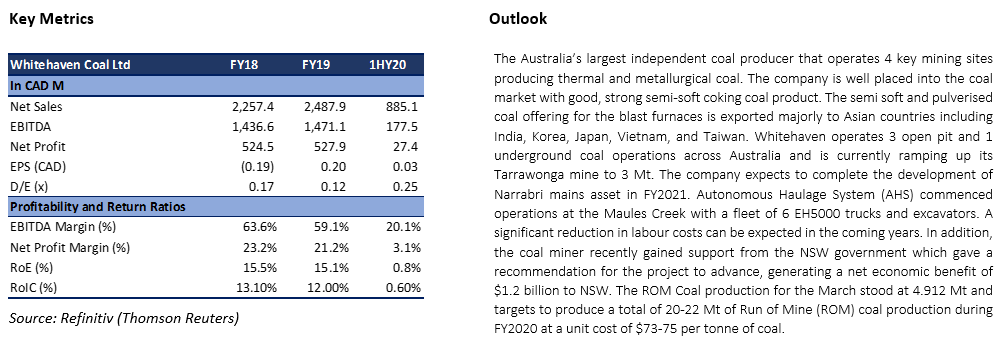

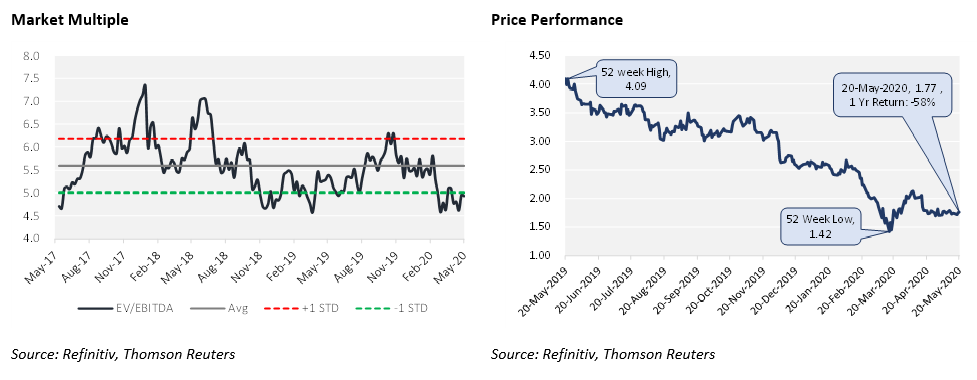

3. ASX: WHC (WHITEHAVEN COAL LIMITED)

(Recommendation: Buy, Potential Upside: Low Double Digit, Mcap: AUD 1.8 Billion)

Whitehaven is an independent miner operating key coal mines in the Gunnedah Basin producing high energy thermal coal and metallurgical coal.

Valuation

Our illustrative valuation model suggests that stock has a potential upside of ~17% on 20 May 2020 closing price..png)

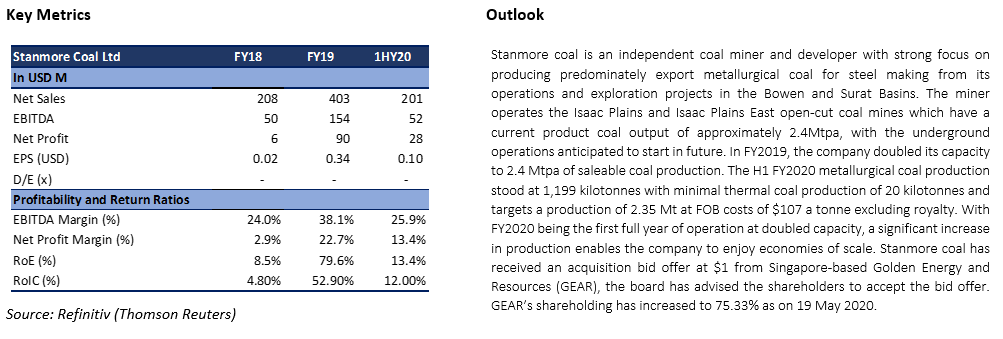

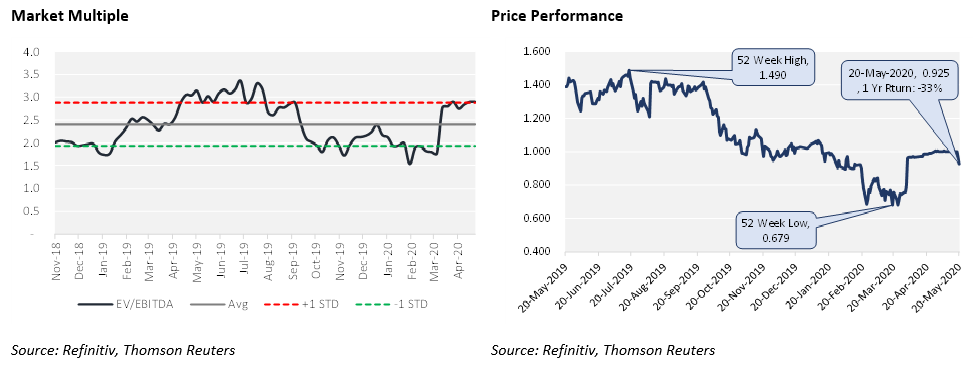

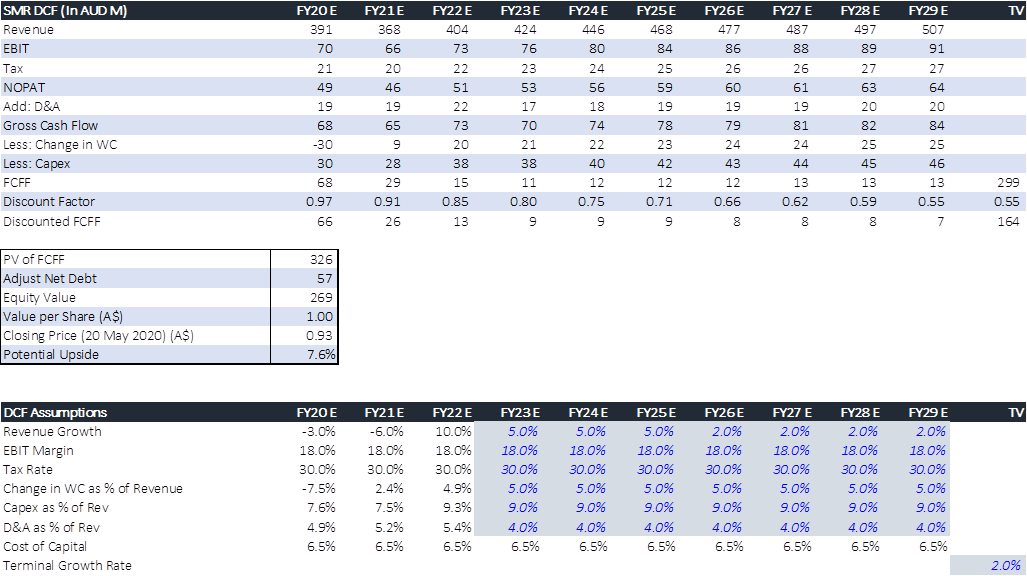

4. ASX: SMR (STANMORE COAL LIMITED)

(Recommendation: Hold, Potential Upside: High Single Digit, Mcap: AUD 259.6 Million)

Stanmore Coal Limited is a coal mining company. The Company's principal activities include the development of operation of coal mines in Queensland, Australia.

Valuation

Our illustrative valuation model suggests that stock has a potential upside of ~8% on 20 May 2020 closing price.

Note: All the recommendations and the calculations are based on the closing price of 20 May 2020. The financial information has been retrieved from the respective company’s website and Thomson Reuters. All the recommendations are valid on 21 May 2020 price as well.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...