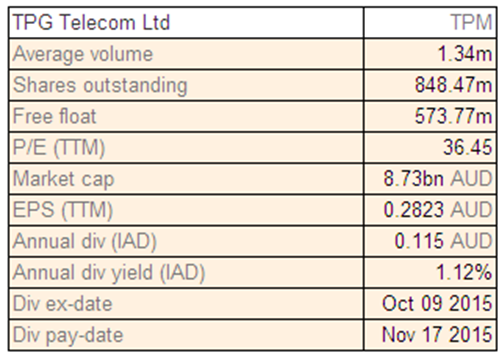

TPG Telecom Limited

TPM Dividend Details

Declining mobile subscriber base: TPG Telecom Limited (ASX: TPM) has consistently been delivering strong results over the recent past. According to its FY15 financials, the company achieved revenue of Australian $1.27 billion, which was an increase of about 31% from the FY14 revenue of $970.9 million. A prominent aspect of the company’s financial results was more than 30% increase in each of company’s earnings before interest, tax, depreciation and amortization (EBITDA), net profit after tax (NPAT of $224.1 million) and earnings per share (EPS).

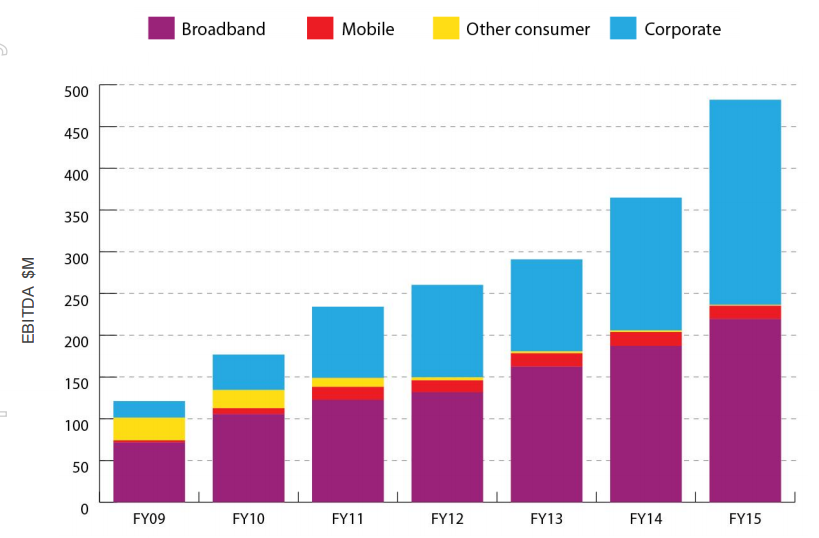

EBITDA Growth (Source: Company Reports)

The FY15 total dividend was 11.5 cents per share, which was a 24% increase over FY14. The company’s home phone subscribers and broadband subscribers have been increasing steadily over the years and stood at 591K and 821K respectively as of July 2015, but the mobile subscribers base has been declining and stands at 320K as of July 2015. This has been a concern and points to weakness in revenue stream for the company despite the huge market potential in mobile segment. The recent acquisition of iiNet has helped in strengthening the geographical presence of its brands. TPM will look to leverage iiNet’s strength in the small business segment. The company seems to have set its eyes on other acquisitions either in Australia or New Zealand. TPM has also acquired 1800MHz spectrum worth $84.7 million under the development front. Meanwhile, as of March 15, 2016 the stock rallied about 14.67% in the last one year.

Despite the overall positive growth prospects of TPM, the stock does not look attractive because it is trading at a premium with a high price to earnings ratio (P/E) and hence we give an “Expensive” recommendation at the current price levels of $10.38

TPM Daily Chart (Source: Thomson Reuters)

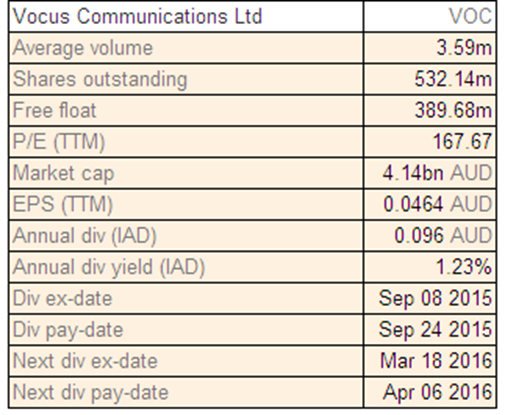

Vocus Communications Limited

VOC Dividend Details

Acquisitions adding to the strong organic growth: Vocus Communications Limited (ASX: VOC) announced record results for the half-year ended December 31, 2015. The results were taking into account the acquisition of Amcom which was completed in July 2015.

Core Capital Expenditure (Source: Company Reports)

Accordingly, the group’s revenue in Australia reached $176.3 million, an increase of 181% over last year, while net profit after tax (NPAT) was $27.4 million, up 203%. The earnings before interest, tax, depreciation and amortization (EBITDA) were $62.3 million, up 188% over last year. The 5-year compound annual growth rate in EBITDA was an impressive 68%. This followed the merger of Vocus with M2 Group Ltd. on February 22, 2016. M2 has also delivered strong growth with a half-year revenue of $707.4 million, an increase of 29% over previous year period. M2 will start contributing positively to Vocus Communications by helping it become a vertically integrated full-service telecommunications company.

Synergies of $40 million are expected by the end of FY18. The stock has also been added in S&P/ASX 100 Index as per the March quarter updates by S&P Dow Jones Indices. But, the stock is trading at a very high price to earnings ratio (P/E), which we believe is “Expensive” at the current price of $7.65

VOC Daily Chart (Source: Thomson Reuters)

Amaysim Australia Limited

AYS Details

Increasing ARPU and growth prospects: Amaysim Australia Limited (ASX: AYS) announced its financial results for the half year ended December 31, 2015 wherein the net revenue jumped 17.9% to $117.3 million from $99.5 million in H1 15. The underlying earnings before interest, tax, depreciation and amortization (EBITDA) saw a massive growth of almost 174% and stood at $12.6 million compared to $4.6 million in H1 15. Hence, the net profit after tax (NPAT) jumped by a massive 248% to $8 million. The company, which had its initial public offering (IPO) in July 2015, also announced a maiden dividend of 3 cents per share which was in line with previous guidance. The EBITDA growth reflected the increased subscriber base of Amaysim, which grew by about 12.5% from 679000 to 764000 and the increased operational leverage. The gross margin per subscriber stood at $8.01, exceeding the FY16 forecast of $7.93. This was a result of strong network service agreements (NSA) with Optus, pursuit of quality customers, online engagement and Amaysim’s capital light business model. The company’s unlimited plans have been a success in the competitive market and has helped increased the average revenue per user (ARPU). AYS has also made improvements (more data, unlimited standard international calls and billing cycles) to its core unlimited mobile plans.

.png)

Gross profit growth over the years (Source: Company Reports)

We believe that Amaysim has a very strong growth prospect in the Australian market because of the sizeable market size (the company has only 2.6% market share), smart phone penetration in Australia (73% Australians have a smartphone), and trend of purchasing outside of contract (65% of smartphones purchased outside of contract in 2015). The stock has also been added in S&P/ASX 300 Index and S&P All Ordinaries Index as per the March quarter updates by S&P Dow Jones Indices. Given the aforementioned, we give a “BUY” on the stock at the current price of $1.895

AYS Daily Chart (Source: Thomson Reuters)

Telstra Corporation Limited

.png)

TLS Dividend Details

Steady growth for the telecom giant: Telstra Corporation Limited (ASX: TLS) has maintained its sustained growth as revealed in its first-half results of 2016. Total income has increased by 9.1% to $14.2 billion while the company’s net profit after tax (NPAT) has remained almost at the same level, increasing by just 0.8% to $2.1 billion. The earnings before interest, tax, depreciation and amortization (EBITDA) were $5.4 billion, up 1.7%. The company also announced interim dividend of 15.5 cents per share, which is an increase of 3.3% compared to the previous corresponding period. Telstra Corporation now has total mobile subscriber base of 16.9 million, way ahead of its competitors. Telstra also recently announced upgrades in its mobile connectivity services, while aiming to implement 5G by 2020. With a strong performance in all its retail businesses, the company has provided a guidance of low-single digit growth in EBITDA and mid-single digit growth in total income.

Considering its size, the company is delivering impressive results but as expected, its competitors are growing at a much larger pace compared to it. We give an “Expensive” recommendation for TLS at the current price levels of $5.30

TLS Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.