Company Overview: CYBG PLC is a United Kingdom-based company that operates through Clydesdale Bank PLC (Clydesdale Bank), Yorkshire Bank, B and Virgin Money brands. It offers a range of banking services for both retail and business customers through retail branches, business banking centers, direct and online channels, and brokers. Clydesdale Bank provides the United Kingdom retail and small and medium enterprises (SME) banking services. Clydesdale Bank's products and services include mortgages, current accounts, deposits, term lending, personal loans, working capital solutions, overdrafts, credit cards and payment and transaction services. The Bank consists of approximately 160 branches.

.png)

CYB Details

CYB Managed To Deliver Sustainable Customer Growth: CYBG PLC’s (ASX: CYB) corporate profile has been made up of 4 unique brands i.e. Clydesdale Bank, Yorkshire Bank, B and Virgin Money. As on July 1, 2019, the market capitalisation of CYBG PLC stood at ~A$4.9 billion. The group had delivered results for the six months ended December 2018 in which its pro forma underlying profit before tax stood at £286 million, which reflects a fall of 5% on the YoY basis because of the anticipated increase in the impairments, but the figure was up 2% on 2H FY 2018. The bank’s total underlying income amounted to £843 million in the first six months, which was in line with the 1H FY 2018 and 2H FY 2018. Its net interest income witnessed a fall of 1% on 1H FY 2018 and its Net Interest Margin (or NIM) stood at 171 bps (or basis points), and the company witnessed mortgage pricing pressures in 2018. The company’s non-interest income witnessed a rise of 11% on the YoY basis because of growth in the Virgin Atlantic credit card fee income. The bank had also witnessed growth in the customer lending of 2.4%, and it stood at £72.7 billion. Also, CYB stated that its customer deposits witnessed a rise of 1.2% and stood at £61.7 billion and there was an increase in the relationship savings balances. The bank had stated that integration has been progressing well and they have also incurred significant acquisition and integration costs.

Moving forward, the focus on increased shareholder value might help the group to gain traction among the market players. As stated in the interim financial results 2019 investor presentation, CYBG happens to be strongly capitalised, which might act as a tailwind for future growth.

.png)

Underlying P&L (pro forma basis) (Source: Company Reports)

Top 10 Shareholders: The following table gives the broader idea of the top 10 shareholders in CYBG PLC:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

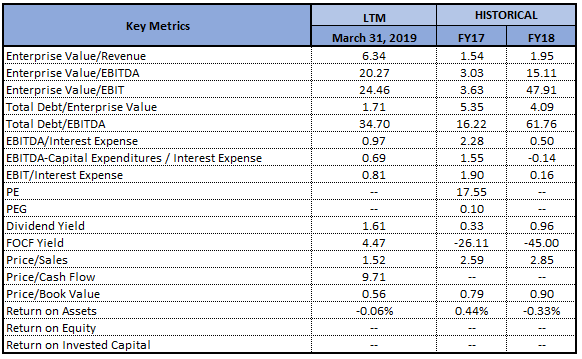

Lower Efficiency Ratio Builds Confidence in CYB’s Operational Capabilities: CYBG PLC’s efficiency ratio stood at 76.8% in 1H FY 2019, which is lower than the industry median of 84.6% and, thus, it looks like that the bank has been earning sufficiently to meet its non-interest expenses. The group’s net interest income had witnessed a CAGR growth of 2.04% in the time frame from FY 2014-FY 2018, which might be considered at respectable levels.

.png)

Key Metrics (Source: Thomson Reuters)

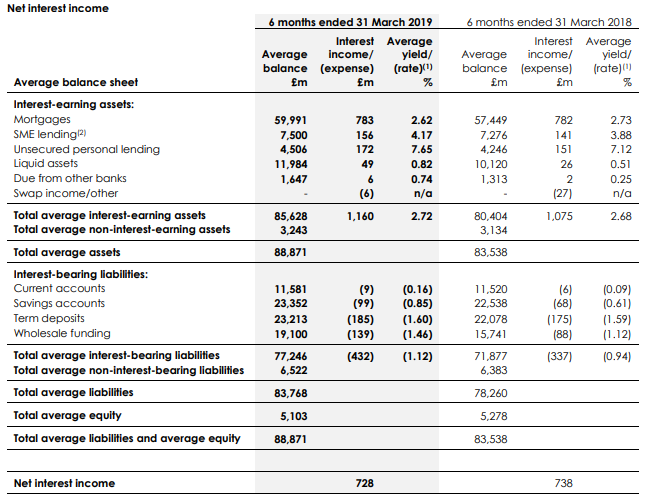

Decent Net Interest Margin: CYB stated that its NIM stood at 1.71% and had reduced from 1.84% since March 2018. The largest impact on Group’s NIM had been the continued dilution, which was witnessed in the mortgage margins because of sustained competition as well as more pressure in higher margin segments of the market. The bank had witnessed improvement in the yields in the SME book and there was a steady increase over the last 3 periods from 3.88% in the period to March 2018 to 4.17% in period to March 2019, with an emphasis on the pricing discipline as well as a higher interest rate environment helping the company to deliver the result.

Net interest income (Source: Company Reports)

CYB stated that its wholesale funding costs have witnessed an increase because of an increase in the issuance of senior debt as the company positions itself to meet the MREL requirements and the issuance of £250 million of the subordinated debt in December 2018.

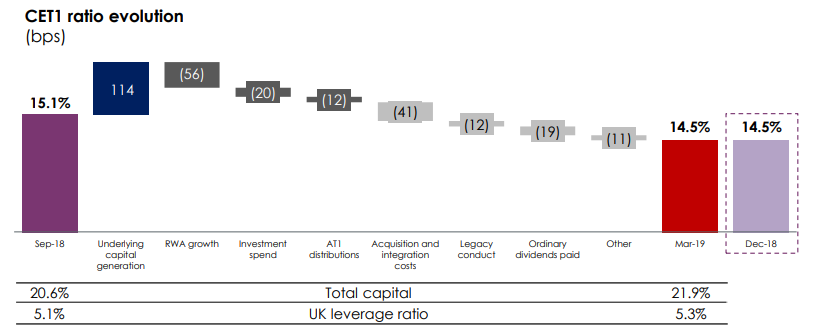

Understanding CYB’s Capital Position: CYB had managed to deliver the CET 1 ratio of 14.5% and the total capital ratio of 21.9% at March 2019. In the month of October 2018, CYB received accreditation to move onto IRB methodology for the calculation of risk-weighted assets on mortgages and corporate exposures, which increased its CET 1 ratio by 3.5%. Also, the acquisition of the Virgin Money group increased its CET 1 ratio by further 1.1%, which together with the impact of the introduction of IFRS 9, increased CYB’s September 2018 pro forma CET 1 ratio to 15.1%.

CET 1 Ratio Evolution (Source: Company Reports)

CYB continues to maintain the significant buffer to the regulatory capital requirements and the group remains confident in the ability to deliver net capital generation moving forward.

Announcement About External Appointment: CYBG PLC had notified the market that Darren Pope, which is an independent Non-Executive Director of the company, happens to be the Senior Independent Non-Executive Director and Chair of the Audit and Risk Committee of Network International Holdings plc.

Announcement Related to Total Voting Rights: CYBG PLC had also notified the market that, as of May 31, 2019, the total number of the voting rights of the company stood at 1,433,516,368. As at the close of business on May 31, 2019, the total number of the ordinary shares were 538,324,986 as well as the total number of CHESS Depositary Interests stood at 895,191,382. The release also stated that there are no shares which are held in the treasury.

Key Insights From CYBG PLC Capital Markets Day 2019: CYBG stated that they would be delivering the increased shareholder value through the four new strategic pillars i.e. pioneering growth, delighted customers and colleagues, super straightforward efficiency as well as discipline and sustainability. The group stated that, amidst the challenging operating environment, its strategy revolves around delivering on the actions, which are within the control as well as optimise the balance sheet mix in order to mitigate the industry pressures.

Further, the group stated that they are also starting the new Transformation Programme in order to realise the significant opportunities to digitise and simplify the internal processes, to deliver the improved customer propositions and cost efficiencies.

Understanding of CYB’s Funding and Liquidity Position: CYBG PLC continued to maintain the robust funding and liquidity position. The group’s loan to deposit ratio happens to be broadly stable over the period and it stood at 118%, as compared to September 30, 2018 number of 116%. The group’s liquidity surplus had been exceeding the regulatory minimum and internal risk appetite, with the LCR of 158% as compared to September 30, 2018 figure of 161%. The group’s NSFR stood at 125% as at March 31, 2019.

In addition to the retail and SME deposits, the group ensures the appropriate diversification in the funding base through the numerous wholesale funding programmes.

Key Valuation Metrics (Source: Thomson Reuters)

What To Expect From CYBG Moving Forward: CYBG PLC stated that the clear set of medium-term financial targets is expected to deliver the increased shareholder value. The group had re-affirmed the guidance for 2019 and it expects to post NIM in the range of 165-170 bps. It is also targeting approximately £200 million of the net cost savings by FY 2022 and is targeting operating costs < £780 million by FY 2022. The targets which have been set up by the group includes achieving the mid-40%’s in the cost to income ratio by FY 2022.

Additionally, CYBG PLC is also targeting approximately 13% of the CET 1 capital ratio. As per the key personnel of CYBG PLC, the achievement of the financial targets would be creating significantly more efficient and profitable business with the strong and sustainable returns for the shareholders. The company stated that its continued focus on the differentiated mortgage propositions had resulted in the annualised growth of 5.0% in the period, which is above the system growth of 2.6%. On the pro forma basis, the market share has witnessed an increase from 4.2% to 4.3%. The company, in the interim financial report, had stated that the pace of the lending growth in its mortgage book is anticipated to slow in 2H as the group looks to optimise the mix of lending in the portfolio as well as proactively reduce the volume in the selected segments to mitigate some of the margin pressures.

Stock Recommendation: Talking about the stock’s performance, it has posted the return of 4.59% in the span of previous six months, while on the YTD basis, it has delivered the return of 4.91%. However, in the past few months, the stock had witnessed some correction as it had fallen 2.01% and 7.57% in the span of one month and three months, respectively. As per ASX, the stock is trading towards its 52-week lower levels, proffering a decent opportunity for accumulation. The group had stated that the delivery of the strategy and the targets is anticipated to drive the strong shareholder returns, specifically the statutory RoTE (Return on Tangible Equity) of >12% by FY 2022, more than 100 bps of the excess CET 1 capital generation per annum by FY 2022 and progressive and sustainable ordinary dividend.

The group is having the diversified funding model, which might attract the attention of the market players moving forward. Also, the group has been managing the NIMs with the help of the portfolio mix. From the valuation front, it reported an NTM P/B multiple of 0.5x, which is lower than the industry median (banking service) of 0.9x, indicating that the stock is relatively undervalued. Given the backdrop of aforesaid facts coupled with decent CET 1 ratio in 1HFY19, growth in mortgage, and small & medium sized enterprises (SME) businesses, lower P/BV multiple than industry median, and anticipated decent shareholder return in the future, we give a “Buy” recommendation on the stock at the current market price of A$3.530 per share (up 3.216% on 01 July 2019).

.png)

CYB Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.