Kalkine has a fully transformed New Avatar.

(6).png)

COVID-19 – An Unprecedented Crisis: Initially a national health emergency and now a global pandemic, as declared by the WHO, Coronavirus or COVID-19 has hit hard on the sentiments of the stakeholders of planet earth. The virus is said to have originated from a Wet market in the Chinese city of Wuhan and has been transmitted from animals to human race. As soon as the virus started claiming its territory outside China, the outbreak has had various socio-economic implications with countries declaring a complete lockdown to prevent the spread. While some countries living in denial faced the worst consequences, others have set the stage to fight the foe.

Four Months of Becoming a Global Threat (December 2019 – March 2020): With the number of infections across the world rising over 600,000 and more than 30,000 lives engulfed by the slowly crippling disease, the virus has so far been a mystery for even the largest healthcare systems across the world. For instance, Italy, which was ranked by the WHO amongst the top healthcare systems in 2019, has seen the worst impact in terms of the number of deaths despite a complete lockdown. On 23rd March 2020 alone, the deadly virus claimed over 600 lives in the country with the total number of cases standing around 64,000. Apart from Italy, some of the severely impacted countries include Iran, Germany, France, the USA, South Korea, Switzerland, and the UK. Wuhan, the epicentre of the disease, has seen a drastic drop in the number of new cases due to strict measures taken by the government. As a result, the city has eased out some of the restrictions with a view to embark on the journey of recovery.(13).png)

COVID-19 Cases - 22 January 2020 to 29 March 2020 (Source: WHO)

Covid-19 Pain accompanied by Sharp Weakness in Crude Oil: As COVID-19 continued to trigger panic across the world, global stock markets became victims of a massive sell-off, with a large amount of investor wealth being shaved off owing to the rising economic threat. Things escalated further as a result of the crude oil war between Saudi Arabia and Russia, with Russia refusing to cooperate in balancing the oil prices by slashing production, as advised by the Organisation of the Petroleum Exporting Countries (OPEC). As a result, Saudi Arabia, the world’s largest exporter of oil, further decided to backfire by deciding to boost its crude output above 10 million barrels per day after the deal to curb production expires. Consequently, crude oil prices witnessed a sharp fall of around 30% on 9th March 2020.

.png)

Brent Oil Chart – Last 6 Months (Source: Thomson Reuters)

A Historical Sell-Off in Equity Markets Worldwide: Despite the efforts of Central Banks to curb the adverse economic impacts of COVID-19, global equity markets continued to sink as panic aggravated. As the US Federal Bank announced a rate cut to a range of 0 – 0.25%, the Dow Jones Industrial Average witnessed a steep fall of 12.9% and UK’s FTSE 100 went down by 4%. The Australian markets couldn’t escape the turmoil for long and saw the largest one day drop after the rate cut was announced. As per media reports, the benchmark index (S&P/ASX 200) went down by ~9.7 percentage points on close.

Fallen Equity Markets, Rising Volatility, Financial Watchdogs’ Actions; Will Recovery be that Sharp?: The uncertainty arising from the coronavirus pandemic is such vast that volatility indices across the major equity markets have witnessed large swings since mid-February 2020 with few broader indices such as Dow Jones, Nifty, FTSE, etc., breaking the circuits during trading sessions. Most of the leading Indices suffered from the biggest drops in history during this period due to the panic selling. The spreading pandemic led the financial authorities across the global to take immediate measures to alleviate the pain of the economies. U.S. Federal Reserve pumped in a big package in the financial system, following a 50 bps cut on 03 March 2020. On similar lines, Bank of England cut the interest rates by 50 bps while British Government announced a spending package of $39 billion. European Central Bank (ECB) announced $135.28 billion expansion to its asset purchase program.

Now the question arises when will the equity markets rebound? We opine that these scars on the economies and businesses are likely to remain in the short to medium term and next few quarters’ corporates earnings may not be able to meet the expectations, and these facts are largely digested by the equity markets. Having said that, the recovery is expected to be seen but we do not completely rule out any further hiccups and selling pressure in the near term. In this scenario, many factors will play a role in deciphering the route to recovery and whether it will be a V-shape recovery or a protracted one.

10-Year Comparative Chart - Market Volatility Indices (Source: Thomson Reuters)

Impact Across the businesses by Outbreak: As the effects of coronavirus multiplied rapidly, some of the businesses were badly impacted due to a slowdown in manufacturing activities, restricted imports and loss in demand. On the contrary, there were businesses that remained intact as the need for essential commodities drove sales.

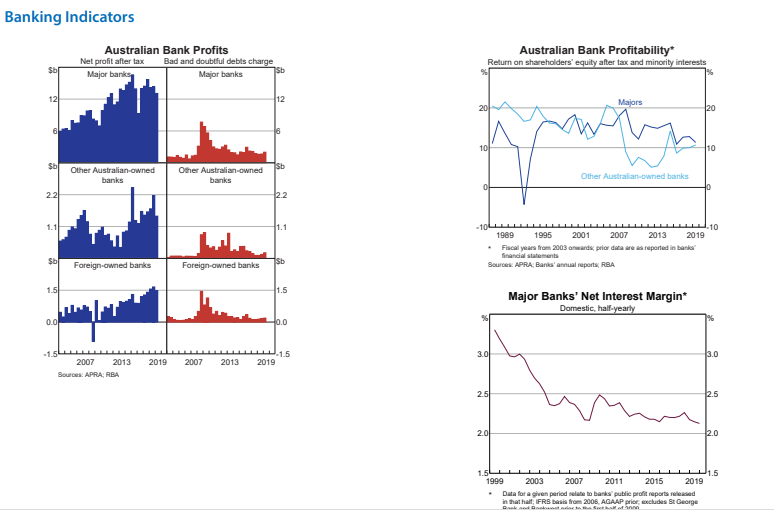

(1) Banks to lend Moral Support amidst the Downfall: The Australian big four banks had a rough trot due to increased quantitative easing by the Reserve Bank of Australia during the tough times. As the RBA reduced interest rates to 0.5% in March 2020, the expectation of losing a part of their earnings led to a fall in share prices. As businesses across varied sectors resort to preventive measures and adhere to government regulations, the banking sector stands at a risk of increased default in repayment of loans. Supply chain disruptions along with the effects of social distancing have led to a decline in revenues that can lead to delayed payments. Threat to household income poses another uncertainty due to potential failures in credit card payments and mortgage payments. Henceforth, while the demand for loans doesn’t seem to rise, banks are required to be supportive enough to lend the required time for repayments.

Historical Performance – Banking Sector (Source: RBA)

(2) Riding & Rising Through Difficulties is what the Situation Demands: Players in the automotive sector, particularly those sourcing components from China, witnessed a loss in business due to slowdown in manufacturing activity in China. The sector has also been impacted by a drop in demand for new cars, taxis, as well as ride sharing services as people were advised to stay indoors. Closure of leisure and recreational centres such as cinemas and amusement parks, hotels, restaurants and cafes, also fed into the drop in the sector’s performance.

(3) When one of the Largest Consumers of Resources gets Quarantined: With respect to the resource sector, Australia being a major supplier of iron ore, LNG and energy products, and metallurgical and thermal coal to China, suffered a loss of exports. It has seen a setback in demand as factories in China went on a halt, raising business uncertainties for Australian resource producers in near future. However, with conditions stabilising in China, one can expect the businesses to go back on track very soon.

(4) Be ready to Land in Trouble if you Choose to Fly during Crisis: As travel bans to the severely affected countries increased and clouds of uncertainty loomed over the business, players in the aviation and tourism industry resorted to cost-cutting measures and withdrawal of earnings guidance. Airlines saw a substantial decline in international traffic and were persuaded to reduce the capacity in order to control costs. Looking at the positive side, the above restrictions have helped the government to prevent the outbreak from reaching the uncontrollable and fatal stage for businesses and the economy.

(5) Survival is Essential for Fighting the Battle: An economic downturn has the history of benefitting the consumer staples and food industry, as a result of increased grocery spending. Even in the initial stages of the outbreak, consumers started hoarding essential goods such as food products, household items and hygiene products, to avoid the risk of shortage at times of severe crisis. As a result, such businesses have seen a rise in sales and earnings as demand accelerated.

(6) Health Always Comes First: A major chunk of healthcare providers have come forward to protect the world against the novel coronavirus by ramping up production of Personal Protective Equipment (PPE). Moreover, due to the inelastic demand for healthcare services and various development initiatives by companies, any decline in the stock price of healthcare companies is expected to recover as soon as the dust settles. The increased role of Artificial Intelligence in Healthcare will also compliment the sector’s performance going forward, through improvements in dealing with healthcare challenges by digital means.

Apart from the above businesses, there were companies in the telecommunication, technology and financial sectors, which had to bear the consequences of strict border controls and social distancing. However, there lies optimism in the fact that the current challenges have pushed the impacted geographies and businesses into realising the dire need of implementing advancements like 5G technology and artificial intelligence, providing better training programs to ensure seamless execution of work and adopting smart city technologies.

Is Investing Really a Dilemma?: A popular statement from Warren Buffet, one of the most successful investors of all time, comes as comfort in the chaos – “Someone is sitting in the shade today because someone planted a tree a long time ago”. With the rising uncertainty, restrictions imposed on travelling, businesses shutting down as a preventive measure, rising tensions among households and the impact on exports and imports due to harder border controls, investors have been on a wobbly ground, seeking the dos and don’ts to survive in the market. During the tough times, investors must be patient enough to retain the stocks with potential rather than panic selling. At the same time, they must be pro-active enough to shed everything belonging to the worst performers.

Amidst the current market scenario, where the fall in stock prices has taken toll over an investor’s confidence, one must be watchful of the quality of holdings and retain or buy the stock that can sustain and provide long term returns in the future. In doing so, being updated with the recent announcements made by the company play a key role in analysing its performance. Apart from that, how the business has responded to challenges in the past is required to assess its immunity to market wide adversities. In addition to a company specific approach, it is very crucial for an investor to understand the risk exposure of various sectors and pick those that are relatively stronger at times of such tough market conditions. Overall, any short-term pain in the field of investments should not be looked at as a failure, if the ultimate goal is to create long-term wealth. With the above philosophy, investors should consider buying the below stocks that demonstrated resilience to the ongoing market conditions and maintain a positive outlook for the business in the long-term.

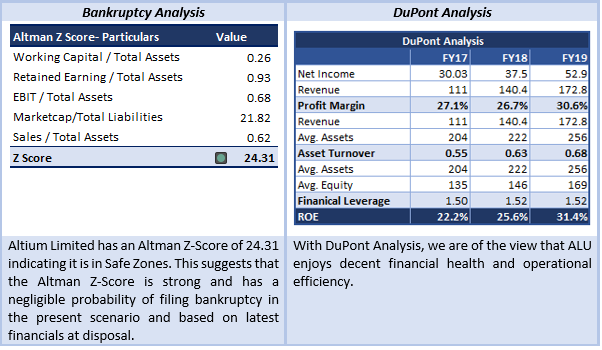

(1) Altium Limited (Recommendation: Buy, Potential Upside: High Single-Digit to Low Double-Digit)

FY20 Revenue and EBITDA Margin to Grow YoY: Altium Limited (ASX: ALU) is a multinational software company focused on electronics design systems for 3D PCB design and embedded system development. During the first half ended 31st December 2019, the company reported revenue and profit growth of 19% and 23%, respectively, as a result of robust performance for all divisions and regions. During the half, Altium Nexus alone delivered revenue growth of 197%. The company has successfully expanded its EBITDA margin while investing in growth initiatives, marking 1HFY20 as the eighth consecutive period of double-digit revenue growth and margin expansion.

What to Expect:

- The business moves forward with a strong balance sheet and expects FY20 revenue to be in the range of US$205 million – US$215 million, as compared to US$171.8 million reported in FY19.

- EBITDA margin on a reported basis is expected between 39% - 40%, as compared to 36.5% in FY19.

(2).png)

Bankruptcy and DuPont Analysis:

Valuation Methodologies:(2).png)

*1USD= ~1.63 AUD as of 30 March 2020

Stock Recommendation: While the stock has shown a sharp correction as a result of a steep rise in market volatility, Altium Limited can be a good pick at the current trading levels as the strong growth trajectory, resilient balance sheet and a decent financial guidance signal brighter prospects for the company. The above factors can act as key catalysts driving the stock price, going forward. Apart from the correction in stock price due to a massive sell-off, the company is expecting results at the lower end of the guidance provided, due to uncertainty regarding the impact of Coronavirus. However, the company has demonstrated a brilliant growth trajectory and is committed to achieve market dominance by 2025 in the PCB design software market. Moreover, it aims to boost adoption of Altium 365, its new cloud platform, to lead industry transformation. Our valuation model suggests a “Buy” rating with potential upside of high single-digit to low double-digit (in % term).

ALU Daily Volatility Chart (Source: Thomson Reuters)

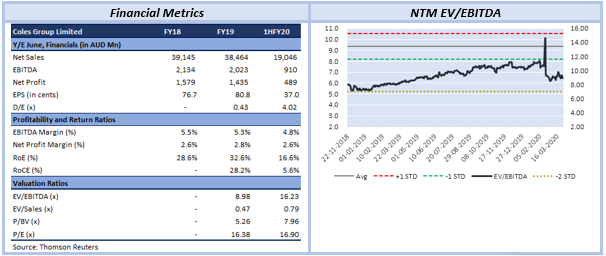

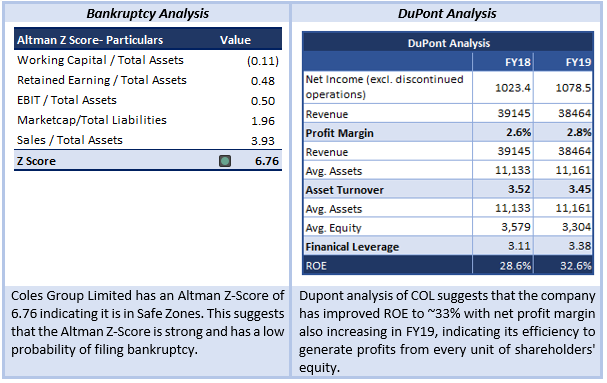

(2) Coles Group Limited (Recommendation: Hold, Potential Upside: Lower Double-Digit)

More than 3,000 New Products Introduced in 1HFY20: Coles Group Limited (ASX: COL) distributes food, groceries, fuel, liquor, etc., through a network of stores and online channel. During 1HFY20, the company delivered a decent financial performance on the back of continued success in strategy execution, as productivity improved and new products were added in the portfolio to serve better value to customers. During the period, the company introduced over 3,000 new products and reported the 49th consecutive quarter of Supermarkets comparable sales growth in Q2. The company also reported progress in its online business, along with $95 million in cost-out as a result of Smarter Selling Initiatives. Going forward, Supermarkets EBIT is expected to benefit from the Smarter Selling provision of $19 million. The liquor business will be impacted due to a collective impact of bushfires, tailored range reviews and clearance activity.

Bankruptcy and DuPont Analysis:

Valuation Methodology:

Stock Recommendation: While the company has seen a delay in shipment of renewal refrigeration equipment out of China due to Coronavirus, which may impact the renewal program and export sales, the stock price has shown a positive reaction in the current turmoil as the consumer discretionary sector continues to be a supplier of essential products to consumers. In the chart below, we can see that the stock spiked equally with respect to market volatility as the consumer goods supplier maintained a defensive stand unlike other sectors. On the business front, the company’s Supermarkets sales went up by 3.3% in 1HFY20 and have raised an optimism with regards to future performance as new products contribute to sales and productivity shoots up. There has been a universal rise in demand for essential consumer goods due to the outbreak of coronavirus, which remains a key positive for the business in the current market scenario. We have valued the stock using EV/EBITDA based relative valuation method and arrived at a target price of low double-digit growth (in percentage terms). The stock is currently trading above the average of 52-week high and low of $18.090 and $11.472, respectively. We believe that most of the positives are factored in at the current levels. Hence, we give a “Hold” rating on the stock at the current market price of $16.82.

COL Daily Volatility Chart (Source: Thomson Reuters)

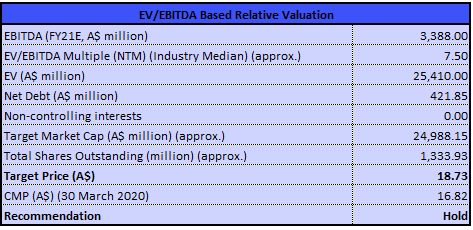

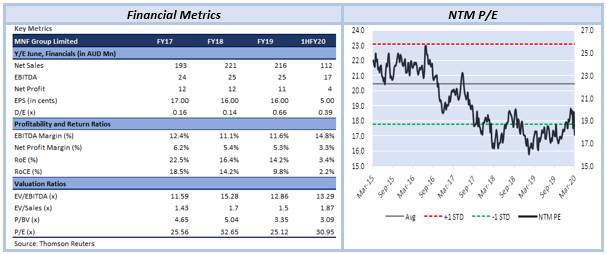

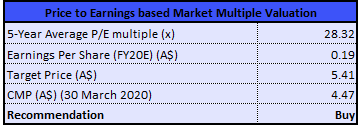

(3) MNF Group Limited (Recommendation: Buy, Potential Upside: Lower Double-Digit)

Strong Demand for Core Products: MNF Group Limited (ASX: MNF) operates a global communications network and software suite enabling leading innovators to serve new-generation communication solutions. During the six months period, the company reported robust results with double digit growth in both EBITDA and NPAT. While EBITDA reported an increase of 52% on pcp, NPAT went up by 20%. This was a result of strong demand for core products i.e., phone numbers with number portability.

What to Expect:

- Performance in FY20 will be backed by strong demand for Australian based phone numbers, used for collaboration and conferencing applications.

- As a result of robust demand and increase in usage volumes, the company expects FY20 EBITDA to be in the range of $36 million - $39 million, subject to uncertainties in the external environment.

Bankruptcy and DuPont Analysis:.png)

Valuation Methodology:

Stock Recommendation: MNF Group Limited’s stock saw a sharp decline as a result of a spike in market volatility, demonstrating the natural reaction to uncertainties. However, with the most recent spike in the market, the price has shown a recovery, which can be attributed to the performance in 1HFY20 and a positive FY20 outlook update, wherein the company reconfirmed its guidance for FY20. The price recovery is also an outcome of a recent rise in demand for MNF Group’s services from businesses that have opted for work from home option as a precaution amidst COVID-19 crisis. While the business remains exposed to external uncertainties, it remains a beneficiary of the strong demand for communication technology. It has seen significant organic growth from the domestic and global customers with a considerable order volume going into 2HFY20. Our valuation model suggests a “Buy” recommendation with potential upside of lower double-digit, valuing at 5-year average price to earnings multiple of 28.32x FY20E EPS.

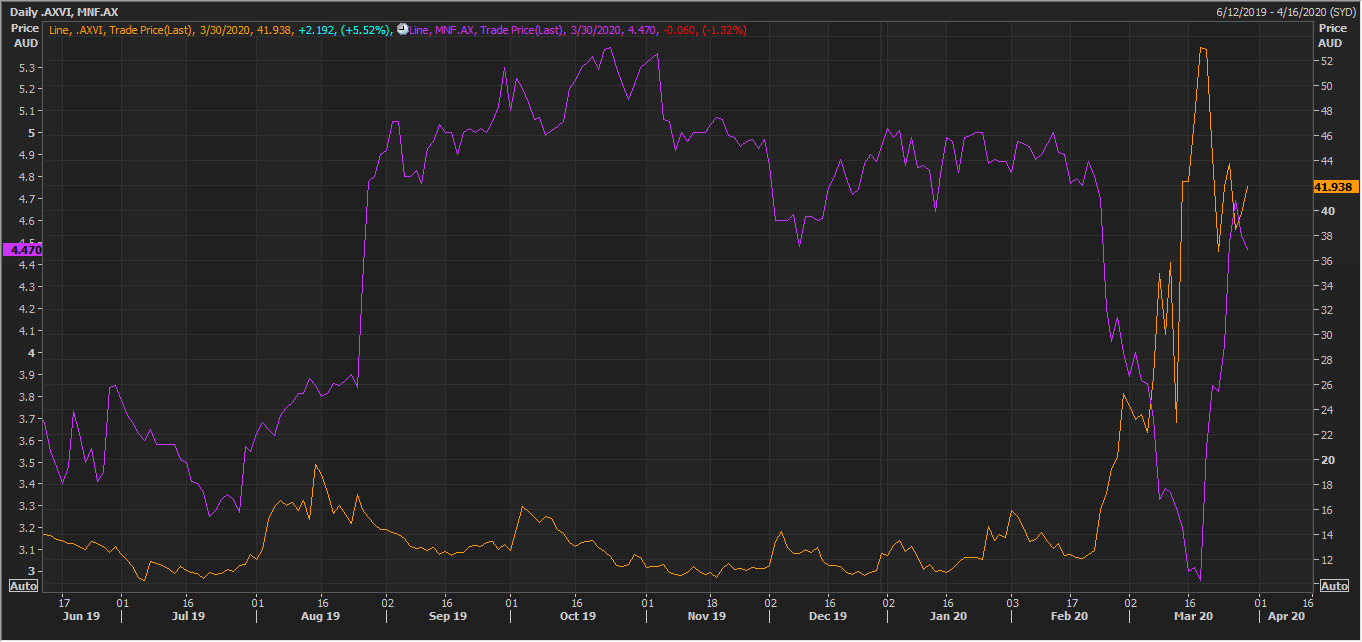

MNFDaily Volatility Chart (Source: Thomson Reuters)

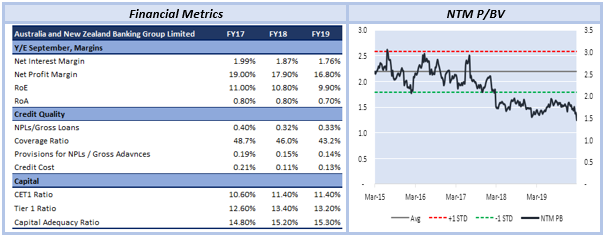

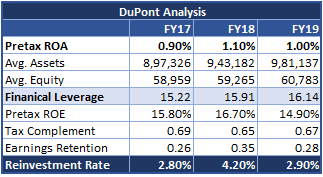

(4) Australia and New Zealand Banking Group Limited(Recommendation: Buy, Potential Upside: Lower Double-Digit)

FY19 Ended with a Strong Balance Sheet: Australia and New Zealand Banking Group Limited (ASX: ANZ) provides banking and financial products to ~8 million customers. During the year ended 30th September 2019, Statutory Profit after tax stood at $5.95 billion and the company reported a stable Common Equity Tier 1 Capital Ratio of 11.4%, above APRA’s ‘unquestionably strong’ measure. Despite a challenging environment, the company continued to enhance customer experience and strengthened its balance sheet. ANZ reported a robust performance in New Zealand and paid full year dividend amounting to 80 cents per share.

What to Expect:

- The bank is expecting to restore its market share in Australia as the Australian home loans business improves.

- The bank looks at diversification as a pillar to withstand geopolitical tensions that can impact earnings. As at 31st December 2019, the Bank had CET1 Capital Ratio of 10.9%.

Bankruptcy Analysis: Altman Z-Score does not apply to banks and insurance companies.

DuPont Analysis:

DuPont analysis for ANZ indicates that the bank has decent levels of Pre-tax ROE with using existing assets to generate healthy NII and recapitalize it to balance the cost of lending and deposits.

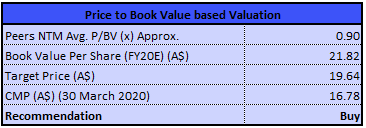

Valuation Methodology:

Stock Recommendation: The stock has corrected sharply in response to the current market scenario and is currently trading very close to its 52-week low level of $14.100. Moreover, with the most recent spike in the market, the stock price reacted by showing an upward movement, which can be looked at as an optimistic scenario. The banking sector has historically been a major victim of a market turmoil due to the obligation for lending the required financial support. Across the world, various regulatory policies by the central banks have had a direct impact on the banking sector, pressurising the earnings with an increased risk of NPAs. The Bank is committed to its stakeholders with a strengthened balance sheet and can be a good buy at the current trading level. The Bank remains in a strong capital position with organic generation capacity. In 2HFY19 it reported organic capital generation of 75 basis points, consistent with historical averages. In February 2020, the bank completed the sale of OnePath Pensions & Investments business for simplification of the wealth business and expects the proceeds from sale to increase the CET1 capital ratio by around 20bps. Our relative valuation model suggests a “Buy” recommendation with potential upside of lower double-digit at the current market price of $16.78. We have taken WBC, NAB, CBA, MQG, and VUK as peer group for comparison purpose.

ANZDaily Volatility Chart (Source: Thomson Reuters)

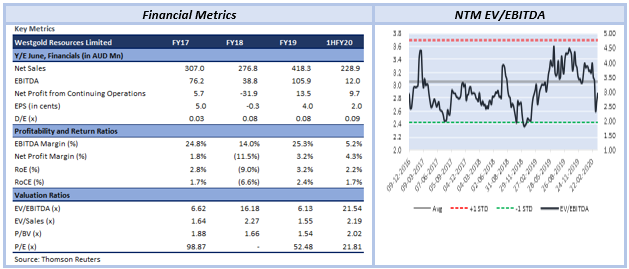

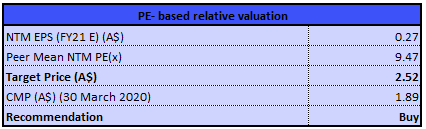

5. Westgold Resources Limited (Recommendation: Buy, Potential Upside: Double-Digit)

No Disruptions in Mine Sites due to COVID-19: Westgold Resources Limited (ASX: WGX) is engaged in the exploration and operation of gold mines in Western Australia. In the wake of COVID-19 outbreak, the company updated that its mine sites continue to operate, with process plants operating at full capacity. During the half year ended 31st December 2019, the company produced 120,127 ounces of Gold, up 17% on pcp. C1 cash costs reduced by 8% and NPAT increased substantially, up 187% to $9.75 million. Overall, in 1HFY20, the company has reported substantial improvement in the financial results, with the mining segments of Meekatharra Gold Operations and Fortnum Gold Operations demonstrating strong profitability. For FY20, the company expects gold production in the range of 275k – 300k ounces, with C1 cost/oz in the range of $1175 - $1230.

Bankruptcy and DuPont Analysis:(2).png)

Valuation Methodology:

Stock Recommendation: In the past, the stock price has demonstrated the usual inverse relationship with market volatility, however, the price has lately started picking pace and has shown recovery despite high market volatility. This pattern can be attributed to gold being considered as a safe haven at times of uncertainties surrounding the stock market. The company has so far not seen any disruptions due to the outbreak of coronavirus and has been running its mine sites smoothly, which will allow for seamless production and accelerated profitability. Moreover, to avoid any disturbances due to any restrictions imposed by the government in the future, the company has incorporated the required changes in the functioning to enable smooth business operations. Our relative valuation model suggests that the stock has a potential upside of double-digit on 30 March 2020 closing price. Hence, we give a “Buy” rating to the stock.

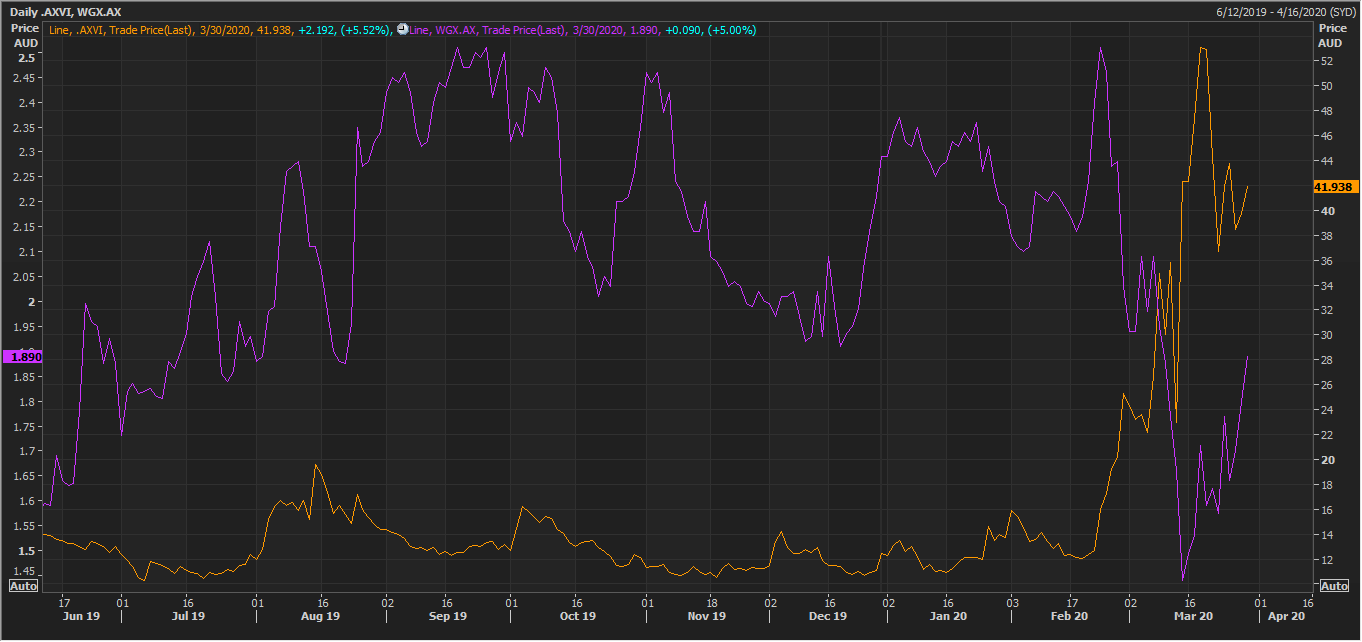

WGX Daily Volatility Chart (Source: Thomson Reuters)

Note:

Altman’s Z-Score Model:

(1) When Z-Score<1.81 than it is in Distress Zone

(2) When Z-Score is between 1.81 and 2.99 than it is in Grey Zone

(3) When Z-Score > 2.99 than it is in Safe Zone

The above relative valuation implies a target price incorporating the key positive factors driving the business and indicate long term potential of the stock. Prices, however, remain subject to any short-term movements due to the impact of coronavirus on the business fundamentals.

All the recommendations and the calculations are based on the closing price of 30 March 2020. The financial information has been retrieved from the respective company’s website and Thomson Reuters.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...