Company Overview: Mineral Resources Limited (ASX: MIN) a Perth-based leading mining services company, focused on providing innovative and low-cost solutions across the mining infrastructure supply chain. MIN also provides pit-to-port infrastructure services across the mining supply chain to Australia’s blue-chip mining companies and MIN’s own and joint venture projects. The company enjoys a world-class portfolio of mining operations across multiple commodities, including iron ore and lithium and aims to grow its core mining services business through innovation, profit sharing projects and its own commodity projects, coupled with industry-leading safety performance.

.png)

MIN Details

.png)

Proven track record of value creation: Mineral Resources Limited (ASX: MIN) is Australia’s leading diversified mining services and infrastructure provider with world-class portfolio of mining operations across multiple commodities, including iron ore and lithium. The company’s business consists of three core pillars: Mining Services, Commodities, Innovation and Infrastructure. MIN has a strong track record of managing the business over 3 decades through industry and commodity downturns and global crisis, building itself on the high-quality portfolio of mining services contracts awarded over the past 25 years. MIN’s strategy has been to invest to drive long-term income streams for the company. It has a strong and proven track record of value creation and return on investment. From 2009 to 2019, the company’s revenue has increased at a CAGR of 19.39% and its NPAT has increased at a CAGR of 14.13%.

.png)

Financial Summary (Source: Company Reports)

Going forward, the company expects its existing and approved projects to drive medium-term growth and sees significant opportunity to deploy capital in long-life, low-cost, high-returning projects. MIN is aiming to double its production and revenue over the next 3 years. In addition, the company is evaluating a range of investment opportunities to support expansionary activities.

FY19 Performance Highlights: The financial year 2019 or FY19 was another year of strong profit and dividend despite volatility in the company’s key markets. For the full year, the company reported a normalised NPAT of $205 million, on revenue of $1.51 billion. Total dividends declared in respect of FY19 amount to 44.0 cents per ordinary share. During the year, the company made significant investments for future growth, with capital outlays of more than $850 million on key projects including Wodgina and Mt Marion lithium projects.

In FY19, the company delivered 378Kt spodumene concentrate from Mt Marion and produced 3Kt of spodumene concentrate from Wodgina. At Koolyanobbing, MIN exported 3.2Mt iron ore during the year and achieved revenue of $117/t.

During the year, the company completed the acquisition of the Koolyanobbing iron ore operation assets in the Yilgarn region of Western Australia and acquisition of the Kumina Iron Ore Project from BCI Minerals Limited. The company is well-positioned to create long-term to shareholders via development of its world-class resource assets and increased annuity-style earnings from enhanced mining services' offerings.

.png)

FY19 Results Summary (Source: Company Reports)

Highlights of Half-year Results: For the half year ended 31 December 2019 or H1FY20, the company generated statutory EBITDA of $1,575 million which includes a $1,290 million gain on the disposal of a 60% interest in the Wodgina Lithium Project (Wodgina). Further, the company reported underlying EBITDA of $330 million, up 224% on the pcp, underpinned by strong growth in the Mining Services segment and record iron ore sales. For the half-year period, the company declared an interim dividend of 23.0 cents per share, up 77% pcp.

During the half-year period, the company ramped up the Koolyanobbing iron ore production, with plans to further increase production to 11 million tonnes per annum from February 2020. The company also completed the acquisition of the Parker Range tenements from Cazaly Iron Pty Ltd, which are scheduled to enter production in 2H20. Due to the ramp up of Koolyanobbing as well as growth in external contracts, the company’s Mining Services business achieved a 95% growth in underlying EBITDA. The company finished the half-year with over $1.3 billion in cash and a net cash position of $79 million.

During the period, the company shipped 3.6Mt from Iron Valley with an average revenue of $98/t. From Mt Marion, the company shipped 194Kt spodumene concentrate with Average revenue of $674/t.

.png)

H1FY20 Results Highlights (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 49.15%. Ellison (Christopher James) and Airlie Funds Management Pty Ltd hold the maximum interest in the company at 11.65 % and 7.09%, respectively.

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Enhancing Iron Ore Footprint: On 31 March 2020, the company announced a series of agreements with BCI Minerals Limited (ASX: BCI) which are expected to enhance MIN’s Pilbara iron ore footprint. The agreements include the purchase by MIN of the Buckland Project from BCI for a total consideration of $20 million and the optimisation of the existing Iron Valley Agreement whereby BCI will participate in the capital investment required to extend the mine life at Iron Valley through a partial rebate of MIN’s payments to BCI. These agreements reflect MIN’s strong partnership with BCI and provide further opportunity for MIN’s Mining Services business to create value from stranded iron ore deposits in the Pilbara.

Restructuring of Non-Core Manganese Assets: On 19 March 2020, the company announced that it has entered into an Asset Sale Agreement with Resources Development Group Limited (ASX: RDG), as per which, MIN will transfer its Manganese Assets to RDG in return for MRL receiving scrip equivalent to a 75% shareholding in RDG. The transaction is expected to complete by FY20.

A Quick look at Key Margins: For H1FY20, the company reported gross margin of 98.6%, higher than the gross margin of pcp which stood at 95.9%. For the same time span, the company reported net margin of 89.6%, higher than the net margin of pcp. This demonstrates that the company has significantly improved its profitably over the last one year. The company currently has a current ratio of 2.23x, higher than the industry median of 1.76x, demonstrating that the company is well-positioned to pay its short-term obligations.

.png)

Key Metrics (Source: Thomson Reuters)

What to expect: Going forward, the company expects its existing and approved projects to drive medium-term growth. In the next three years, the company is aiming to double its production and revenue. Currently, the company has a strong pipeline of Mining Services contracts over the next 1-2 years.

In FY20, the company expects its crushing business contract volumes to grow more than 20%. Production from Mt Marion production is expected to be in between 360Kt and 380Kt. From Contract Mining Business, the total tonnes mined is expected to increase in excess of 75%. EBITDA from Mining services is expected to be in the range of $280 - $300 million in FY20. The company expects to spend up to $20 million in stages on drilling and feasibility work on iron ore in the Pilbara.

.png)

Profit Share Commodity Projects (Source: Company Reports)

Key Risks: The company’s activities are exposed to a variety of financial risks: market risk (including foreign currency risk, price risk and interest rate risk), credit risk and liquidity risk. However, to minimise the potential adverse effects on the financial performance of the company, MIN follows a risk management programme. In addition, it uses derivative financial instruments such as forward foreign exchange contracts to hedge certain risk exposures. The company is also exposed to a number of climate-related risks and opportunities, which might impact its ability to create and sustain value in the short, medium and long-term.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

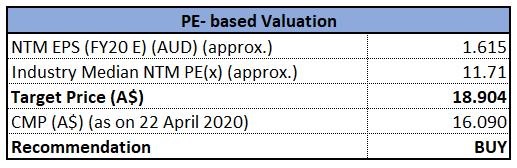

Valuation Methodology: P/E Multiple Based Relative Valuation (Illustrative)

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: MIN has a strong track record of providing return to shareholders. In the past six months, the stock of Min has provided a return of 27.42% to its shareholders. The company continues to invest to drive long-term income streams for the company, building on the high-quality portfolio of mining services contracts awarded over the past 25 years. We have valued the stock using Price to Earnings multiple based illustrative relative valuation method and have arrived at a target price with lower double-digit upside (in % terms). For the purpose, we have taken peers like IGO Ltd (ASX: IGO), Iluka Resources Ltd (ASX: ILU) and Western Areas Ltd (ASX: WSA). Considering, the company’s decent financial and operational performance, its FY20 outlook, improving profitability margins and current liquidity position, we give a “buy” recommendation on the stock at the current market price of $16.09, down by 1.349% on 22 April 2020.

MIN Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.