Magellan Financial Group Ltd

.png)

MFG Dividend Details

High retail net inflows: For its first half financial year ended December 31, 2015, Magellan Financial Group Ltd (ASX: MFG)reported an after tax profit of $109.3 million or 63.7 fully diluted earnings per share, an increase of 41% from prior corresponding period.

.png)

Average monthly retail net inflows (Source: Company reports)

During the period, average monthly retail net inflows stood at $214 million, compared to $123 million earlier. Average funds under management was up 44% to $38.8 billion. Interim dividend was up 38% to 51.3 cents per share from year ago period. As at February 29, 2016, net outflows of $171 million with funds under management being $38.8 billion as opposed to $39.5 billion as at 29 January 2016, was noted. Nonetheless driven by a stable dividend yield and positive financial results, we rate the stock a "BUY" at the current share price of $22.90

MFG Daily Chart (Source: Thomson Reuters)

IOOF Holdings Ltd

.png)

IFL Dividend Details

Cost synergies and high dividend yield: IOOF Holdings Ltd (ASX: IFL) in its latest interim financial results reported an 18% rise in its underlying net profit after tax of $95.4 million from its prior comparable period. Statutory net profit after tax increased to $134.0 million, up 118%. During the period, successful Shadforth integration delivered $11.3 million in pre-tax cost synergies compared to $1.7 million.

.png)

Financial overview (Source: Company reports)

IFL is on track to deliver in excess of $30 million in total synergies by the end of FY16. Interim dividend increased 14% to 28.5 cents per share. The stock with a current dividend yield of 6.6 and strong top line and bottom line growth is rated a "BUY" at the current share price of $8.96

IFL Daily Chart (Source: Thomson Reuters)

VILLA WORLD LTD

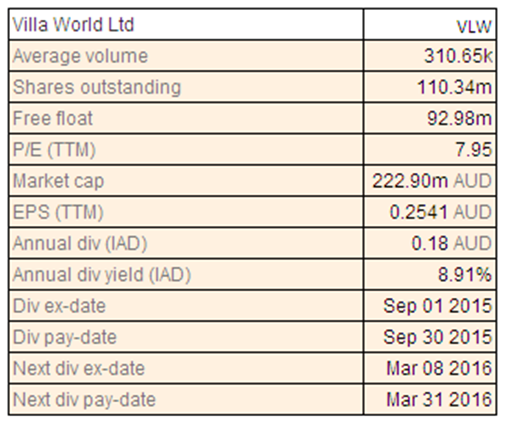

VLW Dividend Details

Increasing land-housing sales: For the first half financial results, Villa World Ltd (ASX: VLW) statutory profit after tax increased 57% to $20.4 million while earnings per share increased to 18.5 cents from 13.9 cents in year ago period. With a dividend yield of 8.91%, the company declared an 8 cents per share dividend compared to 6 cents in year ago period. Revenue rose 49% to $200.2 million mainly driven by 550 accounting settlements in delivery of land and housing compared to 329 in earlier period.

In the past three months, the company's stock price has increased 4.26% (as at March 04, 2016). Based on the above stated factors and strong financial results, we rate the stock a "Speculative Buy" at the current share price of $2.08

VLW Daily Chart (Source: Thomson Reuters)

Cedar Woods Properties Ltd

.png)

CWP Dividend Details

Strong foundation for 2H2016: Cedar Woods Properties Ltd (ASX: CWP) posted a record 100% growth in its first half net profit after tax to $18.1 million. Earnings per share rose to 23 cents from 11.6 cents in the earlier period. Revenue dipped 1.1% to $77.05 million, with presales of $176 million majority of which are anticipated to settle in second half of financial year.

Led by new acquisitions, total assets increased to $457.1 million from $383.3 million as of June 30, 2015. Net bank debt to equity at 25.9% is set to continue well within target range for second half. With a high dividend yield, positive half yearly financial performance and a strong outlook, we issue a "BUY" recommendation for the stock at the current share price of $4.02

.PNG)

CWP Daily Chart (Source: Thomson Reuters)

Surfstitch Group Ltd

.png)

SRF Details

Cost rationalization driving top line: Surfstitch Group Ltd (ASX: SRF) reported its first half financial results with pro forma sales of A$144.9 million, indicating a 40% increase from the prior year period. During the period, SRF recorded a 393 basis point improvement in operating costs to sales ratio led by cost rationalization and revenue scale benefits.

.png)

Revenue and gross profit contribution (Source: Company reports)

Pro forma EBITDA multiplied several times to A$13.9 million from A$ 3 million in year ago period, while net profit after tax increased to $5.7 million from $0.3 million. With no debt, the company is sitting on high cash reserves of $61.2 million which is an increase of 70% from prior year period. SRF recently indicated for investment in its content network for growth prospects, and did not specify for its previous FY16 EBITDA guidance of $18m-$22m.

However, SRF’s effort towards growth on the basis of some investment is not expected to be an unfavourable step given its operations and capitalised position. Based on the above stated factors, we rate the stock a "BUY" at the current share price of $1.24

.PNG)

SRF Daily Chart (Source: Thomson Reuters)

iCar Asia Ltd

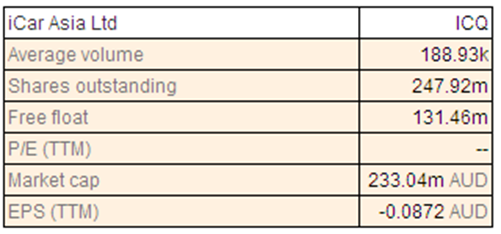

ICQ Details

Narrowing loss and rising sales: iCar Asia Ltd (ASX: ICQ) recently reported financials for year-ending December 31, 2015 with group revenue of $6.28 million, an increase of 123% from prior year period. Supported by a strong revenue growth and well managed costs, net loss after taxes were reduced to $12.5 million from $16.7 million in year ago period. EBITDA loss also narrowed down to $11.46 million from $13.19 million. During the month of December alone, 570,000 unique, individual car buyers sent leads to car sellers across Malaysia, Indonesia and Thailand. Cash collections for full year totalled to A$6.20 million, an increase of 113% over 2014. Based on the foregoing, we give a “BUY” recommendation at the current price of $0.925

.PNG)

ICQ Daily Chart (Source: Thomson Reuters)

Peet Ltd

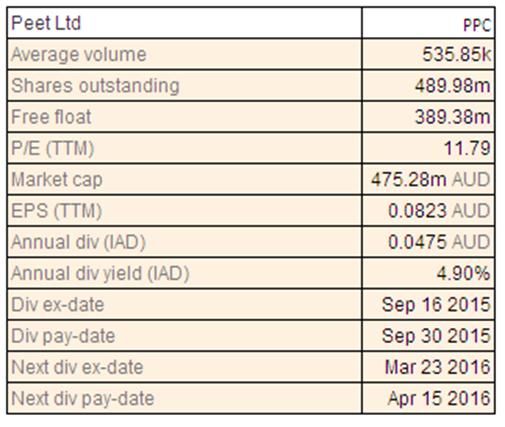

PPC Dividend Details

Record first half with a bright outlook: For the first half financial year 2016, Peet Ltd (ASX: PPC) recorded operating profit after tax of $18.5 million which is an increase of 8% from the year ago period. The Group achieved a total of 1,659 sales during the first half, representing an increase of 3% on the previous corresponding period. As of December 31, 2015, a record number of 2,318 contracts were on hand with a gross value of $523 million, compared with 2,061 contracts on hand as of June 30, 2015 with a gross value of $441 million. This provides a good momentum moving into the second half of FY16.

.png)

Financial highlights (Source: Company reports)

With a dividend yield of 4.9%, PPC declared an interim dividend of 1.75 cents per share, higher by 17% from year ago period. Based on solid first half performance and an attractive dividend yield, we rate the stock a "BUY" at the current share price of $1.00

PPC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.