.png)

Stocks’ Details

Australia And New Zealand Banking Group Limited

Positive Outlook: As per the management, Australia and New Zealand Banking Group Limited (ASX: ANZ) managed to report good results in FY 2018 amidst significant challenges. It has adopted the disciplined approach in order to witness favourable momentum in the balance sheet. Also, the shareholders are being benefited by the bank’s capital management strategies.

.png)

FY18 Financial Snapshot (Source: Company Reports)

Further, the management of Australia and New Zealand Banking Group Limited stated that, with respect to the retail banking in the Australian region, the growth in the revenues is expected to get a hit moving forward. Additionally, the management stated that they would be tapping the prospects related to the growth in the Asia, Institutional as well as New Zealand. From technical analysis standpoint, a technical indicator named Moving Average Convergence Divergence or MACD has been applied on the daily chart and the default values have been considered. As per the observation, the MACD line has crossed the signal line and is moving upwards. Therefore, the crossover can be treated as a bullish crossover and the stock might witness a further rise. The stock has fallen 7.75% in the past three months as at November 29,2018 and traded at reasonable PE multiple of 12.25x. Hence, we maintain our “Buy” rating on the stock at the current market price of A$26.800 per share.

.png)

ANZ Daily Chart (Source: Thomson Reuters)

Challenger Limited

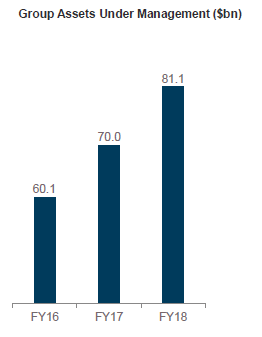

Proposed retirement income framework, to drive annuity sales: Challenger Ltd (ASX: CGF) is a mid-cap company with the market capitalization of circa $6.01 Bn as of 30 November 2018. Recently, the Government’s proposed retirement income reforms which are designed to help provide secure income in retirement, by building retirement solutions that manage risks in retirement while maximizing income. This is expected to drive significant growth in annuity sales and will position Challenger well for the future.

The company recorded the second highest quarterly annuity sales with a figure of $1,171 Mn for the Q1 2019 exhibiting a rise of 7% on PCP. This rise was seen on account of the strong demand for secure income from the growing number of retirees with increasing retirement savings. Annuity sales are also benefiting from Challenger’s expanded distribution reach. The company has maintained its earlier guidance to achieve growth in PBT between 8%-12% on FY2018, also the company has stuck to its 18% pre-tax ROE target. Challenger has announced plans to further expand distribution by making its full range of annuities available on the fast-growing specialist Netwealth platform.

(Source: Company Reports)

The company has a ROE of 10.10 % which is at par with the Industry median. The stock price has fallen over the past three months by 12.30% as on 30 November 2018 and the stock price is trading towards the lower range, representing decent opportunity at current juncture. Hence, considering that the governments retirement framework would expand the Annuity sales exponentially, we reiterate our “Buy” recommendation on the stock at the current market price of $9.520.

.png)

CGF Daily Chart (Source: Thomson Reuters)

Transurban Group

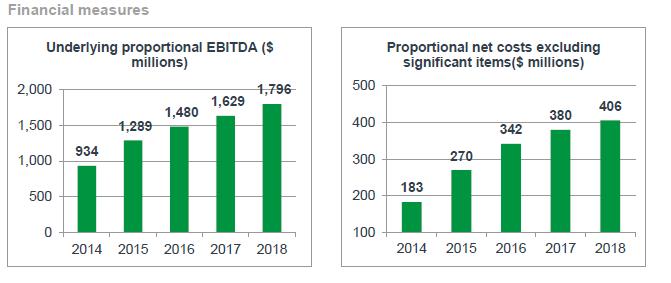

Strong Order Pipeline: Transurban Group. (ASX: TCL) has announced via an ASX press release that the Westlink M7 (“M7”) has priced A$345 million fixed rate 12-year, A$195 million fixed rate 15-year, and A$75 million fixed rate 20-year senior secured notes in the US private placement market (“Notes”). M7 forms part of the North-western Roads Group (“NWRG”). It is to be noted that Transurban has a 50% interest in NWRG. The majority of these proceeds will be used for repaying the M7’s remaining term bad debt, which will get matured in August 2019 & August 2021. This pricing got completed on 29 November 2018, however, the settlement is expected to be done in December 2018.

The company has projects amounting to ~ $10 Bn in the pipeline across Australia and North America, which will be funded through raising the equity & cheap debt via the issuance of corporate notes. The growth for the company shall be fuelled by the heavy spending of the government on the on the Infrastructure sector.

Financial Measures (Source: Company Reports)

The stock has fallen 1.92% in the past three months as at November 29, 2018 and is trading slightly below the average of 52 week high and low prices (i.e., $11.763). By looking at its strong pipeline of orders we expect the top-line to grow further, hence we maintain our “Buy” recommendation on the stock at $11.390.

.png)

TCL Daily Chart (Source: Thomson Reuters)

Paragon Care Limited

Significant market opportunities in Australia and New Zealand: Paragon Care Limited (ASX: PGC) has announced that it has started a critical review of one of its business segments which is “capital equipment”, in line with its undergoing transformation programme. This segment is expected to garner 10% of the company’s forecasted FY 19 revenues. This strategic review is expected to look into the aspects such as evolution of this segment keeping mind the increased focus on innovative technologies and its potential to generate revenues on a concurrent basis.

The firm’s revenues for the FY 2018 were up by 17% and reached $136.7 Mn. This was mainly driven by the acquisition of “Total communications” which has aided in adding high-technology revenues. At present, the healthcare spending in Australia & New Zealand is $193 Bn p.a. & firm’s addressable market is of $ 9 Bn p.a. which is anticipated to grow at a rate of 6% p.a. thus moving further the company expects better opportunities & expansion in its market share.

.png)

Market opportunity in Australia and New Zealand (Source: Company Reports)

The company is trading at an EV/Sales (TTM, as at latest fiscal year performance) multiple of 1.50 times while the industry median stands at around 3 times, which indicates that the company is undervalued considering the sales it is generating. Hence, this parameter suggest that the stock is trading cheap at the current market price. The stock price has fallen substantially over the past three months by 11.03% as on 30 November 2018 thus posing an attractive opportunity for the investors. Hence considering rising top line and robust dividend yields, we maintain our “Speculative Buy” recommendation on the stock at the current market price of $0.635.

.png)

PGC Daily Chart (Source: Thomson Reuters)

Cann Group Limited

Exponential growth in the medical cannabis market: Cann Group Ltd. (ASX: CAN) had posted its numbers reporting its revenue at $1.503 Mn for the year ended 30 June 2018, over the same period the company reported a loss from ordinary activities after tax of $4.726 Mn on the back of high costs incurred on the R&D, cultivation and the product development base.

Going forth, we believe that the medicinal cannabis market is expected to reach US$ 100Bn by 2025 with an estimated CAGR of ~30% on the back of Federal Government’s decision last January to allow Australian producers to access overseas export markets. This would also be aided by a growing number of countries moving to legalize medicinal cannabis. Project Tullamarine will be fully operational by the third quarter of 2020, with a capacity to produce around 40 to 50,000 kilograms of dry flower equivalent product, which’s going to put the company in a leading position to serve the growing Australian market.

CAN’s Growing global market opportunity (Source: Company Reports)

The stock price has fallen over the past three months by 11.11% as on 29 November 2018. Hence, considering the growing legalization of medicinal cannabis across the world, revenues are expected to grow exponentially, thus we reiterate our “Speculative Buy” recommendation on the stock at the current market price of $2.450 as it is trading at lower level.

.png)

CAN Daily Chart (Source: Thomson Reuters)

Woodside Petroleum Limited

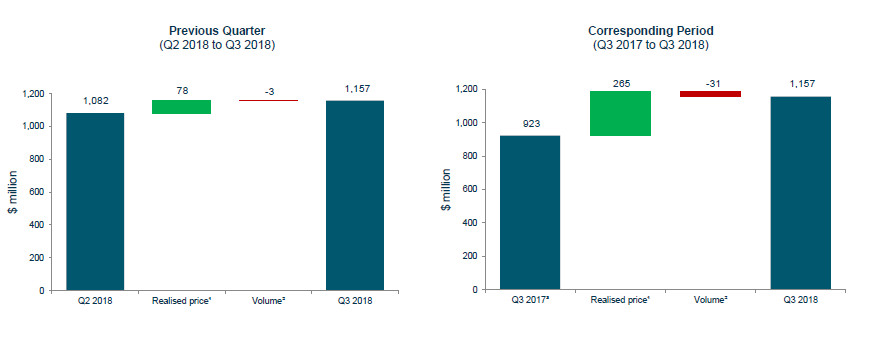

Wheatstone LNG to drive future growth: Woodside Petroleum Ltd (ASX: WPL) stated its recent release that it has inked a gas sale purchase agreement (GSPA) with Perdaman chemicals and fertilizers Pty Ltd for the supply of pipeline gas for a period of 20 years. The pact is such whereby the company will supply an approximate quantity of 125TJ of gas per day for the latter company’s urea plant. This supply shall start between the year 2023 and 2025.

For the quarter ended 30 September 2018, the firm clocked a revenue of $1,157 Mn. This was driven by the higher gas prices prevailing in the market, however, this was partially offset by the tapered sales volumes which were due to the timing of woodside equity sales. There was a production of 23.1 MMboe for the quarter. This was driven by the enhanced production at Wheatstone LNG.

Going further, the company has revised their earlier stated guidance of FY 2018 annual production from 85-90 MMboe to 87-91MMboe & 100 MMboe by the FY 2020. This guidance is on the back of the fact that the company’s LNG Train 1 has achieved the targeted production and Train 2 is on the right track as expected.

Sales Revenue growth (Source: Company Reports)

The company is trading at an EV/Sales (TTM, as at latest fiscal year performance) multiple of 5.60 times while the industry median stands at around 26.80 times, which indicates that the company is highly undervalued considering the sales it is generating. As current market price, the company’s dividend yield ratio is 4.34% which is decent enough & above the Industry median of around 2.7%. Hence, these parameters suggest that the stock is trading cheap at the current market price. The stock price has fallen substantially over the past three months by 15.23% as on 30 November 2018 hence posing an attractive opportunity for the investors. Hence considering rising gas prices and robust dividend yields, we maintain our “Buy” recommendation on the stock at the current market price of $31.060.

.png)

WPL Daily Chart (Source: Thomson Reuters)

Evolution Mining Limited

All operations continue to deliver positive cash flows: Evolution Mining Limited (ASX: EVN) has recently announced that consent has been given to a plant upgrade at the Cowal so as to increase the production capacity to 8.7 metric tonnes per annum. This expansion will fetch a cost of $25-30 Mn. This increase in production is expected to result into additional gold production of 5koz in FY 2020, 10-15 koz in FY2021 and 20kozper annum from FY2022 onwards.

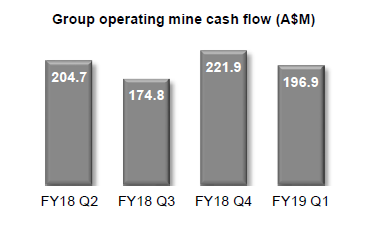

For the quarter ended September 2018, the firm sold 196,021 oz of gold at an average price of A$1662/oz. During the quarter company continued to deliver positive cash flows across its operations after fulfilling its OPEX and CAPEX needs. The operating mine cash flows came in at A$ 196.9 Mn for the September 2019 Quarter vis-à-vis $221.9M for the June 2018 Quarter. This fall was mainly due to the timing of gold sales in September quarter and lower realization in copper prices.

Additionally, the firm has given its guidance regarding the production of 700koz for the upcoming 3 years. This production would be achieved on the back of capacity contributed by the expansion of Cowal plant. As the Australian Gold sector seems to be robust enough, thus we expect that the company will keep on delivering growth in the near future.

Group Operating Mine Cash Flow (Source: Company Reports)

On valuation-wise, the company has a pre-tax margin of 22% against an industry median of 15.5%, this indicates that the company is performing at a better rate compared to the industry at large. Also, the company’s ROE is 11.9% which is decent enough & above the Industry standards. Hence these parameters suggest that the company is a growth stock. The stock price has fallen marginally over the past six months by 0.32% as on 30 November 2018. Hence considering positive cash flows and the above median pre-tax margins, we reiterate our “Buy” recommendation on the stock at the current market price of $3.140.

.png)

EVN Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...